Luke Allchin, Director, North America

As 2026 fast approaches, the consumer financial services landscape in the United States is entering a phase of rapid transformation. While global trends are shaping the industry, the US market faces unique pressures. Consumer expectations, regulatory pressures, and technological innovation are creating both challenges and opportunities. From artificial intelligence (AI) adoption to evolving fraud tactics and wealth management strategies, banks and financial institutions must adapt quickly to remain competitive. In this article, I explore the five key trends identified in RFI Global’s Trends & Predictions 2026 report from a US perspective and what they mean for US financial institutions.

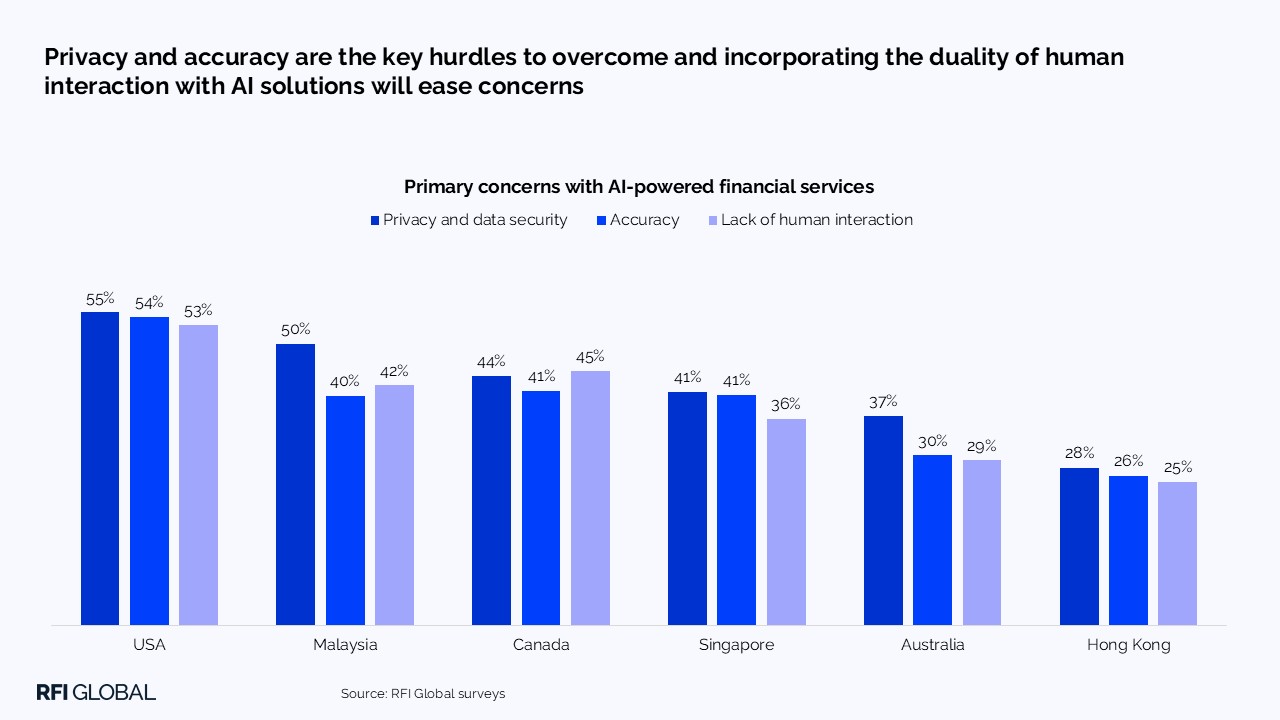

Trend #1. From curiosity to confidence: Building trust in AI-powered finance

AI is no longer a novelty in banking; it has become integral to fraud detection, risk management, and customer service. Yet, trust remains a significant barrier in the US. RFI Global’s MacroMonitor data shows that 84% of American consumers express concerns about AI in banking. Their main worries include privacy, security, reduced human interaction, and potential errors. Over half (54%) doubt AI’s accuracy, and nearly a third (32%) demand regular audits and transparency.

Unlike Asia, where AI adoption is accelerating, North America remains cautious. US consumers favour AI for fraud detection but show limited interest in virtual assistants or automated recommendations. Personalisation and human support are still highly valued, with many preferring a hybrid model combining AI efficiency with human reassurance.

To drive adoption, US institutions must prioritize transparency, robust privacy standards, and clear communication. Regular audits and explainable AI will be essential to build confidence. Banks that fail to address trust concerns risk lagging behind global and domestic competitors in leveraging AI for operational efficiency and customer engagement.

Read more about the US perspective on the rise of AI in finance here.

Trend #2. Digital user experience: The key battleground for customer loyalty

Mobile banking has become the primary channel for US consumers, with apps serving as the central hub for financial interactions. Our iSky platform tracks thousands of real consumer and business interactions with banking apps worldwide. The data reveals a wave of innovation in areas that matter most to customers – security and control.

The shift is no longer about digital access but digital empowerment, giving customers control, customization, and transparency. Leading US banks, such as Chase, have expanded beyond core banking into travel, equity trading, and automated money management. These additions are setting new expectations for integrated services.

Security remains a top priority. US banks are investing heavily in security hubs that combine fraud controls, alerts, and educational resources. Strong card management tools and customer-controlled security settings are now standard features.

Superior digital experiences will determine loyalty. Institutions that fail to deliver seamless, secure, and personalised digital services risk competing solely on price. The benchmark set by global neobanks means US banks must innovate continuously to retain relevance.

Listen to our Banking Uncovered podcast to find out more about digital UX.

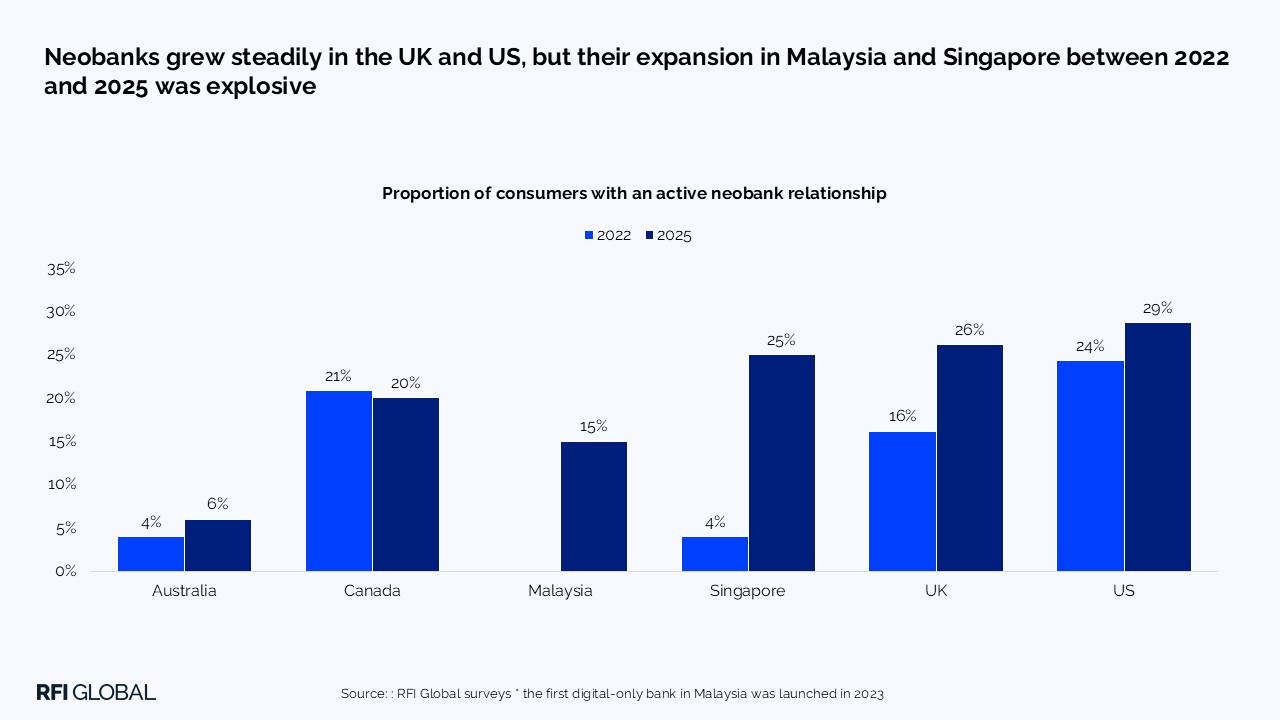

Trend #3. The next chapter for neobanks: From growth to value

Neobanks in the US have moved beyond rapid customer acquisition to focus on engagement and profitability. Adoption is strong. MacroMonitor data shows that 29% of US consumers now use neobanks, more than all other markets in the report, and primary banking relationships have nearly doubled since 2022. Players like SoFi have diversified into lending, investing, and insurance, achieving profitability and positioning themselves as full-service financial institutions.

AI-driven personalisation, embedded finance, and loyalty programs are key differentiators. By 2026, US neobanks are expected to rival traditional banks through innovation and strategic partnerships.

Incumbents must respond with competitive digital offerings and explore partnerships with fintechs. Failure to match neobank agility could lead to erosion of market share, particularly among younger, tech-savvy consumers.

Read more about the fintech evolution in the US.

Trend #4. Cybersecurity: Fraud has evolved, but have banks?

Fraud tactics are becoming more sophisticated, driven by AI-enabled schemes such as voice cloning and synthetic identity fraud. At the same time, anxiety around financial security is growing in the US. MacroMonitor highlights this fact, with 37% of US households expressing concern about the safety of their deposits. Yet only 23% are comfortable with AI for fraud detection and prevention (compared with 74% in Singapore and 50% in Canada. Among households considering switching their main banking relationship, 11% cite fraud concerns as the driver behind this.

Traditional methods are no longer sufficient. Advanced fraud detection now requires behavioral biometrics and multi-source data analytics to minimize friction while enhancing protection.

Cross-industry collaboration and data sharing are critical to combat organized scams, and regulatory scrutiny is intensifying. US banks must leverage AI analytics not only for efficiency but as a frontline defense against evolving threats.

Institutions that fail to modernize fraud prevention risk reputational damage and financial loss. Investments in AI-driven security, customer education, and collaborative frameworks will be essential to maintain trust and compliance.

Read more about the importance of trust in an era of increasing fraud.

Trend #5. Wealth in 2026: Unlocking fee-based growth as affluent investments rise

The US remains a global leader in equity investments. According to MacroMonitor data, High-Net-Worth households hold $8.06 trillion in mutual funds. This is a sharp increase from previous years ($6.02 trillion in 2022 and $3.49 trillion in 2020). Digital platforms and fintechs are capturing investor market share, challenging traditional banks to innovate. Meanwhile, Mass Affluent consumers still keep nearly half of their assets in low-yield deposits, signaling a major opportunity for conversion.

Success will hinge on delivering tailored advisory services and seamless digital experiences that encourage movement from deposits to higher-yield investments. Fee-based growth strategies, supported by personalisation and visibility, will be critical to capitalizing on this trend.

Read more about what $45 trillion wealth transfer means for firms and families.

The year ahead for US financial institutions

The next 12 months will be pivotal for US financial institutions. Building trust in AI, delivering superior digital experiences, competing with agile neobanks, strengthening fraud defenses, and unlocking wealth opportunities are all vitally important. Financial institutions that understand their customers’ evolving needs and act decisively will best position themselves for sustainable growth in an increasingly competitive and technology-driven market.

Download the full Financial Services Trends and Predictions 2026 report for a deeper view of these trends and to understand how the US compares with other key markets. It brings together global benchmarks, market-by-market analysis, and consumer insights to help financial institutions plan with confidence for the year ahead.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileFrequently asked questions about the future of US financial services

Q: What are the biggest financial services trends shaping the US market in 2026?

A: The US market is being reshaped by five major forces: the need to build trust in AI, rising expectations around digital banking experiences, the shift of neobanks from growth to value creation, rapidly evolving fraud threats, and new wealth opportunities driven by changing consumer investment behaviour.

Q: Why is AI adoption progressing more slowly in US banking compared with other markets?

A: US consumers remain cautious about AI in financial services, particularly around accuracy, privacy, and transparency. US consumers favor AI for fraud detection but show limited interest in virtual assistants or automated recommendations.

Q: How are neobanks changing the US competitive landscape?

A: US neobanks are moving beyond customer acquisition to focus on engagement, profitability, and broader financial ecosystems. Their rapid growth and diversification—into lending, investing, and insurance—are putting pressure on traditional institutions to innovate faster.

Q: What fraud and cybersecurity challenges are US banks facing in 2026?

A: Fraud tactics are becoming more sophisticated, driven by AI-enabled scams and synthetic identities. At the same time, only a minority of US consumers feel comfortable with AI in fraud prevention, making it critical for institutions to invest in advanced analytics, behavioural biometrics, and customer education.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.