Luke Allchin, Director, North America

I recently had the pleasure of joining Charles Green on RFI Global’s Banking Uncovered podcast to discuss the latest findings from our MacroMonitor study. The conversation shed light on how rapidly the financial services landscape is evolving in the US, especially when it comes to digital, fintech, and how consumers seek financial guidance.

Fintechs gain ground in the US

One of the standout trends from our study is the significant momentum challenger banks and fintechs alike are gaining in the US. While traditional institutions have long held dominant positions, fintech players are steadily growing their share of the market. The latest data from MacroMonitor shows that 31% of primary bank accounts opened within the last 24 months were with challenger banks such as Chime and SoFi. Consumers are increasingly comfortable with these platforms, not only for managing their money but also for investing. This shift is more than a trend, it’s a transformation that is likely to continue.

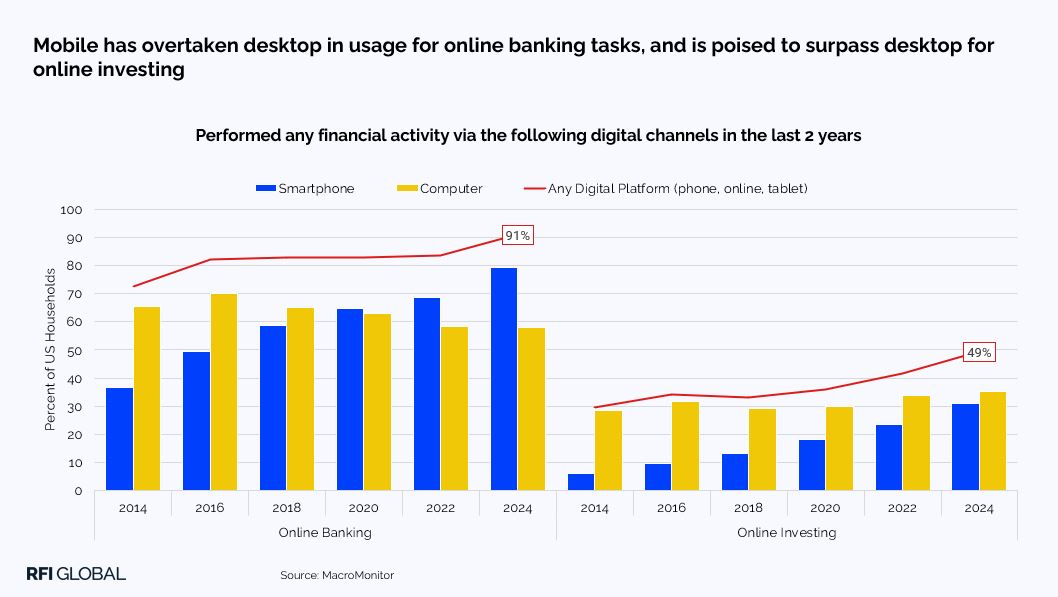

Though branch and community banks still have a place in the market, the growing comfort in digital means their importance is gradually fading. Consumers are shifting toward digital channels in greater numbers, both in usage and in the variety of tasks they’re completing online. Mobile has emerged as the #1 choice for banking and is poised to become the preferred digital channel for investing as well – if usage trends continue, we expect to see mobile surpass desktop early into 2026.

Furthermore, switching between providers is becoming more common, with households more open than ever to exploring new products, services, and platforms. This creates significant pressure on providers that are slow to innovate in a rapidly changing market.

A more independent, yet cautious consumer

We’re also seeing a rise in self-directed financial behavior. As such, households are increasingly looking to simplify their financial management, prompting many to consider consolidating their assets and relationships (31% of households, up from 24% in 2022). This trend puts banking and investment providers at risk of client attrition, especially if they fail to evolve with consumer expectations.

Younger households are entering the investment space earlier, making a strong digital offering essential to attract and retain this growing segment. At the same time, households are becoming more risk-averse. This is reflected in a notable increase in funds held in certificates of deposit (CDs) and a decrease in liquid assets, even as overall wealth levels trend upward.

Interestingly, this cautious approach varies by income. Higher earners continue to take investment risks, while lower-income consumers are opting for safer financial decisions where possible.

Cost awareness and openness to innovation

Another shift is the growing cost-consciousness among consumers. Fintechs are often perceived as more cost-effective than traditional financial providers, which is driving greater interest and trial of new tools and services, including robo-advisors and AI-powered solutions.

Recognizing these shifts, incumbents are beginning to adapt. Institutions like Citi have launched digital-first wealth offerings and modernizing their services to stay relevant.

Consumers are not just looking for affordability, they’re also showing a new level of openness to innovation. For this reason, hybrid advisory models, blending traditional advice with robo-advisory services, should strike the right balance between personalized service and scalable efficiency. When delivered effectively, these models can help foster greater trust among consumers.

The rise in demand for financial advice and the role of social media

There is also a rising demand for comprehensive financial advice (64% of households seek professional advice before making major financial decisions, up from 60% in 2022), with households seeking guidance on a broader range of topics than ever before. Expectations for proactive, personalized communication are increasing, as consumers face unique challenges and want to feel understood by their advisors.

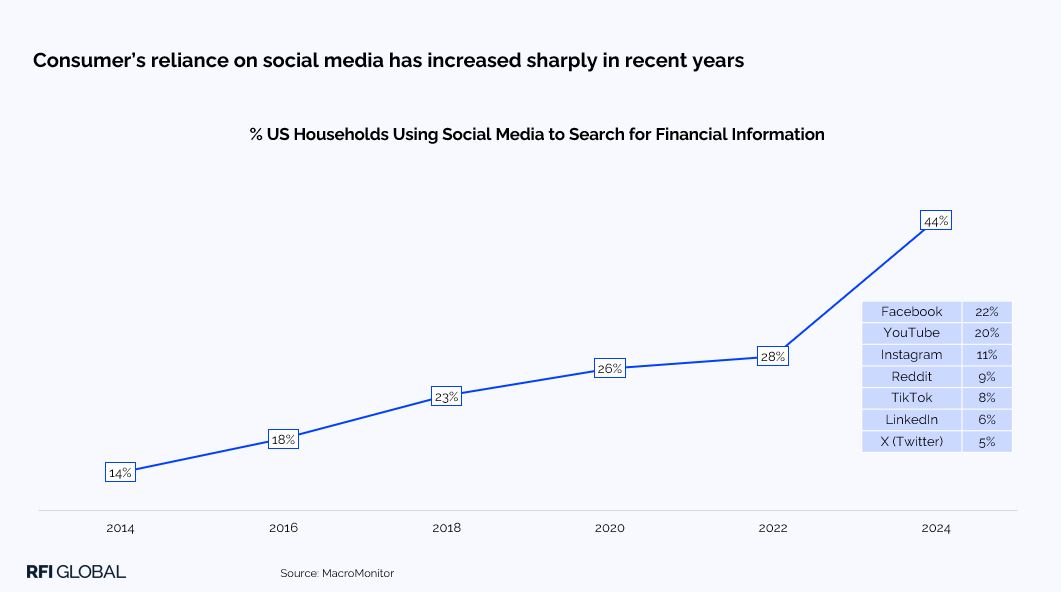

Parallel to the growing need for professional advice, a growing number of households see social media as a powerful source of financial information. While this presents a challenge due to the rise of ‘finfluencers’ and unvetted advice, it’s also an opportunity. Financial institutions have a real chance to become trusted voices in these conversations, offering clarity and credibility in a crowded digital space.

Looking ahead

The financial services industry in the US is at a pivotal point in time, driven by technology, consumer behavior, and a growing appetite for cost-effective, digital solutions. As consumers become more self-directed and digitally native, financial providers, whether fintechs, challengers or incumbents, must be ready to meet them with tools, services, and guidance that reflect this new reality.

It’s an exciting time for the industry, and we’re just getting started. We’ve only scratched the surface of the insights from our latest MacroMonitor study. For a deeper dive into what’s driving change—and how you can stay ahead—tune in to the full conversation on the Banking Uncovered podcast and watch the webinar on demand.

Get in touch for more insights from MacroMonitor and subscribe to our monthly newsletter for the latest data-driven financial service insights.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.