Scott Manderson, Executive Director, Australia

Rapid advances in AI and digital capabilities are changing how consumers interact with their banks, while economic pressures and market uncertainty in 2025 influenced expectations around value, loyalty and service. RFI Global’s data shows that Australian consumers entered 2026 with a more positive outlook, with consumer sentiment rising from 90.3 in December 2024 to 97.3 by the end of 2025 – its highest level since mid-2022.

However, customer expectations are rising just as quickly. As financial pressure eases, consumers are placing greater emphasis on how well their bank supports them day-to-day, rewarding loyalty, delivering value, enabling frictionless digital experiences and providing the tools to manage money with clarity and control.

Based on insights from over 62,000 Australian consumers, this article explores what drives advocacy, how leading banks are differentiating, and what it will take to sustain loyalty in an increasingly competitive market.

Advocacy is rising – but not evenly

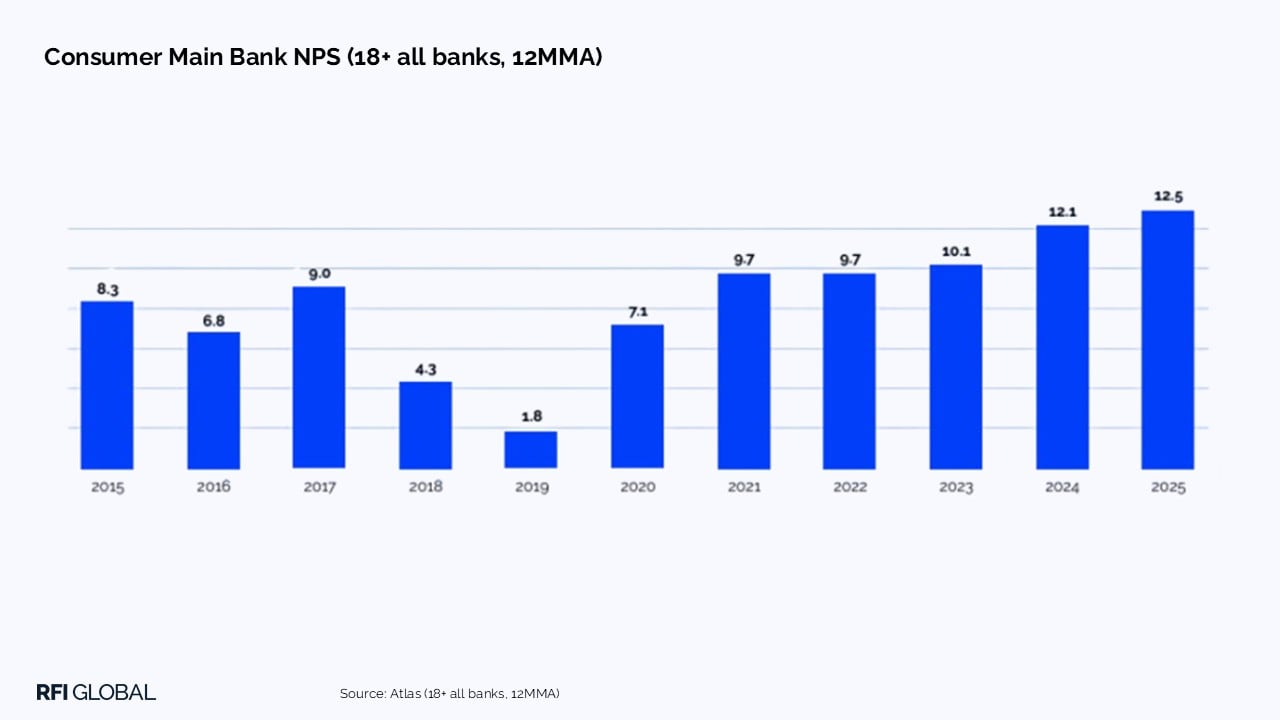

Improving sentiment has translated into stronger bank advocacy across the market. Australian consumers are now more likely to recommend their main bank than at any point on record, building on gains made in 2024.

This uplift has been largely driven by the major banks, all of which improved their Net Promoter Scores (NPS) through 2025, with two reaching record highs.

Commonwealth Bank stood out in RFI Global’s Australian Banking & Finance Awards 2026, as the Most Recommended Major Consumer Bank, underpinned by consistently strong performance across the customer journey. Its ability to deliver across trust, service, innovation and digital experience saw it lead in multiple award categories.

Among non-majors, Up continues to redefine customer advocacy, winning Most Recommended Non-Major Consumer Bank. Its performance highlights the strength of a clearly differentiated proposition built around transparency, usability and customer-centric design.

However, market-level gains mask increasing divergence. While leading institutions are strengthening relationships, others are losing ground, so improved sentiment alone is not enough to secure loyalty.

Value, trust and recognition are driving NPS

The drivers of advocacy in 2025 reflect a shift from price sensitivity alone to a broader definition of value. The most significant gains came from price competitiveness and reputation, supported by tangible improvements in product design and customer engagement. Competitive rates remain important, but they are no longer sufficient in isolation.

Customers are responding to:

- Products that reward behaviour and loyalty

- Greater transparency and perceived fairness

- A sense that their bank is willing to negotiate and recognise their value

- Bundled propositions that deliver clear, combined benefits

Rewards programmes are a key differentiator, but only when executed effectively. Well-designed programmes drive sustained improvements in advocacy, while poorly targeted initiatives have minimal impact.

At the same time, trust remains foundational. Confidence that a bank will ‘do the right thing’, combined with products that meet real financial needs, continues to underpin long-term advocacy.

Raising the bar for digital experience

As digital capabilities evolve, the digital experience has become central to how consumers evaluate their bank. Customers increasingly expect seamless, intuitive and secure interactions across every touchpoint, from onboarding through to everyday servicing. Friction is no longer tolerated, and willingness to switch is increasing where digital experiences fall short.

Security and control are now critical. Features such as real-time notifications, card locking and fraud protection rank among the most important elements of the app experience, reflecting a growing need for reassurance alongside convenience.

While fintechs and challenger banks have redefined expectations of digital, our Awards clearly show that incumbents are equally able to excel in the digital space.

Westpac topped the big four in the digital awards for consumer website and iPhone apps. Its ecosystem of tools – from predictive bill tracking to AI-driven budgeting and real-time card controls – demonstrates how digital can simplify financial management and reduce reliance on assisted channels.

At the same time, digital-first players such as Macquarie and Revolut continue to push the boundaries of functionality, embedding real-time payments, advanced security features and AI-driven assistance into everyday banking journeys.

From improving sentiment to intensifying competition

Despite rising advocacy, competitive pressure is building. With interest rates increasing again in early 2026 and further changes expected, many consumers are reassessing their financial positions. Nearly a third of mortgage holders indicate they may reconsider their provider in search of better rates, while savers are actively comparing options to maximise returns. As a result, many consumers may reconsider their main bank relationship in search of a better deal.

The gains in loyalty achieved over the past two years will now be tested.

What this means for banks and fintechs in 2026

The 2026 landscape will not be defined by sentiment alone, but by how effectively institutions convert improving confidence into durable customer relationships. Our analysis of Australian financial services brands across consumer banking uncovers three strategic imperatives for banks and fintechs:

1. Move beyond price to deliver holistic value

Competitive pricing remains necessary, but differentiation will come from how value is packaged and delivered. This includes meaningful rewards, transparent product structures and benefits that evolve with customer needs. Institutions that fail to move beyond rate-led competition risk accelerated churn as customers shop around.

2. Turn digital capability into everyday utility

Investment in digital must translate into tangible customer outcomes. The leaders are those enabling customers to act; to understand their finances, make decisions quickly and resolve issues without friction. Real-time control, proactive insights and embedded security are no longer optional – they are central to the customer proposition.

3. Deepen relationships through relevance and recognition

Customers increasingly expect to feel understood and valued. This requires more than surface-level personalisation. It demands a deeper understanding of behaviours, needs and life stage – and the ability to respond with relevant products, timely engagement and consistent experiences across channels.

As expectations continue to rise, competitive advantage will come from truly understanding customers’ evolving needs, making banking simpler, more transparent and more responsive to the realities of customers’ financial lives, turning short-term satisfaction gains into long-term loyalty.

For a deeper dive into the trends shaping customer behaviour, and a detailed breakdown of how leading institutions are driving advocacy, trust and growth, download the full Australian Banking & Finance Awards 2026 booklet.

Scott Manderson

Executive Director, Australia

Scott Manderson is an Executive Director at RFI Global, overseeing the firm's work across the Australian market.

View full profileFrequently asked questions about Australian banking

Q: What is driving loyalty in Australian banking?

Rising consumer sentiment through 2025 has lifted advocacy across the Australian banking sector, but loyalty gains are being driven by more than improved confidence alone. RFI Global data shows customers are responding to banks that deliver clear everyday value, recognise loyalty and provide trusted, low‑friction digital experiences – not just competitive pricing.

Q: What drives a strong Net Promoter Score (NPS)?

A strong Net Promoter Score in Australian banking is driven by a combination of improving consumer confidence and banks’ ability to deliver clear, everyday value. RFI Global data shows that beyond competitive pricing, customers reward banks that demonstrate trust, transparency and perceived fairness, recognise loyalty, and provide products that meet real financial needs. Well‑designed rewards programmes, a willingness to engage and negotiate, and seamless, secure digital experiences that give customers control and clarity all contribute to stronger advocacy and sustained NPS performance.

Q: How are customer expectations of digital banking evolving in Australia?

Digital experience has become a core determinant of advocacy. Australian consumers now expect seamless, secure and intuitive digital interactions across the full customer journey, from onboarding to everyday servicing. Real‑time controls, fraud protection and AI‑enabled tools that simplify money management are increasingly viewed as hygiene factors, with poor digital performance driving greater willingness to switch banks.

Q: How likely are customers to switch banks in Australia?

Customer willingness to switch is increasing despite improved overall sentiment. Nearly a third of mortgage holders indicate they may reconsider their provider in response to rising interest rates, while savers are actively comparing options to maximise returns. This is creating a more fluid and competitive market, where recent gains in loyalty are likely to be tested as customers reassess value.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.