Mark Donohue, Managing Director iSky, Global

Mobile is the key battleground in banking. For most consumers worldwide, the mobile app is the primary way they interact with their financial institution. In mobile-first markets such as China and India, this behaviour has long been established, and it is increasingly the norm across global markets. As a result, the digital experience plays a central role in shaping customer engagement, brand perception and loyalty.

For many customers, the app is now the bank.

As mobile has become the dominant channel, screen real estate is more valuable than ever. With customer expectations rising, the quality of the digital user experience has become a key differentiator.

The institutions that succeed in this environment are those delivering seamless, secure and intuitive digital journeys that empower customers, strengthen trust and foster long-term loyalty in a highly competitive market.

How the app landscape is evolving

Our iSky Radar portal tracks thousands of banking and insurance apps and web channels across almost 400 providers. For our Trends & Predictions 2026 report, we analysed how features have evolved. We saw a vast increase in the number of features available, with significant growth in debit card management, marketing and sales, and privacy and payments self-service experiences.

Security-related features are becoming increasingly prominent as both banks and customers prioritise protection. Features allowing the ability to temporarily lock or disable a card have increased by 13.8% over the past two years. And one of the most highly sought-after features globally, the ability to cancel and replace a card also grew steadily.

With the growing importance of trust and data security, we saw banks increasingly embedding customer-controlled security and profile features in app, allowing users to manage their own digital footprint. Over the past two years, 16% of benchmarked banks globally have added profile or account closing features within their apps for the first time.

We’ve also seen an increase in features allowing customer control. Over the past year alone, more than 10% of apps benchmarked globally have added the ability for customers to view card details directly within the app.

Despite this rapid expansion in functionality, many banks are simultaneously working to simplify navigation and reduce cognitive load. As digital capabilities grow, the challenge is ensuring that apps remain intuitive and easy for consumers to use in everyday financial management.

Who’s leading best practice?

While digital-first challengers have often been credited with setting the benchmark for mobile experiences, the reality today is more nuanced.

At the recent RFI Global Banking & Finance Awards in Australia, digital-only provider Revolut won one of the consumer iPhone app awards. However, traditional bank Westpac captured two of the four awards in the same category. A similar pattern is emerging in other markets, where high-street institutions continue to compete strongly alongside fintech entrants.

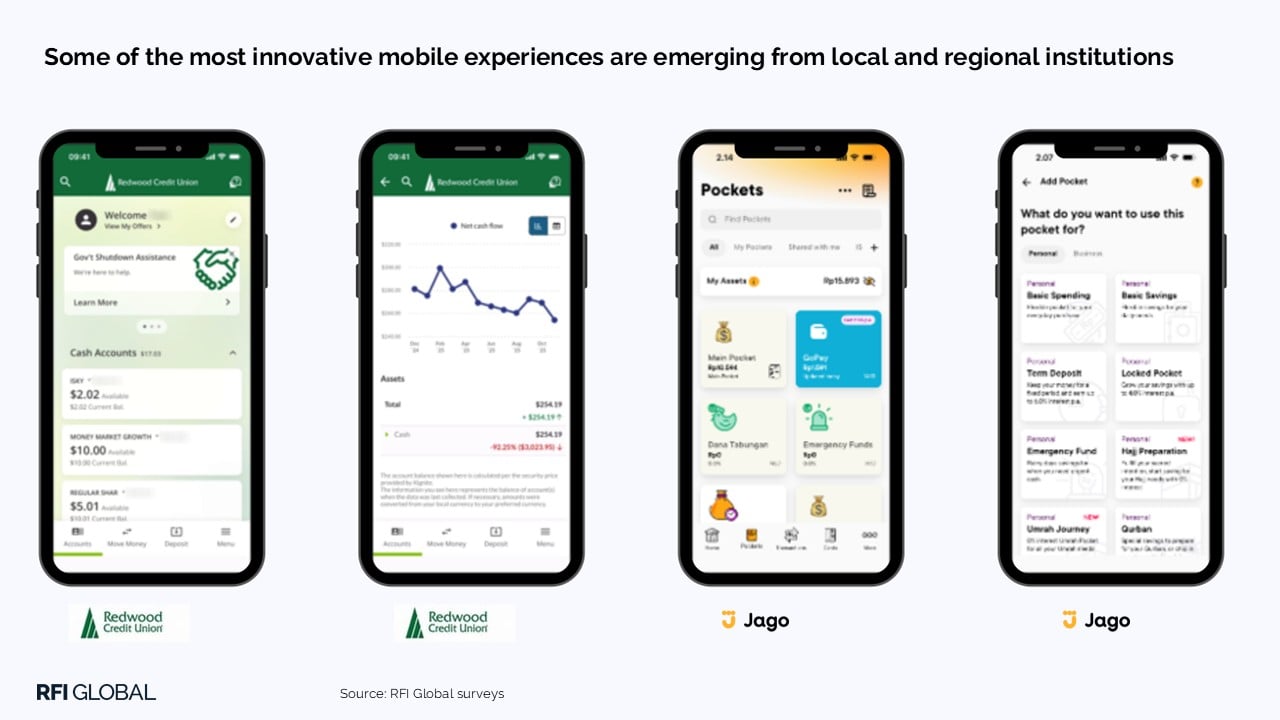

Best practice is also not limited to big global players with big budgets. Some of the most innovative mobile experiences are emerging from local and regional institutions that are designing solutions around the specific needs of their markets. In the United States, credit unions such as Redwood in Northern California has developed extensive digital self-service, while Jago in Indonesia has gained recognition for its flexible ‘pockets’ system that allows customers to organise their money in ways that reflect how they actually manage their finances.

Fintech providers often introduce new and unconventional features – sometimes expanding well beyond traditional banking. However, these innovations are not always aligned with customers’ everyday financial needs. Many established banks, and local players, by contrast, are focused on delivering the core capabilities customers use most frequently, ensuring the app remains a central and reliable financial hub.

What banks should focus on

As the mobile channel continues to evolve, the most successful providers will be those that balance innovation with clarity, relevance and simplicity. In a mobile-first world, customer satisfaction increasingly depends on the quality of the app experience. Institutions that fail to evolve the digital journey or address emerging customer concerns risk undermining loyalty.

1. Simplicity is a powerful differentiator

At its core, what customers want is simplicity. Leading neobanks have demonstrated the value of presenting clear, easily digestible insights that customers can act on immediately.

Rather than overwhelming users with information, the most effective apps surface relevant data points and translate them into straightforward actions that help customers manage their finances more confidently, and in the moment.

2. Customisation and personalisation

There are two ways of tailoring solutions for customers: customisation and personalisation. Customisation allows the user to shape their own experience, adjusting the interface, navigation or features to suit their preferences. Customisation is becoming more sophisticated, with banks allowing customers to choose between different designs and experiences. Personalisation is driven by the bank, using customer data to tailor communications, insights and offers. Institutions that are both data-rich and data-ready will be better positioned to deliver relevant services and insights.

3. Building a financial toolkit

The most effective mobile banking experiences are increasingly being built around a financial toolkit rather than a single static interface. Banks are introducing tools such as virtual cards, spending controls, card locks, automation features and virtual accounts that allow customers to manage their finances in more flexible ways. By giving customers greater control over how they manage money, banks can create more engaging and practical digital experiences.

4. Visible security builds trust

Security has always been fundamental to digital banking, but the way it is communicated to customers is evolving. Too much security friction can create a frustrating experience, while overly frictionless journeys can heighten the risk of fraud. Increasingly, banks are making security more visible through tools such as security hubs that allow customers to monitor activity and manage their own settings. Institutions that balance strong protection with transparency and customer control will be best placed to build trust and confidence in digital channels.

5. Investing where value is created

As digital banking continues to evolve, institutions must think carefully about where they invest in new features and capabilities. Not every innovation will drive meaningful engagement or commercial value, and banks need to focus on developments that address real customer priorities while also supporting sustainable profitability.

Institutions that maximise the use of all their customer data from every source and take a more entrepreneurial approach will be able to focus innovation on capabilities that both improve the customer experience and create measurable economic value.

Looking ahead

Mobile banking will continue to evolve rapidly. Simplicity, trust, personalisation and customer control will remain central to the next generation of digital experiences.

At the same time, the web channel is likely to become more specialised, supporting larger and more complex financial decisions where a bigger interface is still valuable.

Ultimately, success will depend on how well banks understand their customers and the context in which they live and make financial decisions. Institutions that combine deep customer insight with intelligent digital design will be best positioned to create meaningful and lasting value.

Find out more about benchmarking your digital user experience:

Listen to our Banking Uncovered podcast.

Mark Donohue

Managing Director iSky, Global

Mark Donohue is Managing Director of iSky at RFI Global, working with clients globally on data-led financial services intelligence.

View full profileFrequently asked questions about AI in financial services

Q: How is the mobile banking app landscape evolving globally?

Mobile banking apps worldwide are rapidly adding features for card management, payments, privacy and self-service. Banks are also making security more visible and simplifying navigation to create intuitive, user-friendly experiences. These changes reflect a global shift toward apps that balance functionality with ease of use, meeting rising customer expectations.

Q: What are the top trends in digital banking user experience?

The most important trends in banking app UX include simplicity, customisation, personalisation, visible security and flexible financial toolkits. Features like virtual cards, spending controls, automation tools and self-managed security hubs empower users and make apps more intuitive, practical, and effective for everyday financial management.

Q: Which banks are leading best practice in mobile banking apps?

Best practice is emerging across digital-first challengers, traditional banks and local or regional institutions. Global leaders like Revolut and Westpac set benchmarks, while local players such as Jago in Indonesia innovate with solutions like the flexible ‘pockets’ system, reflecting how customers actually organise their money.

Q: How should banks prioritise investments in mobile banking features?

Banks should invest in features that align with real customer priorities and deliver measurable business value. By leveraging customer data effectively and taking an entrepreneurial approach, institutions can focus on innovations that enhance engagement, loyalty, and profitability, avoiding features that do not create meaningful impact.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.