Mark Donohue, Managing Director iSky, Global

With mobile now firmly established as the primary banking channel for consumers worldwide, expectations are rising and changing. Customers no longer judge their bank app by the breadth of features it offers, but by how easily it helps them manage everyday money. Simplicity, speed, security and control have become core expectations. People want to understand what is happening with their money at a glance, act immediately when something doesn’t look right, and feel confident they can get things done digitally without friction, escalation or unnecessary effort.

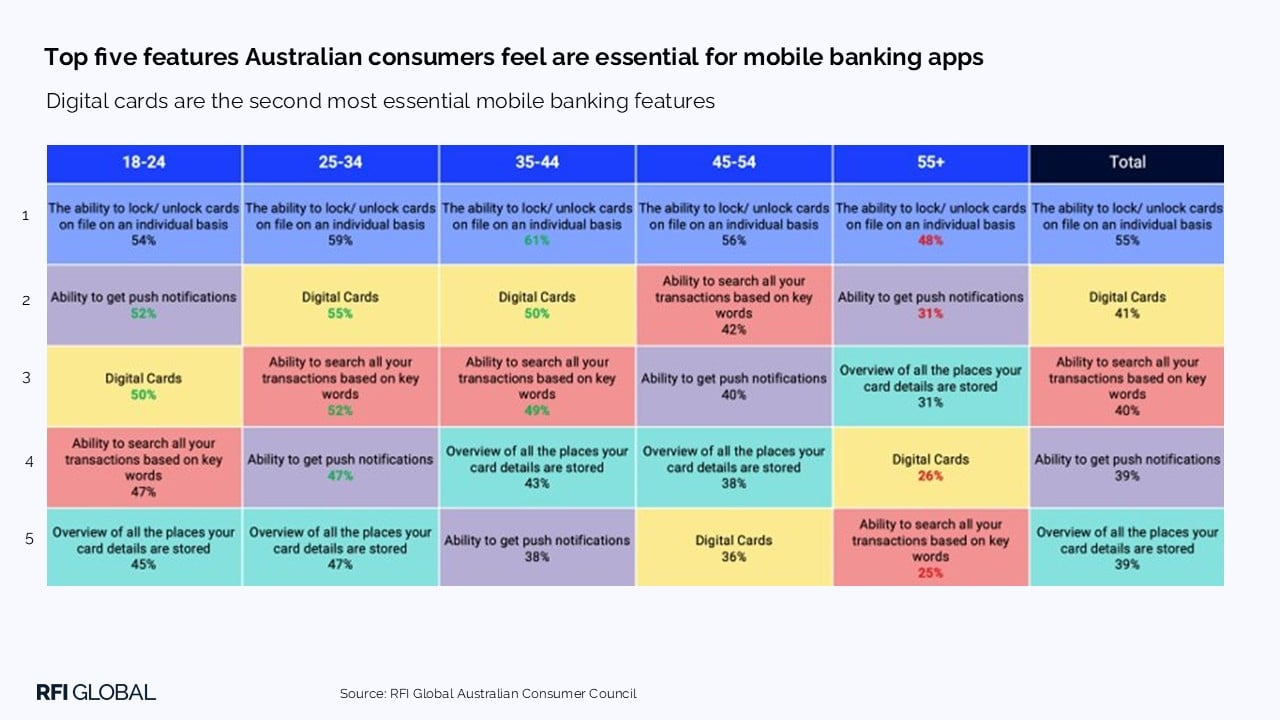

As the number of mobile app features increases, consumers are asking for simple, secure ways to stay in control.

This prioritisation comes through clearly in our data. In Australia, security and card locking features rank as the most important elements of the banking app experience. Interestingly, though, digital cards follow closely in second position, with 41% of Australians ranking them, a figure that rises to 50-55% amongst those aged 25-44. And that is just the number of people who say digital cards are essential. A further 35% say it is preferable – highlighting substantial latent demand as awareness and availability increase.

Availability of virtual cards varies significantly by market. Our iSky Radar platform shows that across key markets, just 13% of banks currently offer virtual cards. The number rises to around two in five banks in Indonesia and Thailand, followed by the UK at around one in four. This is not just digital-only banks; incumbent banks also offer virtual cards, often initially as one-off features rather than fully integrated controls. Some banks are treating virtual cards as distributable permissions, enabling customers to issue cards instantly for specific purposes or people. Others are layering in time-bound and conditional rules, so cards expire automatically or pause when a threshold is crossed.

Despite a strong appeal, adoption remains relatively low

Mobile wallets are widely used in many markets, reaching near-universal use in parts of APAC. However, the use of virtual cards is currently much lower. In Australia, 42% of consumers use a digital card, rising to 71% for under 25’s. At the end of 2023, around a quarter of UK consumers (23%) had ever used a virtual card. Uptake in Canada and Asia is particularly low, with usage at 3% in Canada, 5% in Indonesia, 4% in Singapore and 2% in Malaysia. This gap is not a reflection of limited relevance, but of limited awareness and inconsistent execution. In many markets, virtual cards have not yet been clearly positioned or fully integrated into the everyday banking experience (e.g. as a proposition that may overlap with but is not exclusively linked to virtual wallet usage).

As awareness improves and implementations become more intuitive and better integrated, these figures are likely to rise quickly, driven by the everyday convenience, flexibility and security that virtual cards offer.

The value of virtual cards

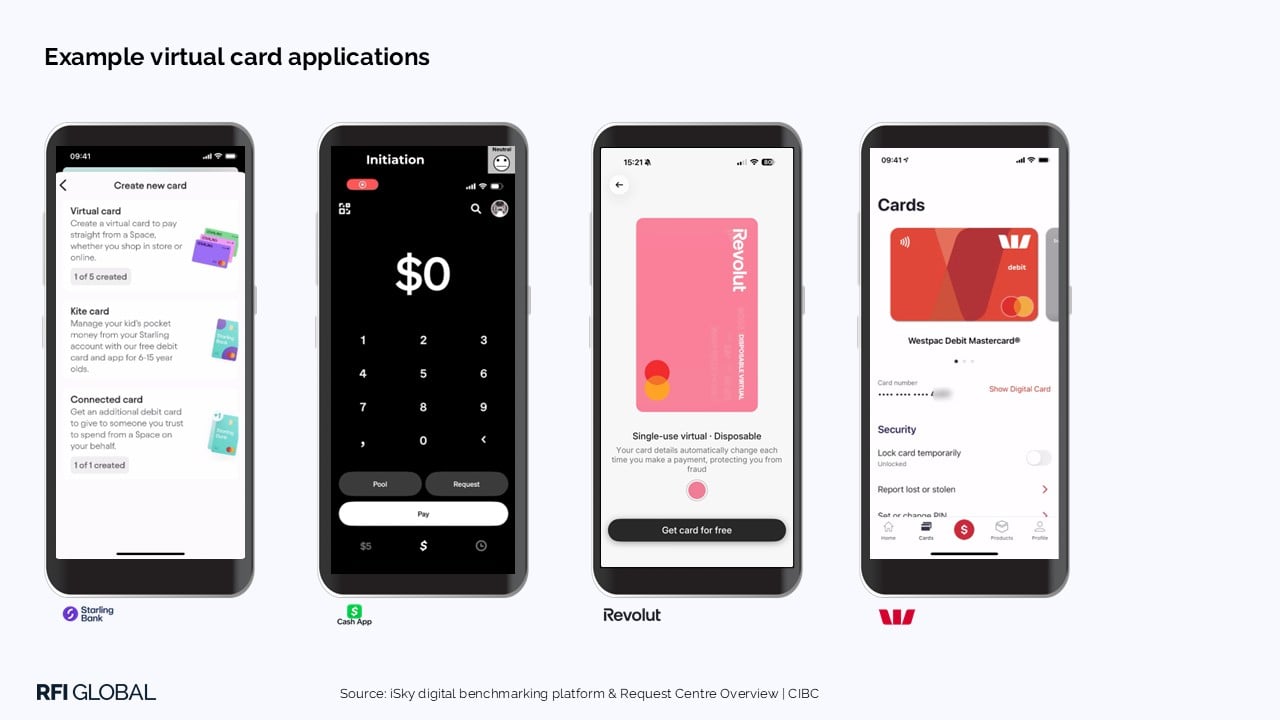

We see some great examples of virtual cards through our iSky Radar platform. Global, regional and local banks providing solutions that give customers flexible, situational access to money that can be issued, adjusted or withdrawn instantly, without disrupting their wider account.

Cards for family and friends

Sharing access to money has traditionally been slow and inflexible, requiring physical cards or account transfers. Virtual cards remove this friction. Customers can instantly issue cards to family members or trusted third parties, with predefined limits and controls. Digital-only UK bank Starling provides a great example of this, with its Kite Card, where customers can manage their kids’ pocket money from their Starling account with a free virtual debit card and app designed for 6-15-year-olds.

Easy oversight and control

Customers expect to see every card, every user and every transaction in one place, with instant actions to pause, restrict or revoke access. This visibility ensures confidence even as cards are handed out more freely and frequently for different use cases.

Virtual and customisable

Our research shows that more than half of Australian customers now leave home without their physical card, relying on wallets and in-app credentials. In response, leading apps surface virtual card details on demand, allowing temporary exposure of sensitive information, and supporting custom naming and rules, positioning the app, not the plastic, as the primary card experience.

Cash App demonstrates this well, allowing customers, including children, to personalise virtual cards visually, reinforcing both ownership and engagement.

Cards for gifts

Virtual cards remove friction from gifting and one-off use cases, allowing money to be issued instantly, used immediately and controlled digitally without physical handover. Recipients can either spend the value as a gift card or deposit it into a new account, with a small incentive encouraging conversion, and a potential referral opportunity.

Increasing security

Virtual cards also enable stronger security models. By separating credentials from the primary account, customers can limit exposure to fraud without needing to cancel or replace their main card. Single-use or disposable cards further reduce risk by regenerating details after each transaction. Physical cards should be void of digits to make them more secure. If there are no digits on a card, there is nothing that can be used in fraud.

Cards that exist in the virtual space do not need to expire in the same way, reducing replacement, production and mailing costs while supporting sustainability goals.

Revolut offers a single‑use disposable virtual card, with card details changing on every transaction to protect customers from fraud. This approach reduces exposure without adding friction, particularly for online and international spending. In recognition of its broader digital execution, Revolut was awarded Best Consumer iPhone App and Best Business Banking App (non‑Big Four) at RFI Global’s Australian Banking & Finance Awards 2026.

What’s next for virtual cards?

Availability and adoption of virtual cards remains modest in many markets, but that gap in usage vs appeal highlights a significant opportunity rather than a lack of demand.

As modern spending becomes more fragmented across subscriptions, online merchants, family use and one‑off purchases, each with a different risk profile, the limitations of a single, permanent card become increasingly clear. Virtual cards introduce precision, allowing customers to match how they pay with what they are paying for.

For customers, this provides reassurance and flexibility, allowing money to be accessed and shared safely while keeping core account details protected. For banks, virtual cards offer a more efficient model, reducing fraud, cutting the cost of plastic and delivery and supporting sustainability commitments.

As awareness grows and communication improves, virtual cards are well‑positioned to become a foundational element of digital banking in 2026 and beyond, offering providers a powerful way to differentiate their mobile experiences while meeting evolving customer expectations.

To learn more about how banks around the world are implementing virtual cards, and to explore best practices based on thousands of banking app evaluations, get in touch to find out more about RFI Global’s iSky Radar platform.

Mark Donohue

Managing Director iSky, Global

Mark Donohue is Managing Director of iSky at RFI Global, working with clients globally on data-led financial services intelligence.

View full profileFrequently asked questions about virtual cards

Q: What is a virtual banking card and how does it work?

A virtual card is a digital card created within a banking app that can be used for specific purposes or for use by nominated people. Unlike a physical card, a virtual card can be issued instantly, paused, replaced or removed without disrupting the customer’s main account details. Virtual cards may be used on their own or added to a mobile wallet.

Q: What is the difference between a virtual card and a mobile wallet?

A mobile wallet is a way to pay using an existing card or account through a smartphone or wearable device. A virtual card, by contrast, allows customers to create separate cards within the banking app for different purposes, such as subscriptions, family spending or one‑off purchases. While a virtual card can be added to a wallet, it does not have to be, and its primary value lies in control rather than convenience alone.

Q: Why are banks offering virtual cards?

Banks are introducing virtual cards to meet growing customer demand for security, flexibility and control in mobile banking. Virtual cards reduce fraud exposure, lower the cost of producing and mailing plastic cards, and support sustainability goals by reducing reliance on physical materials. For banks, virtual cards reduce costs by reducing fraud, customer support needs, and card replacements.

Q: Are virtual cards widely used today?

Usage of virtual cards remains relatively low in many markets compared with mobile wallets. By the end of 2023, around 23% of UK consumers had ever used a virtual card, while uptake in parts of Asia was much lower, at 5% in Indonesia, 4% in Singapore and 2% in Malaysia. This gap reflects limited awareness and inconsistent execution rather than a lack of customer relevance, suggesting significant growth potential as understanding and integration improve.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.