Jackie Greig, VP Marketing, Global

Over the past decade, the way we pay has undergone a quiet revolution. What began with the introduction of mobile wallets in the early 2010s, followed by the rapid rise of Buy Now, Pay Later (BNPL) adoption, has evolved into a global shift in how consumers think about, choose and use payment methods.

Today, consumers are no longer limited to just cash or cards. They’re tapping phones, splitting payments, and deferring purchases with a growing array of digital options. This increased choice has not only changed the checkout experience, but it has also reshaped consumer expectations, loyalty, and financial behaviour. Payment preferences are diverging across borders and generations.

As the payments landscape becomes more fragmented and personalised, understanding these behavioural shifts is essential for anyone looking to stay ahead in the global financial ecosystem.

Payment trends: How do people pay around the world?

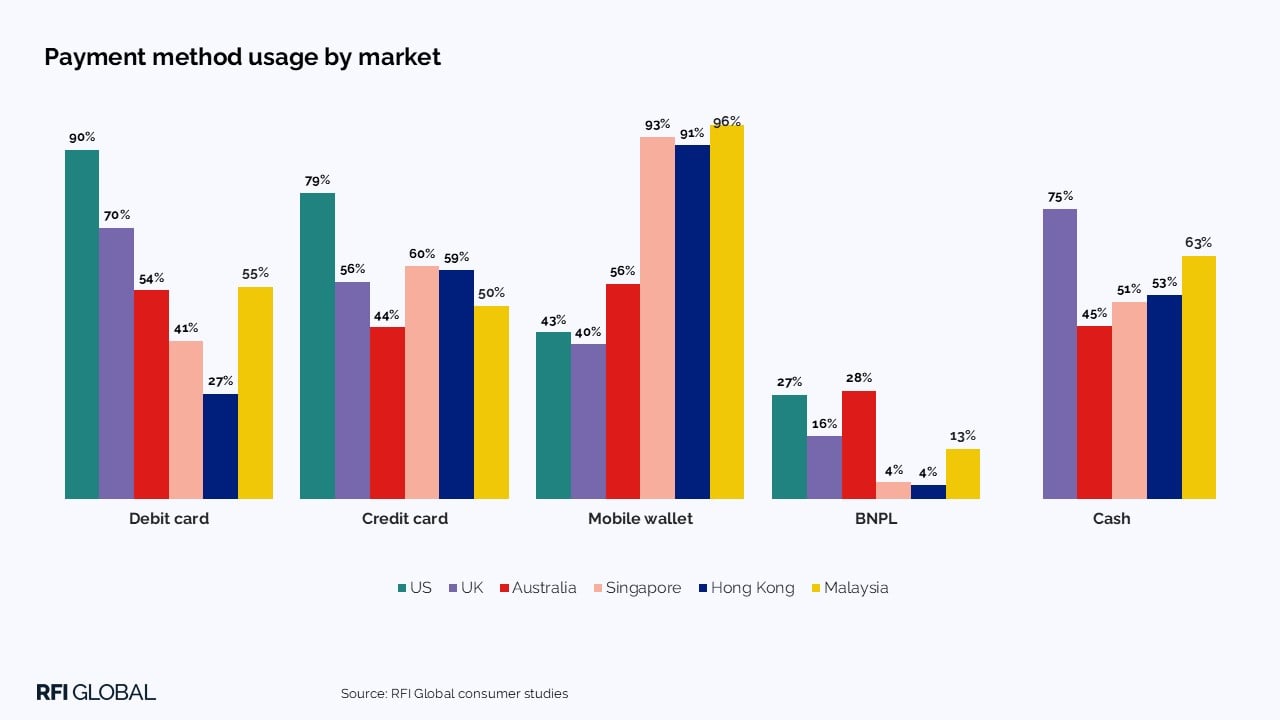

The way people adopt and use payment methods varies significantly across markets, shaped by infrastructure, regulation, consumer habits and digital maturity.

In Southeast Asia, cards remain highly popular due to their attractive perks and benefits. At the same time, mobile wallet usage is nearly universal. In Malaysia, 96% of consumers use mobile wallets, followed closely by Singapore (93%) and Hong Kong (91%). This widespread adoption is driven by mobile-first ecosystems, robust domestic and cross-border QR-code infrastructure and the efforts of major regional players such as Alipay and WeChat Pay.

In contrast, the United States remains anchored in more traditional formats. Debit card and credit card usage is high, used by 90% and 79% of households, respectively. Mobile wallet adoption, while growing, still lags at 43%. In recent years, Buy Now Pay Later (BNPL) has made huge inroads in the US, with over a quarter (27%) of households now using it, having nearly doubled over the past two years.

The UK presents a mixed picture. While mobile wallet usage is lower than all other markets (40%), cash remains surprisingly resilient, with 75% of consumers still using it regularly. Debit cards are widely used (70%), but BNPL and mobile wallets have yet to reach the levels in other markets and may not with the UK government’s crackdown on buy now, pay later providers earlier this year.

In Australia mobile wallet usage has overtaken credit cards (56% vs 44%), and debit cards remain strong at 54%. BNPL is widely used (28%), especially among younger consumers.

Generational payment preferences

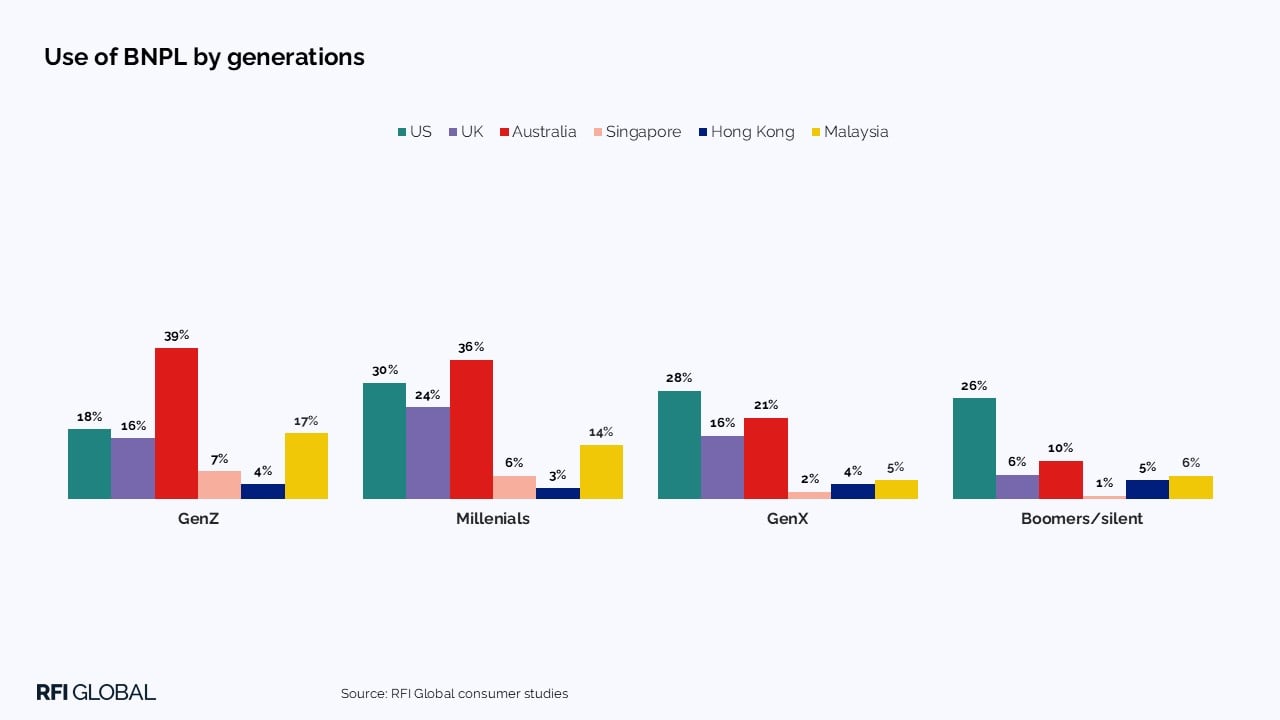

Millennials are the most diversified users, embracing both traditional and emerging formats. They are confident with credit, keen users of BNPL, and highly engaged with mobile wallets. In Australia, BNPL usage among Millennials reaches 36%, and mobile wallet penetration is strong across APAC. However, in Western markets like the US and UK, mobile wallet usage is slightly lower than Gen Z, indicating a generational shift toward mobile-first behaviour.

Gen Z: Mobile-first, budget-conscious

Gen Z are digital natives, but their payment behaviour often reflects caution and control. They favour mobile-first formats and are the heaviest users of mobile wallets across all regions. They are less likely to use credit cards than other generations. Their use of BNPL varies significantly by region. In the UK and US BNPL usage is significantly lower than Millennials and Gen X (US 18%, UK 16%), but in Australia, they top the generations at 39%.

Millennials: Digitally fluent and financially active

Millennials are the most diversified users, embracing both traditional and emerging formats. They are confident with credit, keen users of BNPL, and highly engaged with mobile wallets. In Australia, BNPL usage among Millennials reaches 36%, and mobile wallet penetration is strong across APAC. However, in Western markets like the US and UK, mobile wallet usage is slightly lower than Gen Z, indicating a generational shift toward mobile-first behaviour.

Gen X: Balanced and pragmatic

Gen X shows a similar profile to Millennials, using both traditional and digital payment methods. They maintain high usage of debit and credit cards, and BNPL adoption is notable, especially in Australia (21%) and the US (28%). Their mobile wallet usage is strong in APAC (93% in Singapore), but more moderate in Western markets.

Boomers and the silent generation: Traditional and resilient

Older consumers continue to rely on familiar formats, credit cards and cash, though mobile wallet usage is still high in Asian markets (93% in Malaysia, 83% Hong Kong, 80% Singapore). Outside APAC, their behaviour reflects stability and simplicity, with slower adoption of BNPL and lower mobile wallet penetration.

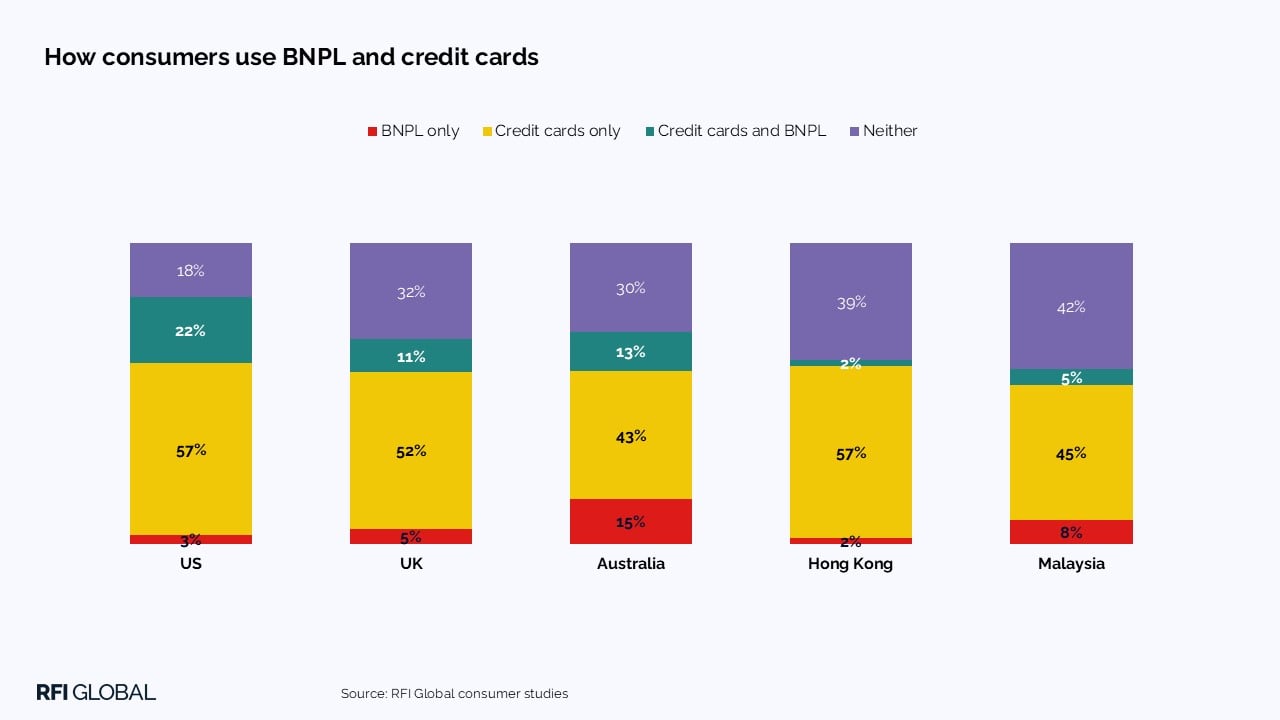

Is BNPL adoption cannibalising credit cards?

The relationship between BNPL and credit cards also varies significantly by market. While BNPL is often used alongside credit cards in most regions, Australia stands out as an exception, where BNPL has often replaced credit cards rather than complemented them (15%). Credit card issuers have launched instalment plan options in response.

In the United States, BNPL is more often used in conjunction with credit cards, but it’s still eating into their share of spend. Among households using both formats (22%), the proportion of spend going to credit cards has dropped from 70% to 58% since 2022. That’s a $279 per household decline in just two years, highlighting BNPL’s growing influence on consumer wallets.

BNPL adoption varies by generation and market. While younger consumers show strong uptake in Australia, in other markets like the US and UK, older generations are also active users, suggesting that BNPL is not exclusively a youth-driven trend.

Who’s winning BNPL share?

BNPL provider use differs significantly by market. Australia is dominated by Afterpay (41%), PayPal in 4 (30%) and Zip (22%). In the UK, Klarna is the most popular provider (13%), followed by Clearpay (11%). Usage is more fragmented in the US, with the main providers as Affirm (9%), Afterpay (8%), Karna (7%), PayPal in 4 (6%) and Synchrony (5%)

What the fragmented future of payments means for providers

The global payments landscape is more fragmented than ever. From the near-universal adoption of mobile wallets in Southeast Asia to the enduring dominance of debit and credit cards in the US, consumer preferences are shaped by a complex mix of infrastructure, culture and generational habits.

BNPL has emerged as a powerful disruptor, but its role varies sharply by market. In Australia, it’s replacing credit cards for many consumers, while in the US, it’s steadily eroding card spend among those who use both. Yet in other regions, BNPL remains a complementary tool or a niche offering.

Generational differences add another layer of complexity. While younger consumers are often assumed to be driving digital adoption, the data shows that older generations are also active users, particularly in markets with strong mobile infrastructure. Behavioural shifts are not just generational; they’re contextual.

As payment options continue to expand, the challenge for providers is not just to offer more choice, but to understand how, when, and why consumers choose one method over another. Loyalty is no longer guaranteed. The winners will be those who deliver seamless, secure, and rewarding experiences, tailored to the needs of each market and each generation.

Want more insights about the future of payments?

Our global surveys track payment behaviour across markets and generations. If you’re looking for further insights into the payments landscape, get in touch, we’d love to help.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileFrequently Asked Questions

Q: How are payment preferences changing around the world in 2025?

A: Payment habits are becoming more digital, with mobile wallets dominating in APAC, while cash and cards still play a major role in markets like the UK and US.

Q: Is Buy Now, Pay Later (BNPL) replacing credit cards?

A: In some markets like Australia, BNPL is replacing credit cards, especially among Gen Z. In others, like the US and UK, it is more often used alongside traditional cards.

Q: Which generation uses mobile wallets the most?

A: Gen Z leads mobile wallet adoption globally, driven by mobile-first habits, but even Boomers show high usage in Southeast Asia.

Q: What payment methods are most popular?

A: The way people adopt and use payment methods varies significantly across markets, shaped by infrastructure, regulation, consumer habits and digital maturity. Mobile Wallets are near-universal in Southeast Asia, the US favours debit and credit cards, the UK still leans on cash, and Australia is shifting toward mobile wallets and BNPL, especially among younger consumers.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.