Jackie Greig, VP Marketing, Global

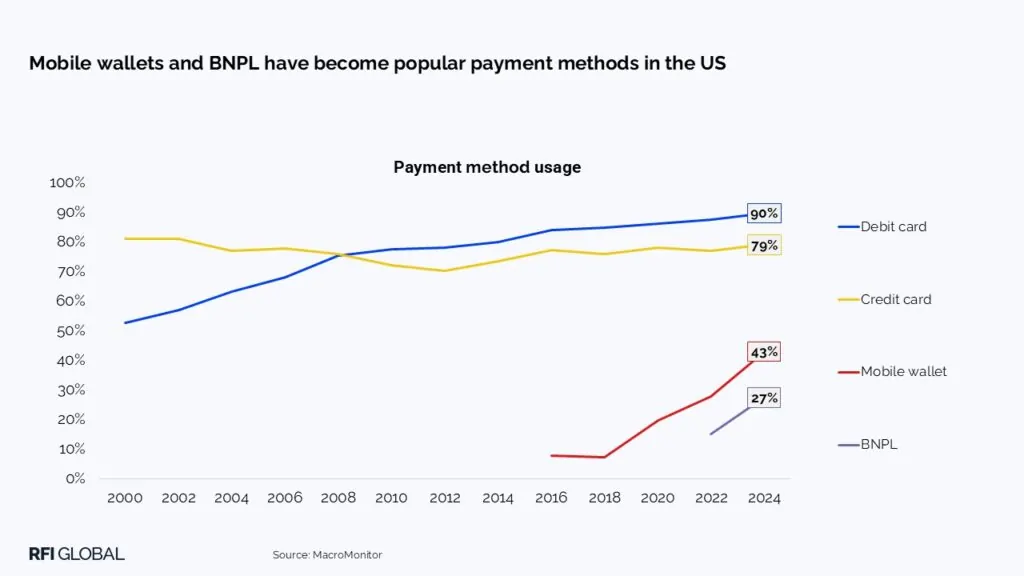

Credit card adoption in the US has steadily rebounded since 2012 following a dip after the 2008 financial crisis. Today, 79% of households hold at least one card, with an average of 3.8 per household. The average balance, after years of decline, is rising again, now at $3,080.

However, our latest MacroMonitor data signals a turning point. While traditional credit cards still dominate, newer forms of payment like Buy Now, Pay Later (BNPL) and mobile wallets are gaining traction and reshaping the competitive landscape.

BNPL usage has nearly doubled over the past two years, now used by 27% of households, and 43% regularly use mobile wallets.

Consumers are turning to BNPL for far more than big-ticket items. From everyday expenses like groceries to luxury items, travel, vet bills, and even concerts. At Coachella, an iconic music festival for young consumers, an estimated 80,000 to 100,000 fans used BNPL to attend this year’s event, accounting for a staggering 60% of tickets sold. The program launched in 2009 to make Coachella more accessible to a broader audience. This year’s record-breaking number of payment plans reflects a broader cultural and economic trend driven by the rising cost of entertainment.

Consumer attitudes towards BNPL

While BNPL is gaining traction, consumer attitudes reveal a mix of enthusiasm and caution. Over half of US households view it as a convenient payment option (58%), and many see it as a helpful tool to access items they couldn’t otherwise afford (46%). But concerns run deep—77% believe BNPL encourages people to take on more debt, and 65% say they’d rather use traditional credit cards or pay with cash. The message is clear: BNPL is valued for its flexibility, but trust and financial literacy will be key to long-term adoption.

Beware the BNPL cannibal

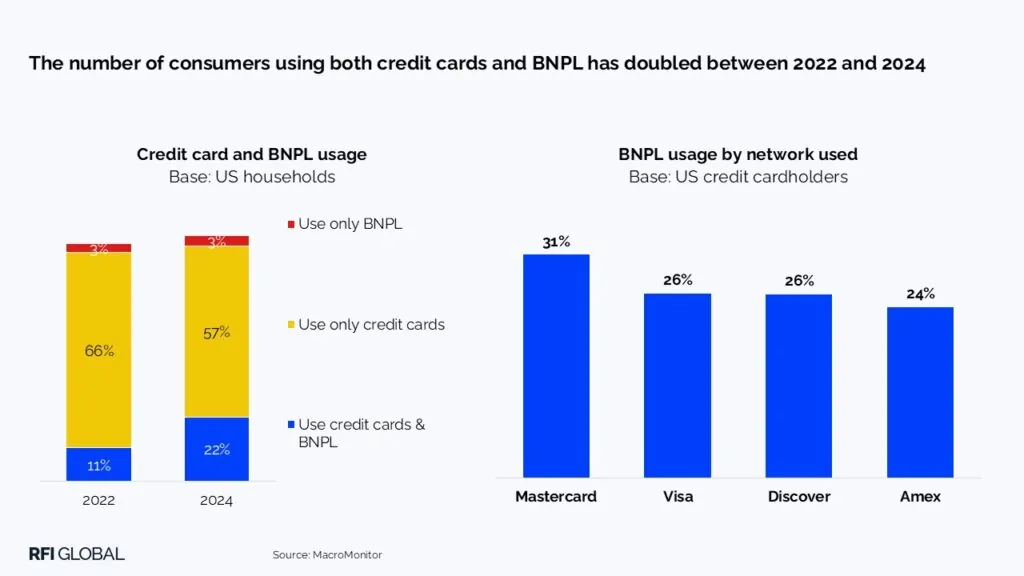

What’s telling is the impact of BNPL on share of credit. BNPL is rapidly becoming a complementary and competitive option, and it is cannibalizing credit card spend. Among households using both BNPL and credit cards (now 22%), the share of spend going to credit cards has dropped from 70% to 58% since 2022. That’s a $279 per household decline in just two years.

The most frequently used BNPL brands in the US are: Affirm (10%), Afterpay (8%), Klarna (7%), PayPal Pay in 4 (6%) and Visa Instalment Credit (6%). Big players are also entering the BNPL space. After piloting Instalment Credit in 2019, Visa is now gaining a foothold with established BNPL players.

BNPL solutions are especially popular among Mastercard customers, with nearly a third (31%) using them. Mastercard could do more to encourage customers to use their service, while 31% of their credit card customers use BNPL, only 4% of US households and 6% of Mastercard’s credit card customers use instalment credit.

And while only a small minority (3%) relies solely on BNPL, it’s clear that BNPL is now a serious competitor and complement to traditional credit.

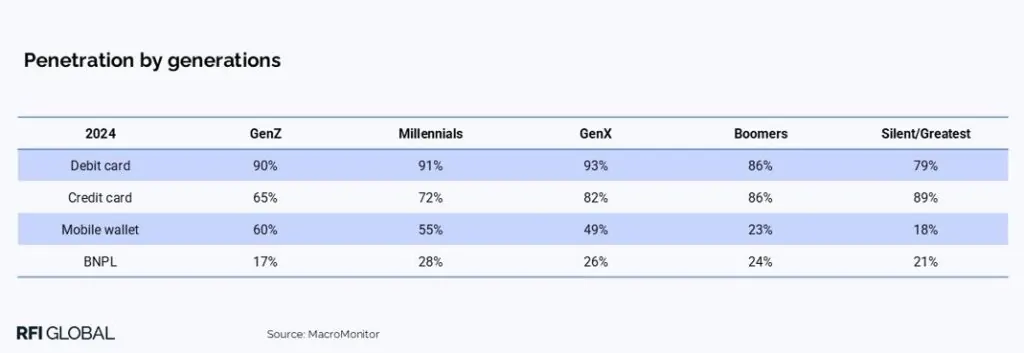

Gen Z is going mobile, but BNPL is for everyone

Mobile wallets are gaining particular traction among Gen Z, with 60% using them regularly. Credit cards still dominate for older cohorts, and BNPL usage is fairly consistent across generations, but less so amongst the youngest and oldest cohorts. For providers, the battleground is no longer just about issuing cards, it’s about relevance across all payment moments.

Stay top-of-wallet

With households juggling multiple credit cards and the growth in mobile wallet use, there is a clear opportunity to capture primary card status. Our data shows that amongst the top 10 credit card providers, only between a third and half of their card-holding customers use their card most often. Capital One and Chase lead the loyalty race, with half of their customers using the card most often.

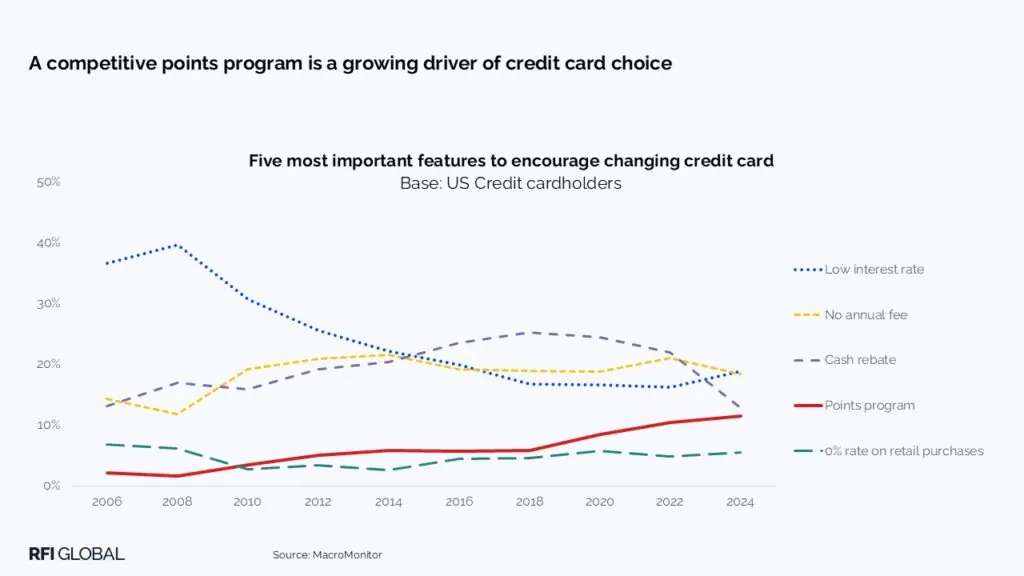

To win and retain top-of-wallet position, card issuers need to deliver on what matters most to their customers. Our data shows that practical, everyday value continues to drive card choice and loyalty. Nearly half (46%) of households say no annual fee would be enough to make them switch, followed closely by a low interest rate (35%). But rewards still pack a punch—29% would switch for a strong points program, and 28% for cash rebates. In a competitive payments landscape, blending low-cost features with compelling rewards is key to staying front-of-mind and front-of-wallet.

Consumers are shopping around

This evolution is happening against a backdrop of growing financial stress. MacroMonitor data shows that more households are struggling to stay ahead and are actively adjusting their behaviors accordingly.

– 78% of US credit card customers are open to switching if offered the right incentives

– 74% say they plan to spend less

– 53% are worried about keeping up financially

This context is crucial. The rise in alternative payments isn’t just about convenience—it’s about flexibility, control, and financial resilience. Consumers are looking for smarter ways to manage cash flow and avoid fees or interest wherever possible. BNPL, in particular, appeals to those seeking predictable payments without revolving debt.

Rewards matter

As highlighted in our Financial Services Trends and Predictions 2025 report, rewards are an important lever for building customer loyalty.

This remains true for credit cards in the US. Twelve percent of US households now cite rewards as the most important factor in choosing a credit card. While financial incentives such as low fees and interest rates remain critical, rewards programs are becoming a decisive driver of both choice and loyalty.

The customer attrition risk is particularly acute among affluent consumers, where loyalty hinges on incentives like points and travel benefits. Among affluent households, 39% would switch their main credit card if these perks were removed. That number remains high among high-net-worth households too, with 31% saying they would switch if they lost points or travel benefits.

The future of credit cards: Five key takeaways for issuers

In a market defined by high switching rates, multi-card households, and the rapid rise of alternative payment methods, credit card issuers need to rethink how they earn, and keep, a place in consumers’ wallets. The data is clear: loyalty is fragile, and relevance is being redefined. Here are five data-driven takeaways from the trends we’ve observed in our data:

1. Loyalty is earned, not assumed

With 78% of cardholders open to switching for the right incentives and only a third to half of customers using their issuer’s card most often, incumbents can no longer rely on inertia. Winning ‘top-of-wallet’ status requires more than just presence, and the right rewards can help.

2. Rewards matter, but must be tailored

Rewards remain a top driver of choice and loyalty after financial incentives, especially among affluent and high-net-worth segments. Issuers need to personalize rewards to align with customers’ spending patterns and lifestyle needs.

3. BNPL is not a niche, it’s a norm

Buy Now, Pay Later is not just a millennial trend. It’s a mainstream behavior that’s actively cannibalizing credit card spend. Issuers must understand how BNPL fits into their customers’ financial lives and consider how to compete or collaborate with these models.

4. Mobile wallets are the new battleground

Gen Z is leading the charge, but mobile wallet adoption is growing across demographics. Issuers must ensure their cards are not just compatible with, but prioritized in, digital wallets, through seamless integration and smart incentives.

5. Financial stress is reshaping behavior

Consumers are under pressure and responding by shopping around, cutting back, and seeking control. Transparent pricing, predictable payments, and tools that support financial resilience will be key to building trust and long-term relationships.

Explore how MacroMonitor can help you stay ahead of shifting expectations and changing household dynamics.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.