Two things have happened in the last month that have had me thinking about changes in the way consumers make payments. The first is that RFI Global released the 2024 Australian Payments Diary study. Now in its 14th iteration, the Payments Diary is an annual study that provides a fantastic trend analysis of consumer behaviour in what is a rapidly changing market. The second is that I’ve done an unusually large volume of presentations to RFI clients on the topic of payments recently. In some cases, payments generally, in other cases more specific areas of interest within payments, such as credit cards or Buy Now Pay Later (BNPL).

Shifting sands: The future of payments

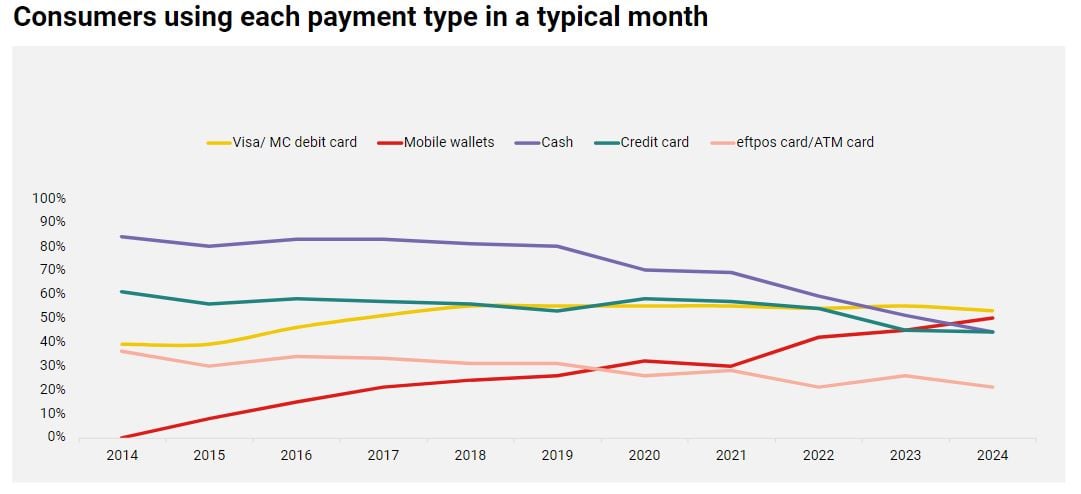

Across both the Payments Diary and my recent presentations, a consistent theme has emerged – the extent to which the entire Australian landscape is shifting. One of my favourite slides from our payments research shows the payment methods consumers use regularly in a typical month.

Over the years we’ve seen regular usage of cash slowly decline and then decline rapidly, to the point where it was overtaken. The thing that struck me this year is that more people now use mobile wallets in a typical month than cash. This might not sound that significant to some, but as recently as 2021, only 30% of Australians used mobile wallets regularly, vs 69% cash.

Note: A consumer can use both a debit card or credit card and a mobile wallet in a typical month. While every mobile wallet transaction is underpinned by one of these cards, it does not negate the usage of each.

Demographics: The driver behind payment evolution

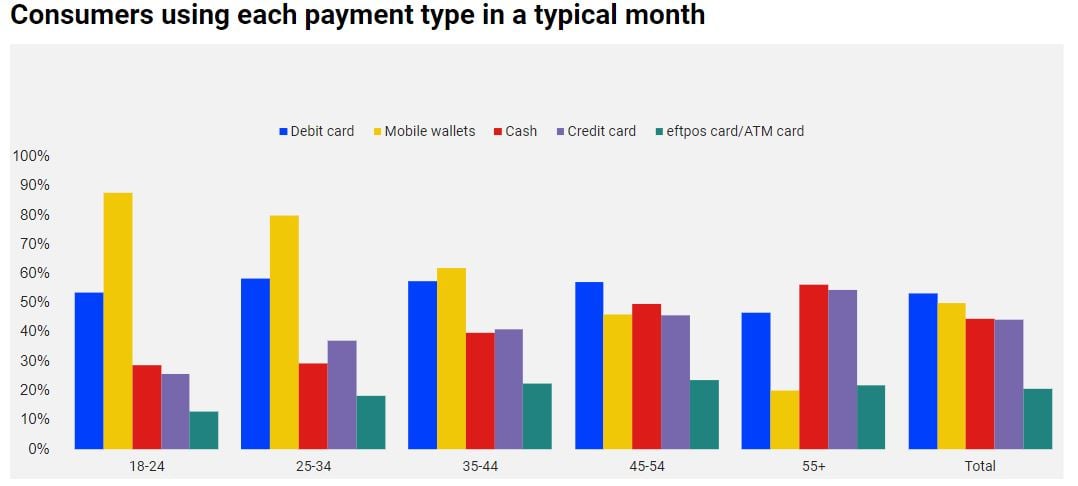

The importance of demographics should not be underestimated. A simple view of 2024 data by age shows that it is younger consumers who are delivering growth for mobile wallets.

What is also interesting is that younger consumers are going to keep Visa/ Mastercard debit card usage going strong – more than 50% of those under 54 say they use the cards regularly, vs 47% of over 55’s – but they are not supporting the continued usage of cash, credit cards and eftpos cards, which represents a problem for those looking to engage consumers with these products.

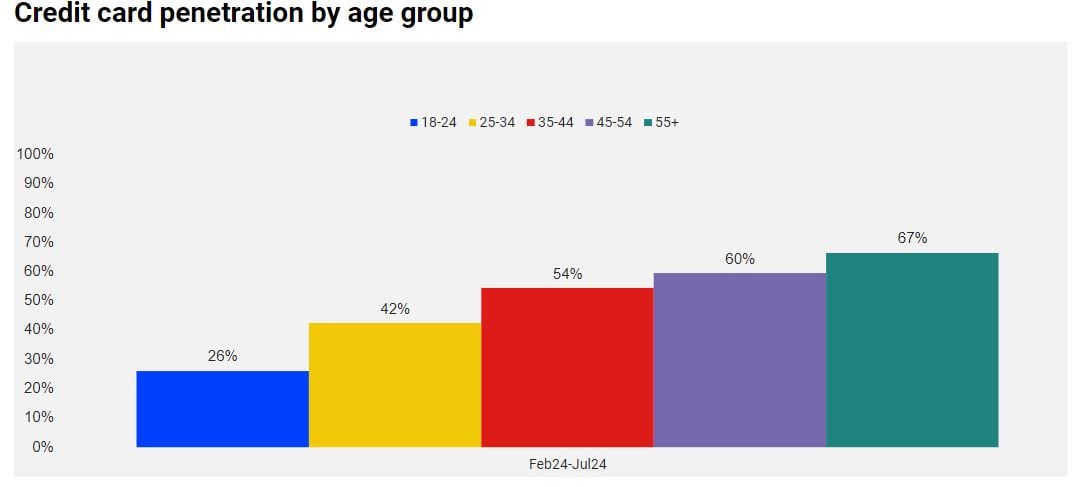

A further negative indicator for credit cards comes in the form of card penetration by age group. RFI’s consumer Atlas data shows that overall credit card ownership has slipped from approximately two-thirds of consumers a decade ago to just over half of all consumers in 2024. Don’t just take our word for it, the RBA’s data shows that the number of personal credit cards on issue peaked at 22.3 million in 2016 and by June 2024 there were just 15.8 million personal cards.

Part of the reason for this is that younger consumers are less reliant on credit cards and many don’t own them. In fact, just 26% of 18-24 year-olds and 42% of 25-34 year-olds own a credit card. If this doesn’t change, then credit card ownership can only continue to fall and at some point, we’ll see a decline in usage.

Volume and value: Statistics covering up the cracks

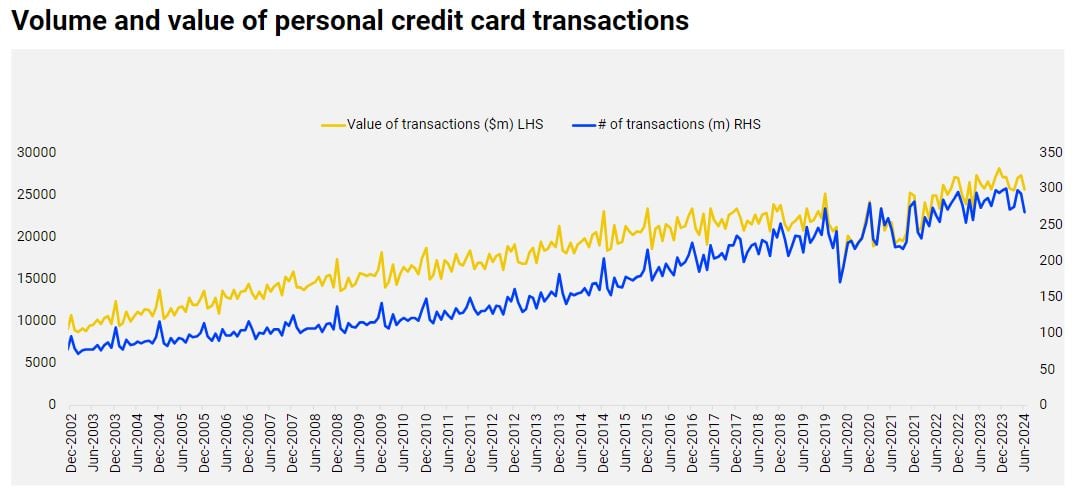

Fortunately for credit cards, we’re still seeing growth in transaction volumes and values. In fact, in June 2024, more than $25 billion was spent across more than 267 million personal credit card transactions. You don’t need to be a statistician to see that over time, both the volume and value of these transactions are growing.

So, a smaller proportion of Australians own a credit card, and the volume and value of credit card transactions are rising. This sounds illogical, but both things can be true at the same time. For starters, there are more people in Australia in 2024 than there ever have been and secondly, the frequency with which credit card holders use their cards is also rising. In fact, the average card was used 17 times per month in June 2024 compared to 7 times in June 2014 and 6 in June 2004.

Consumers are spending more online and have more opportunities to use card-based mechanisms than they ever have in the past. Simultaneously, as we saw, the proportion of consumers using cash regularly has declined significantly, and that spending has migrated to cards.

To me, these growth statistics are covering up the cracks in a credit card proposition that appeals greatly to older consumers (I am one of them) but is less and less relevant to the youth and young adult segment.

What does the future hold for credit cards?

In my last article I talked about the reliance on TikTok and Instagram for information on banking products and services. The conclusion was that banks and card issuers need to go where their customers and potential customers are to engage them.

However, the demographic trends run deeper than mere information and engagement. I believe that credit cards in general have a proposition problem. The proposition does not stack up for newly minted adults and that is a problem that has to be solved if the product category is to continue surviving. Credit cards are not going to die in the next few years, but like cash, the decline will begin, it will be slow and then it will be fast.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.