Jackie Greig, VP Marketing, Global

Onboarding in banking is no longer just the first step in the customer journey. It is the moment that defines how customers perceive a bank, engage with its services and decide whether the relationship is worth deepening.

What was once viewed as an operational process has become a strategic differentiator. Get it right, and banks have the opportunity to build trust, engagement and long-term value from day one. Get it wrong, and the damage is often immediate.

Customers are making this clear in their behaviour. Across markets, ease of opening and setting up an account consistently ranks among the leading reasons for choosing a provider, alongside reputation, customer service and recommendations from friends and family. In many cases, it matters as much as, or more than, rates or rewards.

Onboarding is evolving from a process-led experience to an intent-led one. Rather than simply moving customers through verification and account setup, leading providers are increasingly designing onboarding around what customers are trying to achieve from the outset. Whether it is receiving income, moving money internationally or managing everyday spending, the focus is shifting towards enabling quick outcomes with minimal effort.

It is no longer just about conversion. It is a commercial lever and a clear opportunity to differentiate at the point where customers are forming their first impressions.

Onboarding sets the tone and shapes the entire relationship

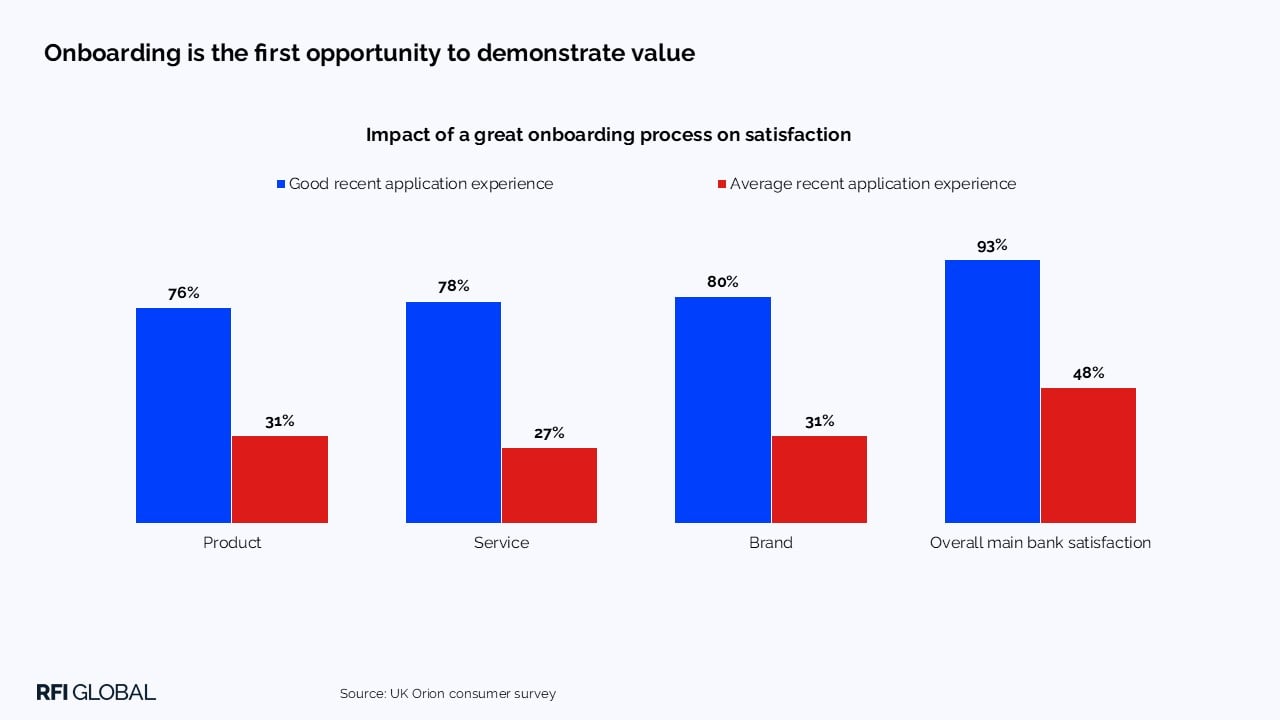

Our analysis of the UK retail banking market shows how strongly onboarding shapes broader perceptions of a bank relationship. Customers who have a positive onboarding experience don’t just feel better about the application process; they rate their entire relationship more highly. A strong onboarding experience also significantly increases product satisfaction and drives higher perceptions of service and brand.

Onboarding creates a halo effect, where a strong start elevates how customers judge every aspect of their bank. The reverse is also true. A poor onboarding experience sets a negative tone that can be difficult to shift.

It explains why providers like Revolut continue to stand out. Its streamlined onboarding, combined with a strong mobile experience, reinforces its value proposition from the outset rather than after the relationship has been established.

Ease of account opening is a global driver of choice

Onboarding also plays a clear role in the providers consumers choose. Across six markets, convenience and ease of setting up an account rank among the most important drivers of choice. In the UK, it is the number one reason consumers choose a provider. In Singapore, Hong Kong and Malaysia, it sits firmly within the top three. Even in markets where other drivers are particularly strong, such as Australia, it remains a top-tier factor.

Onboarding actively influences acquisition. Customers are not just comparing pricing or features, but also how easy they expect it will be to get started. Digital‑first providers have raised the bar for what good onboarding looks like. Simplicity and speed are now expected as standard.

In the US, 19% of consumers opened a new bank account in the last two years, and 14% of Canadians are looking to open new accounts in 2026. In markets such as the UK and Australia, these levels are lower, but the absolute number of new accounts remains significant.

That creates a steady flow of customers at the point where experience matters most. Every interaction is an opportunity to make a strong first impression.

Satisfaction with onboarding

Banks have improved onboarding over time. Across markets, around three-quarters of customers are satisfied with their onboarding experience. Satisfaction is highest in the UAE (83%) and lowest in Canada (62%). Digital‑only providers often outperform traditional banks that have streamlined onboarding and reduced friction. In Malaysia, we see 84% satisfaction with digital-only providers vs 66% for traditional banks.

But what about the quarter that aren’t satisfied with their onboarding? And those who didn’t proceed in opening the account and went elsewhere due to the friction they faced?

Redefining the role of onboarding

Customers are not opening accounts for the sake of onboarding itself. They are trying to achieve specific outcomes, whether receiving salary payments, managing money internationally or accessing funds quickly. This creates an opportunity for banks to guide customers towards meaningful actions early in the relationship and introduce relevant services at the moment they are most useful.

Rather than a process to complete, it is an opportunity for banks to understand what the customer is trying to achieve and to guide them towards meaningful actions. In a digital environment, this is one of the earliest moments where a bank can demonstrate relevance and introduce additional solutions.

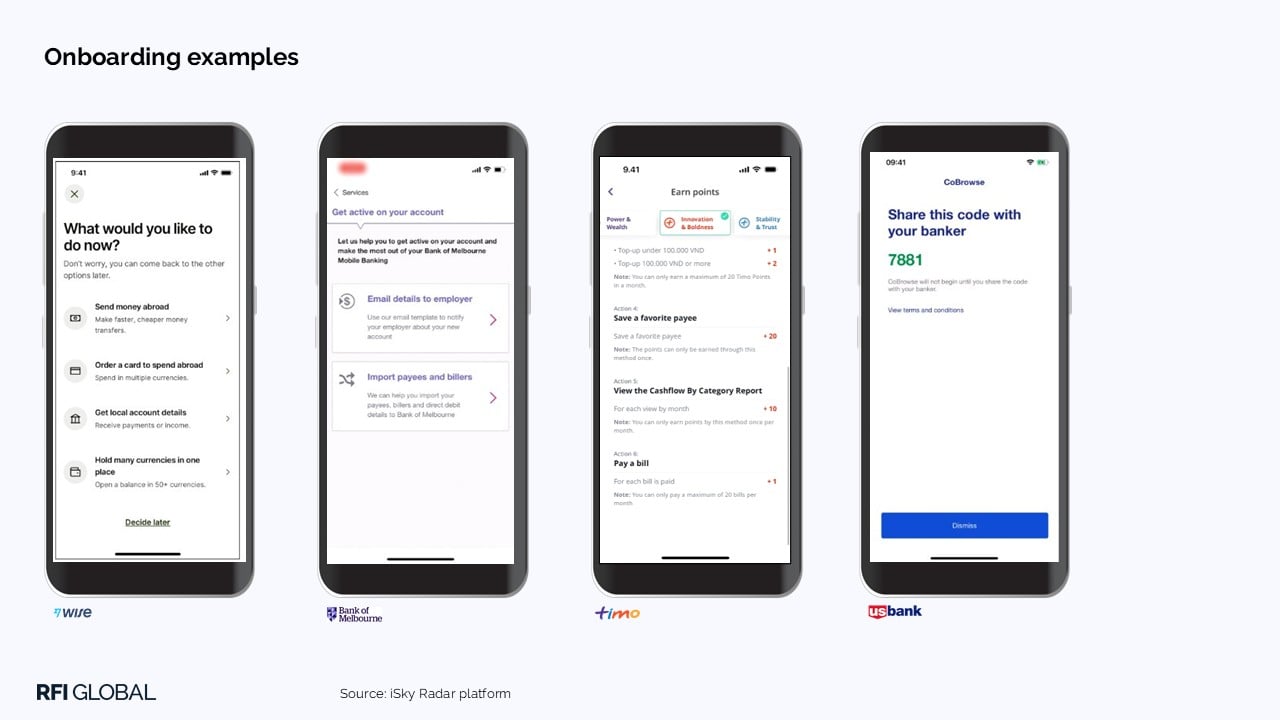

We see from our iSky Radar digital benchmarking platform that some providers are already looking at onboarding as an opportunity for both relationship-building and a growth opportunity. Fintech Wise focuses on customer intent from the outset, asking users what they want to do and guiding them towards completing those actions quickly. One of the first things you see on their website is ‘open an account in minutes’. The Bank of Melbourne addresses one of the most persistent sources of friction by helping customers move key elements of their financial life, such as salary payments and billers, into their new account with simple email templates to use. Timo in Vietnam takes a different approach, encouraging early engagement through clear prompts and simple incentives that guide customers to activate cards, make payments and begin using their account. US Bank and other providers are introducing more direct forms of support, enabling customers to interact with the bank during onboarding, including features such as screen sharing to resolve issues in real time.

While the approaches differ, the underlying principle is consistent. Strong onboarding is not about completing tasks. It is about reducing effort, helping customers get up and running quickly and building a longer-term relationship.

The future of onboarding

In an environment where account switching is easier and expectations continue to rise, the first experience carries more weight than ever before. Onboarding is no longer just the start of the journey. It is becoming one of the most important drivers of competitive advantage in retail banking. It is the starting point for a successful, ongoing relationship and an opportunity to demonstrate value and build trust early.

The institutions that succeed will be those that use onboarding to accelerate engagement, demonstrate relevance and establish trust from the very first interaction. By understanding customer intent early and reducing effort at key moments, banks can create stronger customer relationships and unlock greater long-term value.

Get in touch for further insights from our data on how to strengthen onboarding and early-stage customer engagement.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileFrequently Asked Questions

Q: How important is onboarding in banking?

Onboarding plays a critical role in shaping how customers perceive a bank and influences satisfaction, engagement and long-term relationship value. RFI Global’s research shows that customers who have a positive onboarding experience rate their overall relationship with their bank more highly and report stronger perceptions of service and brand.

Q: How does onboarding influence bank account acquisition?

Ease of opening and setting up an account is one of the most important drivers of provider choice across multiple markets. In the UK, it is the leading reason consumers choose a banking provider, while in markets including Singapore, Hong Kong and Malaysia it ranks among the top factors influencing acquisition decisions.

Q: What is intent-led onboarding in banking?

Intent-led onboarding focuses on helping customers achieve their goals rather than simply completing account-opening processes. Instead of treating onboarding as a series of administrative steps, banks identify what customers are trying to accomplish, such as receiving salary payments, transferring money or managing everyday finances and help them achieve those outcomes quickly and with minimal effort.

Q: How can banks improve onboarding and early-stage customer engagement?

Leading banks and fintechs improve onboarding by reducing customer effort, simplifying account setup, helping customers complete meaningful actions early and providing support when needed. The most effective onboarding experiences establish relevance from the outset, accelerate engagement and build trust from the very first interaction.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.