The importance of trust in an era of increasing fraud – how AI creates greater opportunities for payment providers

Payments are a key line of defence for traditional banks, but the speed and ease of a great customer experience have enabled fintechs to exploit the friction banks had previously created to make significant market share gains. According to RFI Global’s data, 75% of UK consumers who use fintechs or money transfer apps to make payments would switch their main bank compared to 12% of those who don’t use fintechs. Clearly that’s a huge opportunity for fintechs, as well as a potential threat to the banks. This has resulted in the likes of HSBC launching Zing in response.

According to Rupert Lee Browne, founder and chairman of Caxton, this goes to show “how serious banks are about serving their customers.” In our Banking Uncovered podcast, he goes on to say that “banks provide longevity and the ability to withstand market conditions”, “Banks have a significant strength and reliability” and “customers want reliability when they send and receive money.”

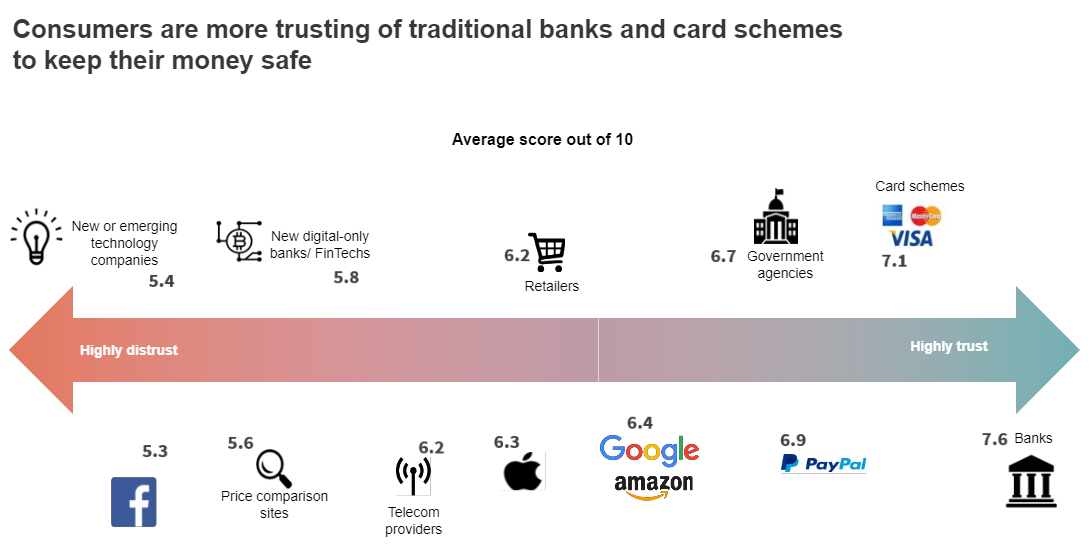

This ties in with RFI data. When asked to define trust, consumers define it as ’keep my money safe‘ followed by ‘keep my personal details private and secure.’ On this metric fintechs have made huge progress since 2015 with trust increasing to 5.8/10 but banks still lead all institutions with 7.6/10.

The impact of fraud

Trust becomes critical as we witness fraud increase dramatically. Rupert says that “In order for the market to operate properly you need to treat your customers fairly”, and some of his competitors have been failing recently in their duty of doing this. This is backed up by the FT which, quoting the UK Payments Systems Regulator, states that Monzo and Starling have some of the highest fraud rates, with Monzo only reimbursing 6% of those who reported fraud compared to 70% for NatWest and 91% for Nationwide.

The issue of fraud and reimbursement will only increase in the UK in October when the liability onus shifts to 50:50. Rupert asks that if car manufacturers aren’t responsible if cars are stolen, is it fair if financial institutions are held entirely responsible for fraud? He does, however, agree and strongly advocates that a culture of honesty and transparency is crucial for any fintech, payments-focused or otherwise, to grow profitably – “it is vital that culture is the bedrock of the business as that creates longevity.”

The dichotomy of the ease, speed and convenience that consumers want, coupled with the increased but opposing need for greater cyber security poses a challenge.

Changing consumer behaviour

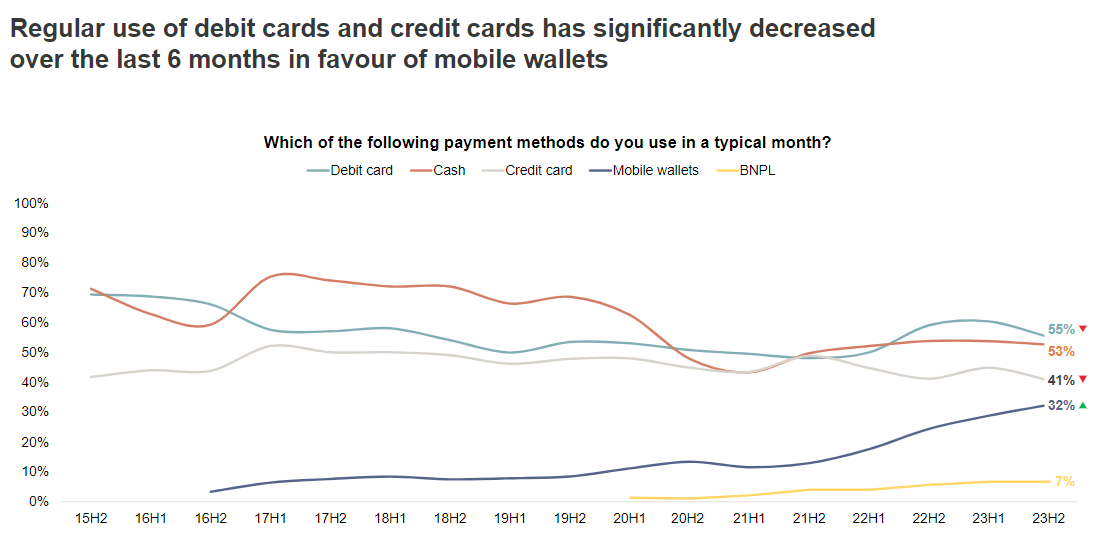

Debit card, cash and credit card monthly usage have all declined in the UK over the last five years down to 55% (debit) 53% (cash) and 41% (credit). At the same time, mobile wallet usage has increased significantly from 0 to 32% monthly usage in the corresponding period.

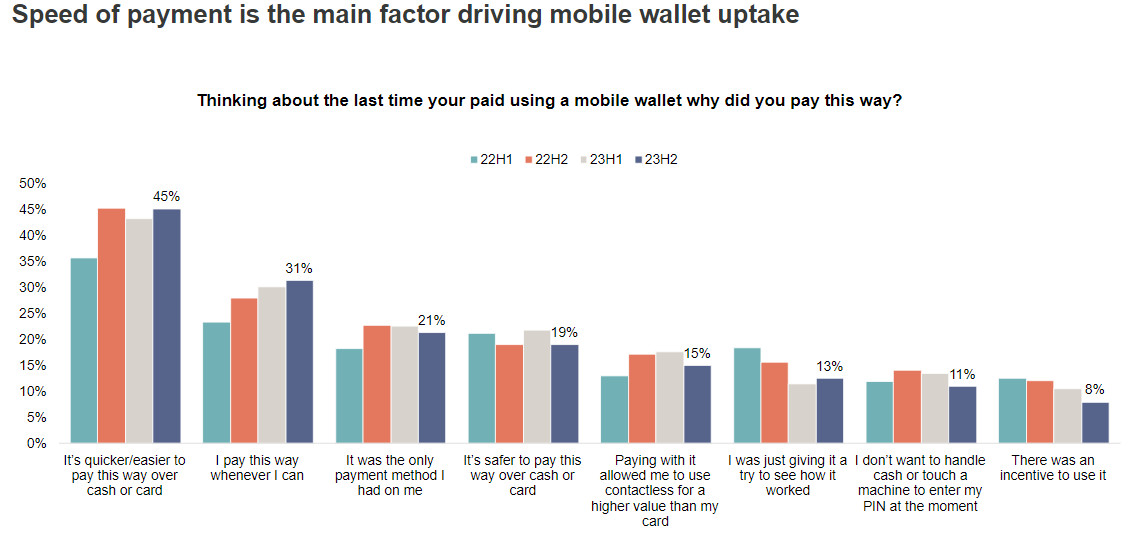

Speed and convenience are the number one drivers of mobile wallet usage.

What about Generative AI?

In the UK Generative AI is increasingly seen by both banks and fintechs as adding huge value to customer experience. Klarna has stated that it has reduced customer wait times from 11 to 2 minutes, replaced 700 staff and added $40 million to its bottom line by using AI for CX. However, Rupert argues that this isn’t the most valuable opportunity that AI creates. AI is a crucial tool in identifying fraudulent or suspicious transactions without causing the consumer pain from the delay in transacting. There is no doubt that AI is already being hugely impactful for fraud detection and transaction monitoring and the speed at which it can do this allows any institution, whether it is an established brand or a fintech, to deliver a fast and convenient payment experience while still providing the security that the consumer wants and needs.

Over the last 10 years we have seen the initial competition and then the co-opetition between banks and fintechs play out with various peaks and troughs for both. While no one is any doubt that the fintechs can provide a great CX and in doing so have forced the banks to up their game in this area, there is also no doubt, corroborated by the data, that banks own the consumer trust index.

Where AI gets exciting is that it allows both parties to leverage their strengths and further address perceived weaknesses by providing a holistic, fast, convenient and secure payment experience. It enhances the ability of traditional banks to provide a fast, seamless and convenient experience and enhances the ability of fintechs to provide a secure and trusted transaction. However, even the best AI applications will ultimately fail to add value if the culture of the business isn’t right – fintech or bank the primary focus has to be on delivering an exemplary CX for the consumer.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.