Mark Donohue, Managing Director iSky, Global

For years, family banking has been treated as a relatively narrow proposition focused on junior savings accounts, pocket money cards and parental controls. That framing is now rapidly becoming outdated. Winning younger banking customers is not just about supporting a children’s account – it’s about securing relevance across the financial lifecycle. Family plays a significant role in banking decisions well beyond childhood, and these early relationships often endure as customers move through adulthood, borrowing, investing and building wealth. A first child account can therefore become the starting point of a multi-decade relationship.

What is emerging is far broader – a connected financial ecosystem spanning parents, children, education, payments, savings, investing and long-term relationship growth.

Evolving expectations in family banking

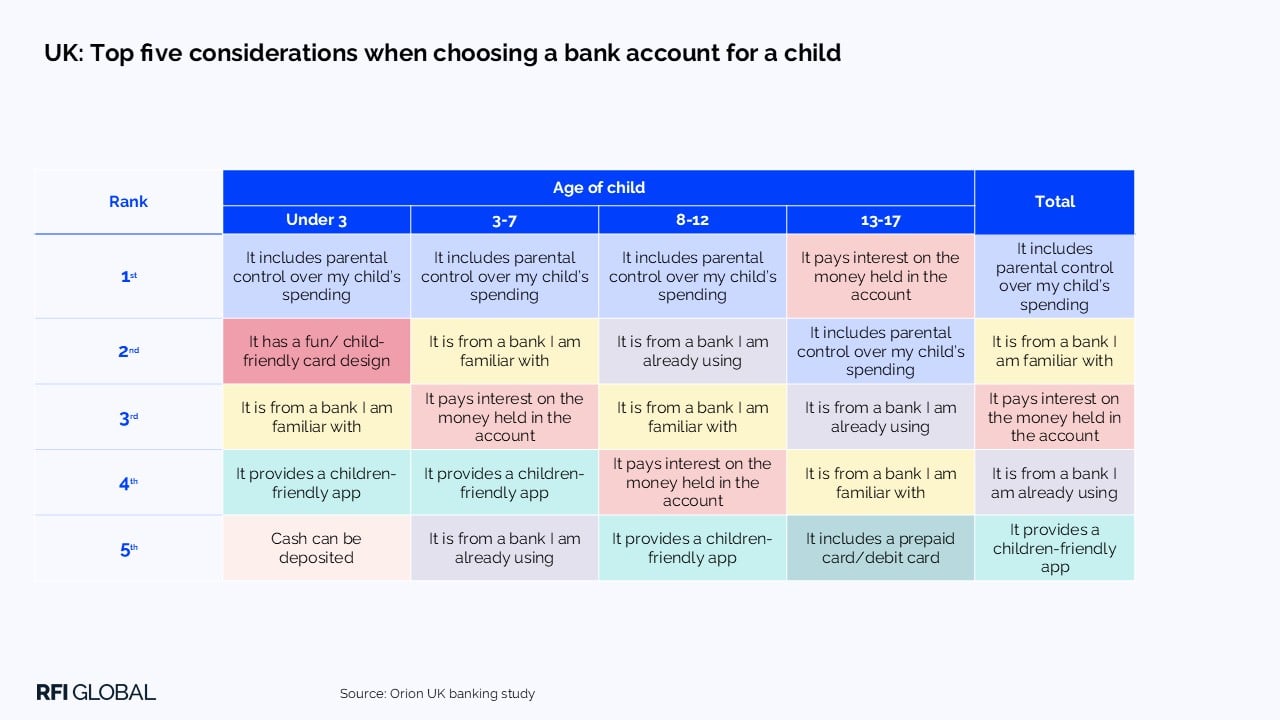

Recent RFI Global analysis across the US, UK and Australia highlights just how materially customer expectations in family banking are evolving. Our research found that parental control over spending remains the single most important factor when choosing a bank account for a child, ahead of areas such as rewards or broader feature depth. Even as the child reaches 13-17, parental concern is still a primary factor, but interest rates rise to the top position. Familiarity with the bank and existing relationships is also critical and highlights the opportunity for providers to build on established.

Our data also shows that app-based onboarding is now the preferred channel for opening an account overall among younger customers and families, reinforcing how central digital-first onboarding and servicing experiences have become within family banking propositions.

Trends in family banking

One of the clearest themes emerging from the market is that oversight and shared participation remain central to the proposition. Parents still want visibility, control and confidence around how younger customers engage with money, but they also increasingly expect children to participate actively in financial decision-making and learning. The strongest experiences, therefore, blend empowerment with governance, allowing younger users to build independence within clear boundaries.

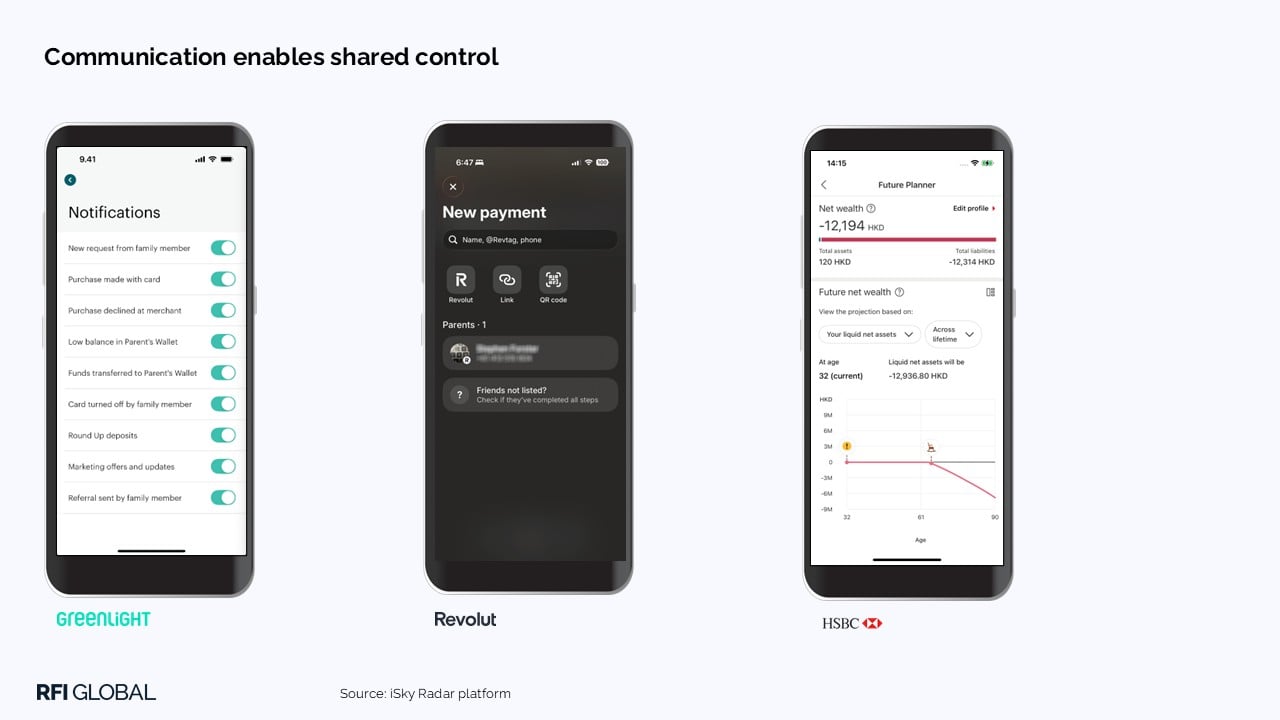

Importantly, digital experience expectations in family banking are now converging with broader retail banking expectations. Customers increasingly expect low-friction onboarding, intuitive navigation, strong security controls, clear communication and practical financial management support. Security itself is no longer viewed purely as a backend function; it has become part of the visible customer experience through features such as granular card controls, permissions management, approval-based payments and security scoring.

We see a strong example of this in the US through Greenlight’s family banking experience, which combines real-time parental approvals, spending notifications and chore-linked payments within a highly simplified interface designed for both parents and children. Similarly, Revolut <18 has focused heavily on gamified saving goals, instant peer transfers and highly visual spending insights to encourage engagement and financial education amongst younger users.

HSBC’s Future Planner focuses on forward-looking financial guidance, helping younger customers understand how their current behaviours shape long-term outcomes and build a clearer path to future financial goals.

Virtual and digital cards are also becoming increasingly important within family banking propositions. Rather than relying on a single shared card, virtual cards allow parents to create separate, purpose-specific cards for different use cases, such as subscriptions, allowances, or one-off purchases. This not only improves oversight and control but also reduces risk by limiting exposure if card details are compromised. More broadly, virtual card functionality creates a more flexible and controlled environment for younger users, enabling participation in digital payments while maintaining clearly defined boundaries set by the parent.

The role of education in family banking

Our research also highlights a major shift in the role of education. Younger customers show the strongest understanding of savings accounts, whilst mortgages remain the least understood financial product amongst surveyed youth cohorts, reinforcing the growing literacy gap as financial complexity increases.

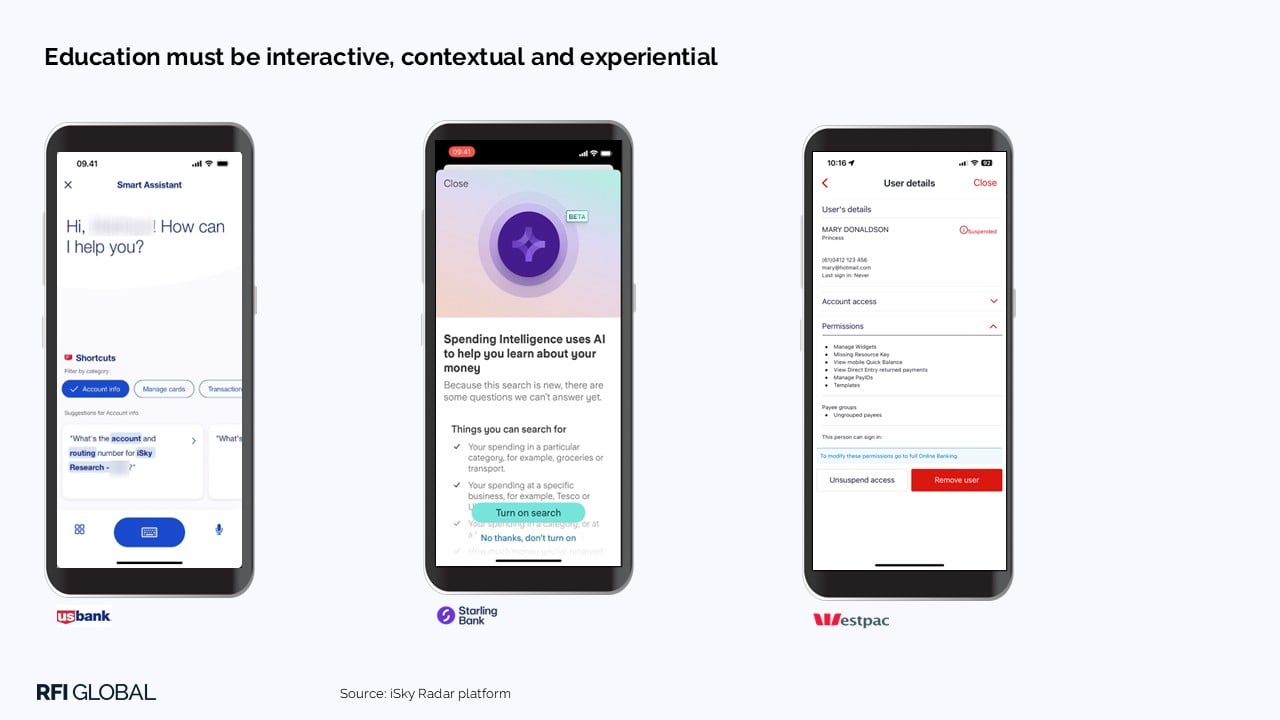

Conversational interfaces, AI guidance, scenario modelling and contextual prompts create a more natural way to build understanding and enable a two-way interaction, with the potential to transform financial learning from passive reading into active participation. The strongest future experiences are likely to combine education, action and real-life money management into one integrated journey.

We’re already seeing examples of banks embedding education tools in the product journey via our iSky Radar platform. US Bank demonstrates how conversational interfaces can create more interactive, two-way learning, while UK digital-only bank Starling introduces AI-driven spending insights to help customers understand behaviour in real time.

Another important trend is the expansion of family finance beyond simple savings products. Increasingly, providers are introducing investing functionality, family hubs, custodial structures and shared financial visibility designed to support multi-generational wealth building. Neo-banks and fintechs are moving more aggressively into this space, but incumbents still retain significant structural advantages where they successfully connect household relationships across banking, servicing, oversight and communication. Westpac in Australia provides a good example of this. Its Family Hub brings together spending limits, pocket money and activity tracking, helping households manage and guide younger users’ financial behaviour within one shared environment.

The future of family banking

Ultimately, the strategic value of family banking extends well beyond the child account itself. A meaningful share of adult banking relationships still originates through family influence or accounts opened at a young age. That means family banking should not be viewed as a short-term acquisition exercise, but as the foundation of a multi-decade customer relationship.

The institutions that succeed in this space will likely be those that stop thinking about family banking as a standalone product and instead begin designing around the financial lifecycle of the household itself.

Get in touch to explore deeper insights from our survey data and digital experience platform, and how these trends are evolving globally.

Mark Donohue

Managing Director iSky, Global

Mark Donohue is Managing Director of iSky at RFI Global, working with clients globally on data-led financial services intelligence.

View full profileFrequently asked questions on family banking

Q: How has family banking changed in recent years?

Family banking has evolved from a narrow focus on children’s accounts and parental controls into a broader, connected ecosystem. It now spans education, payments, saving, investing and long-term relationship growth, reflecting a shift towards supporting the full financial lifecycle of the household.

Q: Why should banks invest in family banking?

Family banking creates an opportunity to establish early customer relationships that can extend over decades. Many adult banking relationships originate through family influence or accounts opened at a young age, making it a strategic way to build long-term relevance, engagement and value.

Q: What do parents look for when choosing a bank account for their child?

Parents prioritise control over spending above all else when selecting a child’s account. As children get older, interest rates become more important, while trust in the bank and existing relationships also strongly influence decision-making.

Q: What is the future of family banking for financial institutions?

The future of family banking lies in supporting the financial lifecycle of the entire household rather than offering standalone youth products. Leading institutions are expanding into family hubs, investing tools, virtual cards, shared financial visibility and multi-generational wealth solutions. Success will depend on creating connected ecosystems that combine education, money management, security and long-term relationship growth.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.