The $45 trillion great wealth transfer aka The Silver Tsunami holds significant implications for investors, advisors, and families.

This monumental transfer of wealth is not only a financial event but a cultural and societal one. As Baby Boomers pass their assets to younger generations, the values, priorities, and financial behaviors of these inheritors will shape the future economic landscape.

According to the International Monetary Fund (IMF), this ageing population represents “the most formidable demographic challenge facing the world.” This shift will profoundly impact virtually every industry, especially financial services.

An unprecedented wealth shift is coming to the United States

The term ‘Silver Tsunami’ was first referenced in a September 2001 report by the Pew Internet & American Life Project. It describes the significant social and economic changes caused by the ageing of the baby boom generation (born between 1946 and 1964). In 2020, the US Census Bureau reported 55.8 million people aged 65 and over in the United States.

Our data from MacroMonitor, the largest survey of US financial service behavior, shows that over the next decade, households with individuals aged 70 and over are projected to transfer $45.05 trillion to the next generation. This is predominantly from Baby Boomers to Generation X and Millennials and approximately $18.81 trillion of this total will come from real estate assets alone.

The implications of healthcare costs

However, among families expecting to inherit wealth, the rising cost of healthcare is quietly reducing these assets. Fidelity estimates that today’s 65-year-old couple will need approximately $330,000 for medical expenses during retirement, excluding long-term care costs.

The impending wealth transfer presents a significant opportunity for firms to serve both those transferring wealth and those inheriting it. To effectively navigate this transition, firms must understand and adapt to the evolving needs of these distinct clientele groups. MacroMonitor provides laser-focused analytics of consumers’ financial behaviors and attitudes to address this phenomenon.

Four data-driven insights to help financial services adapt

1. The estate planning gap

Currently, 1 in 5 households prioritize providing for heirs, a sentiment evident across all ethnic groups. However, despite this priority, significant gaps in estate planning exist, highlighting areas where firms can offer vital support.

Older households are generally more likely to have legal documents in place, such as wills and powers of attorney, yet gaps remain even among different generations and income levels. For example, only 45% of Young Boomers (born 1954-1962) have power of attorney compared to 65% of Older Boomers (born 1946-1954). This disparity underscores the need for targeted estate planning education and services for younger boomers.

Additionally, only 7% of US households have a personal trust in place. Among households with total assets between $1 million and $3 million, 17% have a personal trust, while 20% of households with assets between $3 million and $5 million do. This indicates a clear opportunity for firms to educate their clients about the benefits of personal trusts and to assist in establishing these crucial instruments to ensure a smooth transfer of wealth.

2. High-touch relationships matter

In an era increasingly dominated by digital interactions, the value of high-touch relationships cannot be overstated, especially for older clients. Households with members aged 70 and above prioritize building long-term relationships and consider personal touch and face-to-face interactions are important. These clients value easy access to their financial advisors, guaranteed income, and the safety of their investments.

When deciding where to allocate their savings and investments, older clients lean towards firms that offer personalized service and a deep understanding of their needs. Firms that help these clients feel understood and supported will be best positioned during wealth transition decisions. Offering exclusive events, personal consultations, and dedicated relationship managers can significantly enhance the client experience for this demographic.

Offering robust mobile apps, virtual financial planning sessions, and real-time account access can attract and retain digitally savvy inheritors. Additionally, firms should consider leveraging social proof through testimonials and reviews to build credibility and appeal to potential clients.

3. Inheritors are digitally driven and open to change

The next generation of wealth recipients shows a distinct preference for digital interactions and services. With 5.14 million households having received or expecting to receive an inheritance soon, the safety of funds is their top priority. Many of these inheritors already hold assets with well-known firms like industry leaders Fidelity or Charles Schwab.

The average recipient of inherited wealth is 58 years old and is more likely to consider switching firms, especially if driven by recommendations and a desire for better digital services. This generation values intuitive platforms, responsive digital service, and the ability to manage their finances seamlessly online. Firms must highlight their digital capabilities, ensuring that their platforms are user-friendly, secure, and able to meet the evolving needs of these clients.

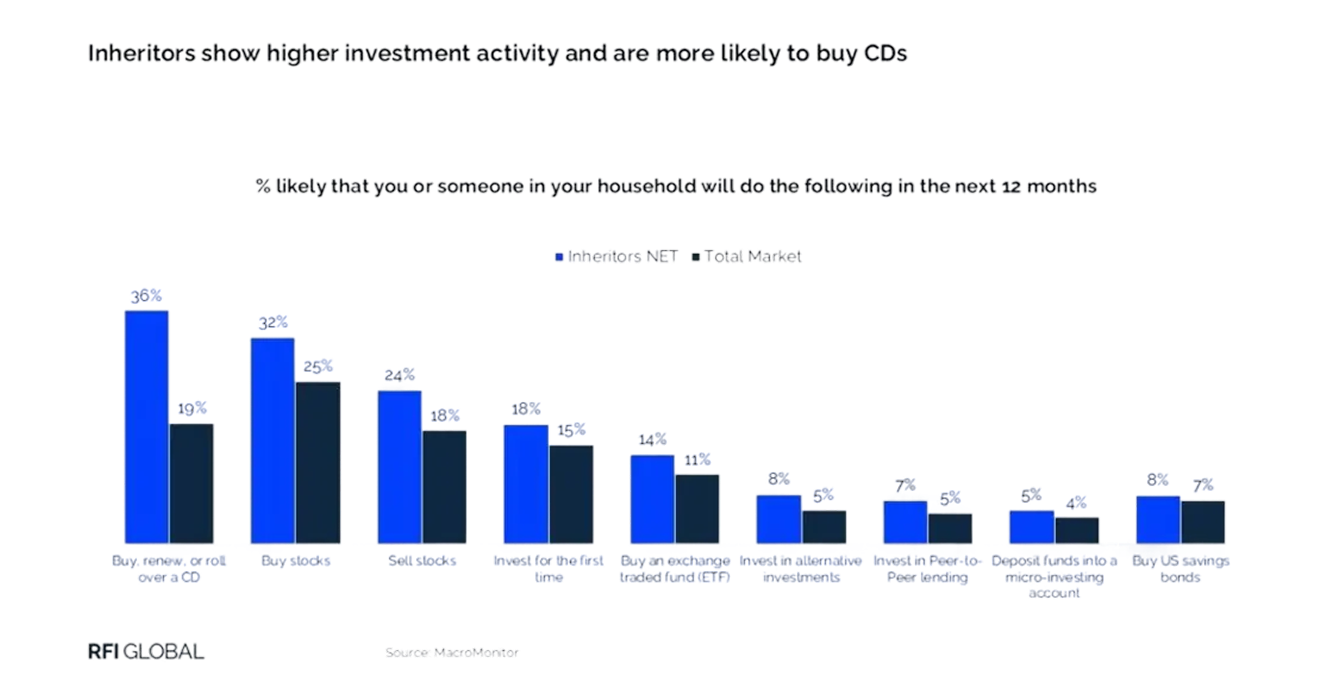

4. Safety and liquidity preferences create product demand

Both transferors and inheritors exhibit a strong preference for low-risk, liquid products such as certificates of deposit (CDs) and municipal bonds.

Offering conservative investment options with modern delivery methods, such as app access, clarity on performance, and transparency on fees. By matching investment offerings to the psychological needs of clients including safety, control, and predictability firms can build trust with both generations.

Creating portfolios that balance low-risk investments with opportunities for growth can appeal to clients who prioritize security while also seeking potential returns. Providing educational resources about these investment options and their benefits can also empower clients to make informed decisions.

The implications for financial services

The great wealth transfer presents both challenges and opportunities for financial firms and their clients. To stay competitive and relevant, firms must adopt a holistic approach that meets the evolving needs of transferors and inheritors.

- Delivering personalized financial planning tailored to each client’s life stage and goals

- Deepening client engagement through ongoing, proactive communication

- Embracing technology to offer seamless, data-driven experiences for digitally savvy clients

Equally important is building trust and transparency, particularly as families navigate complex financial decisions, and adapting to generational differences in communication preferences and financial priorities.

Ultimately, success will come from collaboration between advisors and a more informed, engaged client base.

Get in touch to explore MacroMonitor insights can help you anticipate needs, personalize engagement, and lead with confidence in this generational transformation.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.