Edward Smith, Lead Analyst, North America & EMEA

With up to 400 million active users of ChatGPT, AI is no longer a distant concept—it’s the current reality. But are banks ready to meet consumer demands?

To say that the development of Artificial Intelligence (AI) is fast-moving would be a vast understatement. As technology transitions from theory to everyday practice, the financial services industry has become more ambitious about integrating AI across its operations. Chatbots now support customer queries, personalized analytics help users better manage their budgets and comprehensive data structures form the backbone of advanced anti-fraud security measures, to name a few applications.

This time last year, my colleague identified the key areas where financial service providers would benefit most from incorporating AI services, and the central challenges they may encounter. With new data from MacroMonitor, the largest survey of US households’ financial behavior, we can now look in more detail at how financial institutions can best position these new AI-powered services to engage customers and attract prospects.

The rise of AI in finance

Consumer use of AI tools has exploded in the last few years. For ChatGPT alone, the number of active users doubled from 200 to 400 million between August 2024 and February 2025. Retail banks are chomping at the bit to give their spin on AI chatbots, with ‘Erica’ from Bank of America and Wells Fargo’s ‘Fargo’ as well-known examples, and challenger brands like Chime are also exploring the space. Many in the industry envision these tools as the groundwork for a fundamental transformation of customer relationships, anticipating that AI can facilitate deeply personalized banking experiences and a finely tailored process of product cross-sell.

Importantly, this ideal is not isolated to the institutions; consumers also intend to support their decision-making with AI tools. MacroMonitor shows that around 3 million US households employed AI chatbots as a source of information on financial products in 2024. A strong AI proposition has the potential to encourage greater reliance and trust from users, creating a stronger customer-provider relationship overall.

What consumers want from AI

Despite wider proliferation, most US consumers are still in the dark about what AI-powered financial services are, and why they are needed. 1 in 2 households surveyed by MacroMonitor claim to have only some level of understanding about the capabilities of AI in financial services — this proportion remains broadly consistent across age, affluence and ethnicity. While youth segments are more likely to report a comprehensive knowledge of AI (23% of GenZ vs 6% of Boomers) this mostly reflects the cohort of early adopters that have prior engagement with AI. Identifying both shared and specific knowledge gaps will be vital for financial institutions promoting AI offerings, supporting users to navigate available solutions and positioning the brand as a reliable source of truth.

Establishing trust

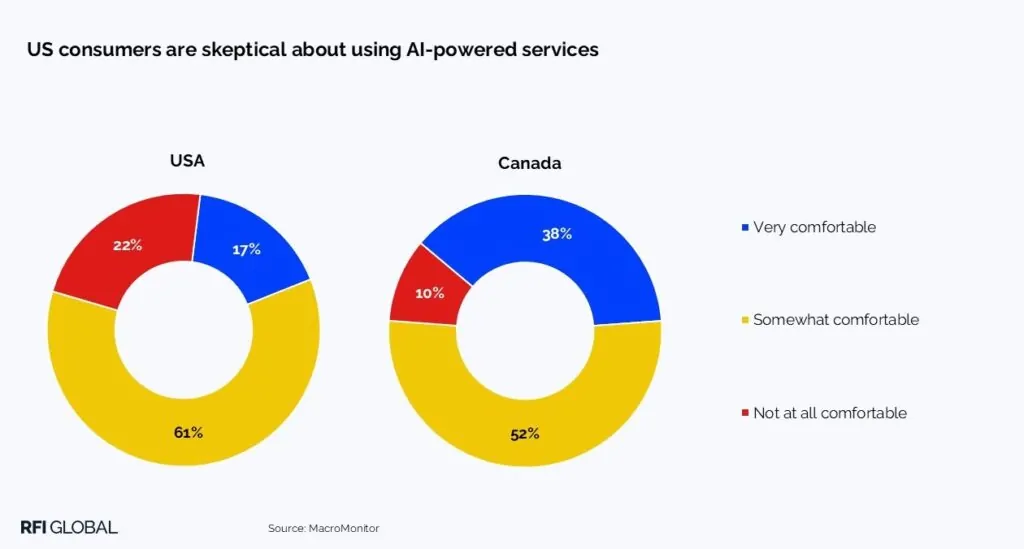

Financial institutions have an uphill struggle awaiting them, given the US population is overwhelmingly skeptical about using AI for banking tasks: only 17% of households are very comfortable using AI-powered technology, and 22% reject these services outright.

Other markets are far more open to using AI-powered services. In Canada, for example, 38% are very comfortable using AI and only 10% reject it.

With AI still in relative infancy in the US, few consumers are willing to entrust these tools to handle complex, data-sensitive tasks, preferring AI to serve back-end security rather than to produce custom insights based on their personal information. This hesitance has some solid basis, news like Microsoft ‘Recall’ logging users’ credit card details despite thorough permission filters, shaking customer confidence. Before asking customers to dream big, institutions must guarantee that users can sleep soundly knowing these tools are appropriately safeguarded.

Embedding AI tools

Exploring the behavior of early adopters reveals insights into how to get users started with AI. As one would expect, younger households are broadly more open to AI services, yet a distinct area of interest for this segment is access to robo-advisors. Awareness of AI-assisted investment platforms has grown drastically in the US, up from 11% in 2020 to 20% in 2024, and usage is slowly following suit as customers increasingly shop around for neo-bank and other fintech offerings. This is not exclusively a trend for the youth segment. The wider market has seen Affluent customers shifting towards digital-only competitors in search of greater returns and financial agency. Tellingly, 1 in 5 Asian-American households (that tend to be more savvy with adopting new financial technologies) currently use a robo-advisor for their investment service needs. When rolling out these advanced features, reinforcing AI’s role in effective decision-making should help establish these services as a competitive value add-on.

Pain points and frictions with AI

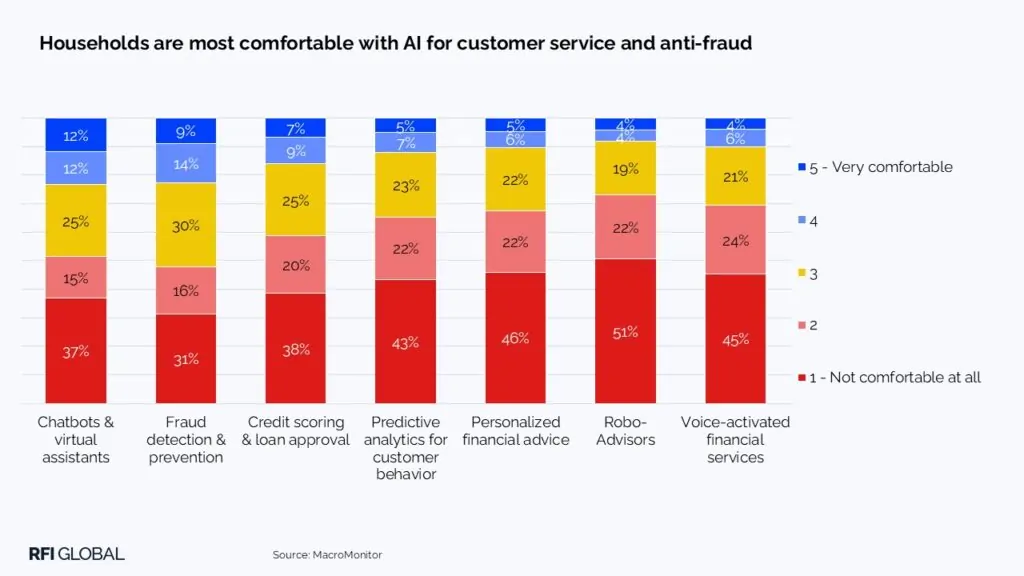

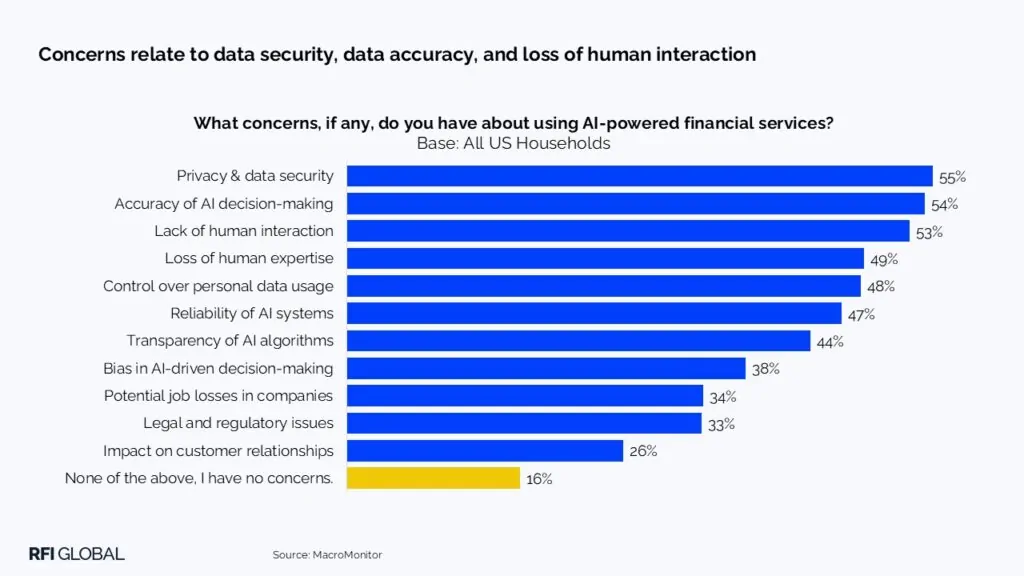

Given the multitude of viewpoints, it is worth digging deeper into US customer pessimism towards AI. 84% voice at least one concern with AI’s implementation in financial services, typically stemming from the potential disruption of the banking experience—privacy, security, accuracy, and agent accountability are common concerns across key demographics. However, not all complaints speak to the same underlying philosophy. On one hand, the stress that Boomers put on the lack of human interaction suggests that these older cohorts see AI as detrimental to the in-person channels they rely on. On the other, transparency and user control over the algorithms powering AI services are most significant to Affluent and High-Net Worth households, revealing a demand to know how exactly data is used by these programs. Recognizing that these emerging pain points have distinct and actionable solutions is one of the first steps in bridging consumer trust.

Strategies to build confidence

The consensus calls for open communication. US consumers want to see evidence of self-regulation and concise explanations of AI’s processes, benefits and limitations. We also see two divergent perspectives emerge from our data. For some, the impetus is on banking providers: Boomers lean towards educational tutorials on how to use AI tools, and around a third of Gen Z households want institutions to actively invest in the development of fair and reliable AI protocols. Others, meanwhile, prefer to hear an independent perspective:

- Emerging Affluents (who tend to put more faith in alternative media and finfluencers) are more likely to propose service authentication from outside experts.

- Asian households value having the option to customize how they interface with AI.

In essence, whether the customer wants their journey with AI to be guided or self-directed, institutions should emphasize their commitment to impartiality, clarity and flexibility, and let consumers engage with AI to the extent they are comfortable with.

Final thought: Humanizing the AI experience

All else being equal, providers should be conscious of how they communicate these innovations to users. AI solutions carry inherent risks, real and perceived, and having an honest, personable conversation about using these tools will be essential for building long-term engagement. The benefits of this technology are already tangible, with the advent of robo-advisors revealing new ways to empower customer decisions, so there is ample space to position these features as competitive value-adds. Most importantly, though, will be how institutions deliver these tools to users: an open and explorative interface would be effective for Early Adopters, while more in-depth tutorials and walkthroughs are appropriate for wider usage.

Brands able to build a reputation as a core authority stand to become a trusted source of truth, and in consequence, establish themselves as a dependable source of AI-powered tools.

As financial institutions navigate the evolving AI landscape, clear and consistent communication will be key to building trust. To explore how different consumer segments engage with AI—and how your institution can respond—get in touch for insights from our latest MacroMonitor study.

Edward Smith

Lead Analyst, North America & EMEA

Edward Smith is a Lead Analyst at RFI Global, covering financial services trends across North America and EMEA.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.