Over the last 18 months, there has been growing acknowledgement in UK business banking that mid-market enterprises (MMEs) are often misunderstood, prompting a renewed focus on how to serve what is frequently described as ‘the missing middle’.

This raises a fundamental question: how do financial institutions deliver solutions that genuinely meet the needs of the mid-market?

On the surface, Mid-Market enterprises appear well defined: annual revenue of £10m-£500 or 50-1000 employees, with meaningful scale and increasingly sophisticated needs. Yet, RFI Global’s UK SME and mid-market banking insights consistently show that revenue segments only ever tell part of the story. Growth stage, organisational complexity, international exposure and digital maturity all play a decisive role in shaping expectations.

This matters because our data highlights that expectations of financial institutions are rising rapidly. Businesses crave seamless digital capabilities that remove administrative friction, alongside human expertise that delivers real commercial insight. Crucially, our data shows that expectations of both digital and human excellence are not competing but increasing simultaneously. As a result, the challenge is no longer whether financial institutions can rise to this demand, but how and when to deploy digital and human capabilities to create meaningful impact.

Expectations on the rise for both digital and human

Like their smaller SME counterparts, digital channels dominate day-to-day interactions for MMEs. However, MMEs are far more selective about when and why they engage with human support. The distinction is no longer about frequency; it is about relevance.

MMEs are not seeking more touchpoints. They are seeking better-timed, higher-value interactions, deployed at moments of strategic importance. This is where personalisation becomes critical. In 2026, personalisation is the defining feature of banking propositions, whether delivered digitally or through human engagement. That is what shapes how MMEs judge the value of their financial institutions.

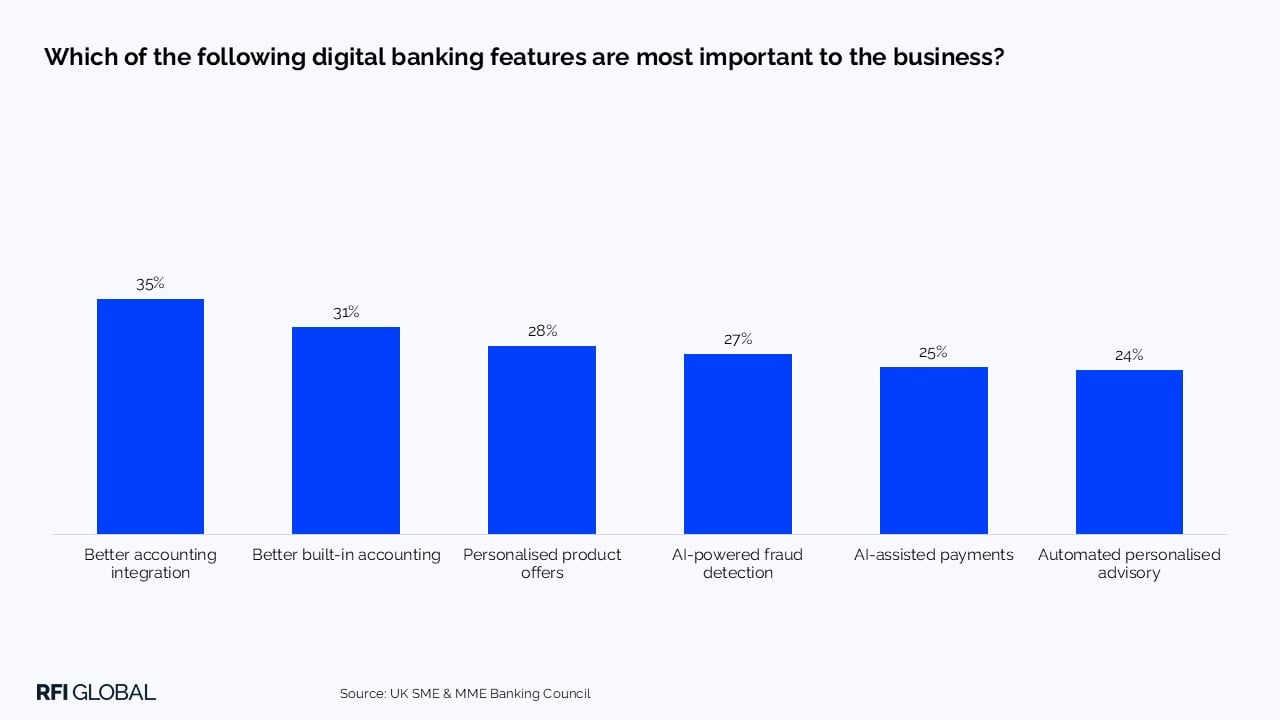

Digital platforms are increasingly setting the baseline expectation, a trend reinforced in our voice-of-customer research. 35% of MMEs cite better integration with accounting software, rising to 43% among weekly digital users, as the most important digital banking feature. Meanwhile, 31% view built-in accounting capabilities as most important. These have fast become non-negotiables: the workflow enablers that allow businesses to focus on running and growing their operations, rather than spending arduous hours on administration.

A demand for greater digital innovation is front and centre in MMEs’ minds. However, as with any innovation, the focus is less on reinventing the wheel and more on alleviating customer pain points to deliver tangible business impact. This naturally leads to the question of how artificial intelligence fits into the service model.

AI as an enabler, not a human replacement

Attitudes towards AI reinforce an important nuance in how MMEs view digital innovation. Our insights show that MMEs are broadly comfortable with AI. 35% are strongly supportive, recognising its ability to improve efficiency and experience. While 37% are somewhat supportive, viewing AI as acceptable for streamlining routine processes, rising to 42% among international MMEs. Personalisation is one area where AI can deliver meaningful impact for MMEs, with 28% seeing value in AI-driven personalised product offers that enable greater proactivity. There is also clear opportunity for AI to provide better visibility of business performance, strengthen security and reduce administrative effort.

Taken together, this signals a clear preference for AI as an enabler, one that removes friction from everyday banking and creates space for human expertise to thrive at moments of strategic importance or complexity. This distinction is critical. It reinforces the idea that technology should elevate the service model, creating capacity for higher-value human interaction, rather than seeking to replace it.

The debate is no longer AI versus relationship management. MMEs increasingly expect intelligent automation and high-quality human expertise to work together as part of a single service model.

Relationship management still drives advocacy

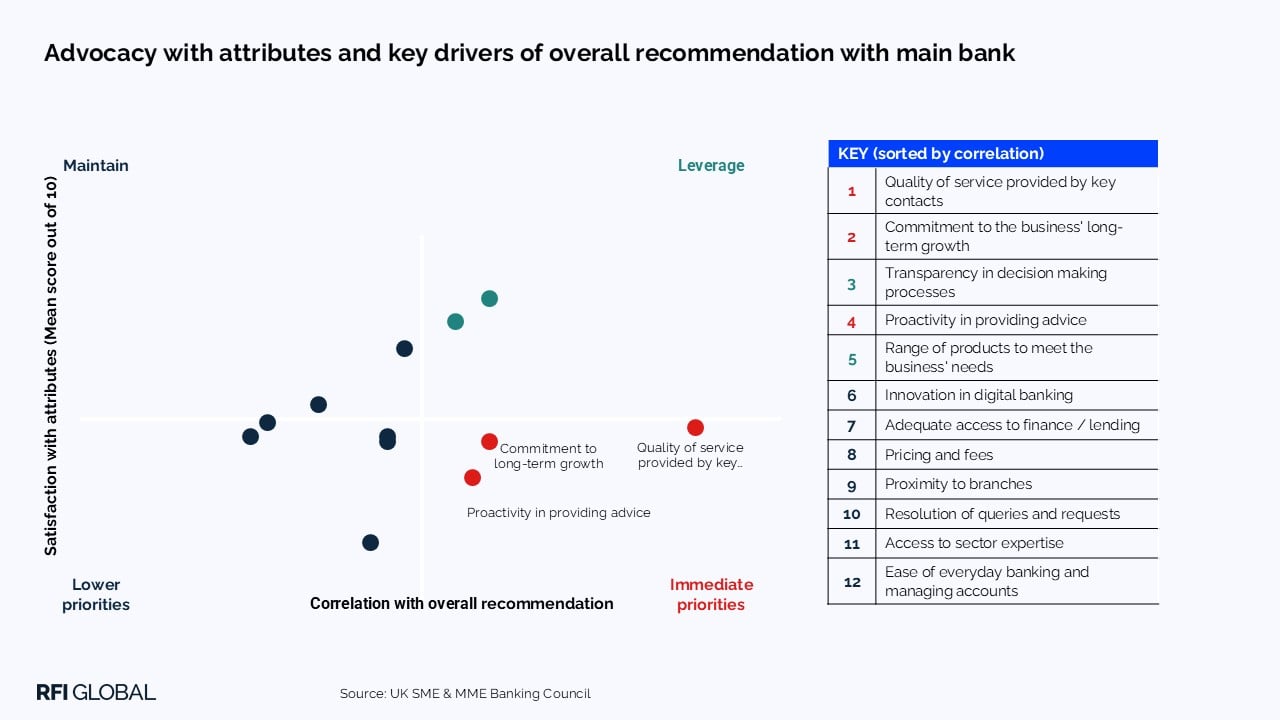

When we look at the top drivers of advocacy for MMEs, the importance of human expertise comes sharply into focus. Across the top five drivers, three are rooted in personal engagement.

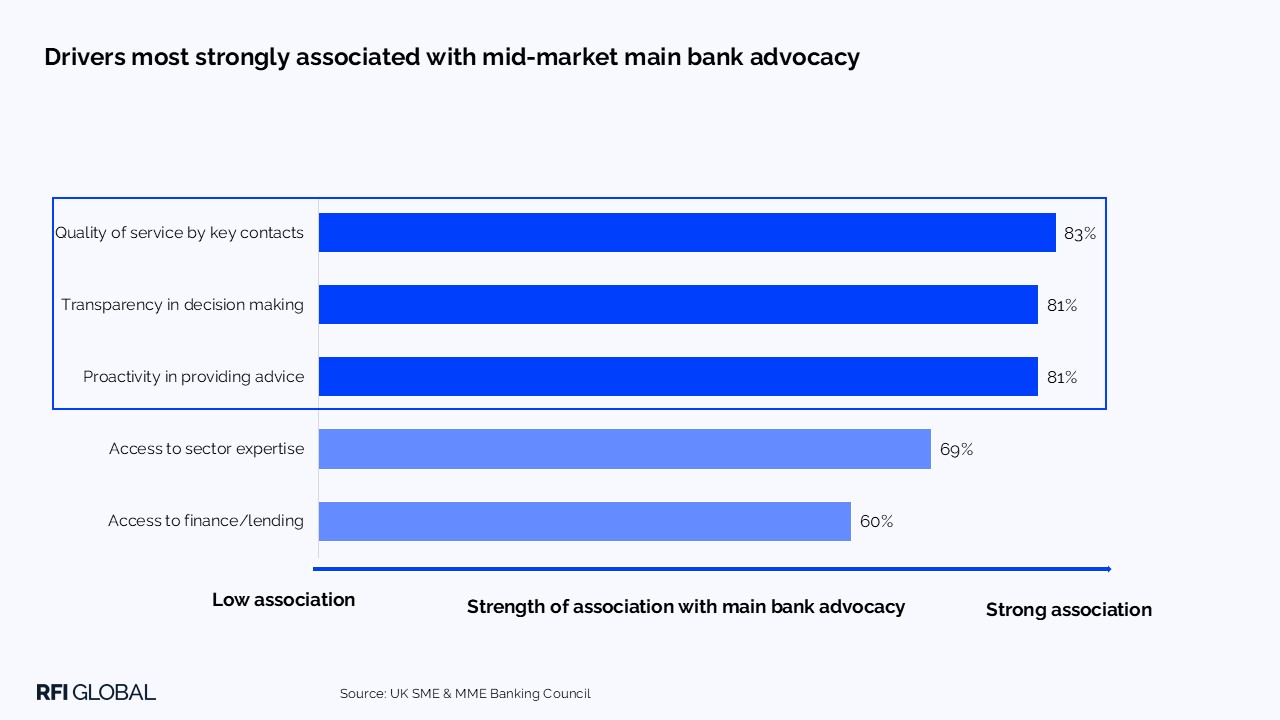

The leading driver of main bank advocacy is the quality of service provided by key contacts, followed closely by commitment to long-term growth and proactivity in providing advice. Crucially, these are the areas where MMEs see the greatest gap between importance and delivery, signalling a clear opportunity for differentiation.

As part of the inaugural RFI Global UK Banking & Finance Awards 2026, we highlighted the growing importance of commitment to growth as a key differentiator in the UK business banking landscape. This remains a long-standing pain point in the market and is becoming even more important for mid-market enterprises.

Historically, commitment to growth has been closely associated with access to lending, a factor that will always remain critical. However, our voice-of-customer data shows that commitment to growth is no longer measured by products alone, but by the quality of insight, transparency, and foresight a banking partner brings to the relationship.

The evolving role of the relationship manager

As digital capabilities increasingly absorb the operational load of MME banking, the role of the relationship manager is evolving accordingly. Value is no longer defined by accessibility or frequency of contact, but by relevance, judgement and insight at moments of strategic importance. Our voice-of-customer data reinforces this shift. Advocacy among MMEs is most strongly correlated with proactive engagement, reliable advice from the business’s primary contact, and the ability to engage in strategic dialogue. Yet these are also the areas where performance falls below expectations.

This does not point to higher-touch coverage models, but to smarter deployment of human expertise. Winning financial institutions will use digital channels to execute day-to-day banking, increasingly augmented with proactive, automated insights via digital. This empowers relationship managers to focus on what technology can’t easily replace: contextual advice, sector expertise and strategic foresight when complexity or change arises.

How to win with mid-market businesses

The message is clear, digital excellence is now table stakes, but advocacy in the mid-market is shaped by how and where human expertise is applied. The strongest signals come not from access alone, but from transparency, proactivity and the ability to engage in moments of strategic importance. Winning financial institutions will be those that use technology to remove friction and surface insight, while focusing human support where it delivers the greatest impact. There are a few clear principles that define how to win with MMEs.

- Use technology to create space for human impact, not replace it – MMEs value AI and automation most when they remove friction, surface proactive insights and improve visibility. This enables financial institutions to deploy human expertise more effectively at moments of strategic importance.

- Anchor relationship value in proactivity, advice and strategic dialogue – These are the areas most strongly correlated with advocacy yet are also where performance falls short of expectations

- Relationship management is about relevance, not coverage – Winning in the mid-market does not require more touchpoints. It requires smart deployment of RM expertise, aligned to moments of change, complexity and growth where judgement and insight genuinely add value.

- Demonstrate commitment to growth through action, not access alone – Commitment is no longer defined solely by lending. Sector expertise and proactive support increasingly determine whether a bank is viewed as a genuine long-term partner.

RFI Global’s UK SME and mid-market banking research tracks how MMEs evaluate their banking partners across digital experience, relationship management, growth support and advocacy drivers. Get in touch to understand how you perform vs competitors, and what SMEs and MMEs want from their financial institution.

Frequently Asked Questions about mid-market business banking needs

Q: What do mid-market enterprises (MMEs) want from their banks?

RFI Global data shows that MMEs expect a combination of seamless digital banking and high-quality human expertise. Digital capabilities are now a baseline requirement for reducing administrative friction and improving operational efficiency, while human engagement is expected to deliver relevant, timely and commercially valuable insight at moments of strategic importance.

Q: How important is AI in mid-market business banking?

AI is increasingly viewed as an enabler rather than a replacement for human interaction. MMEs are broadly supportive of AI, particularly where it improves efficiency, enhances personalisation, strengthens visibility of business performance and reduces administrative burden. The expectation is that AI should complement, not replace, relationship-driven banking.

Q: What role does relationship management play in mid-market banking success?

Relationship management remains a primary driver of customer advocacy. MMEs place the highest value on proactive engagement, trusted advice from key contacts, and support for long-term growth. However, there is a persistent gap between the importance of these factors and perceived delivery, creating a key opportunity for differentiation among banks.

Q: How are expectations of business banking changing for MMEs?

Expectations are rising across both digital and human dimensions simultaneously. MMEs now expect digital channels to handle day-to-day banking as a baseline, while also expecting more relevant, insight-led human interaction. The distinction is shifting from frequency of engagement to the quality, timing and relevance of support provided.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.