Jon Ruston, Insights Director, EMEA & North America

It continues to be a challenging time to run a business. While juggling daily operations, SMEs have faced global uncertainty, changing regulations and rising inflation. As a result, understanding the needs of small and medium-sized businesses (SMEs) has never been more important. For banks and fintechs serving this segment, these shifts are not simply macroeconomic pressures; they define where future growth, differentiation and customer retention will come from.

Our Financial Services Trends and Predictions 2026 report identified five global trends that will shape 2026 for consumers and businesses. In this article, I examine each trend and highlight the key opportunities in SME banking for financial institutions in 2026, based on survey insights from over 10,000 SMEs across Australia, the UK, Canada, US, Hong Kong, Malaysia and Singapore, plus insights from our iSky platform, which tracks thousands of real consumer interactions with banking apps globally.

Trend #1. AI-powered finance: Building trust through transparency

Artificial intelligence is no longer a distant innovation for SMEs; it is part of their everyday operations. In 2023, just 1 in 10 UK SMEs had no concerns using AI in financial services. By 2025, this figure has surged to over 1 in 4 (27%), and we expect further growth in 2026.

In Canada, sentiment remains more cautious; fewer than 1 in 5 SMEs (18%) are fully supportive, with more than 1 in 4 (27%) comfortable with AI for only routine tasks.

As comfort grows, so does scrutiny. When looking at perceived benefits of AI, SMEs increasingly recognise AI’s potential to improve operational efficiency and reduce costs, yet concerns persist, particularly around data security and the loss of human interaction. The latter is cited by 25% of UK SMEs, and by 60% in Canada. Meanwhile, 38% of Australian SMEs believe that AI chatbots would never be able to replicate human interaction.

For financial institutions, building trust through transparency is essential. That means clearly communicating to SMEs about how AI is used, what outcomes it delivers, and understanding where human expertise remains vital. In a landscape of rapid technology change, clarity, control and trust will define the winners.

Trend #2. Digital UX: Winning in a mobile-first landscape

Digital experiences are undergoing rapid transformation for businesses. Across 55 corporate and SME web channels benchmarked with our iSky platform, and a comparable set of mobile apps, the strongest growth has been in workflow automation, payment security and administrative control.

The ability for administrators to manage user access and authorisations online has increased 19% since 2023, while tools supporting same-day or batch payment approvals have grown 14%. Security management features, spanning biometrics, token login and device recognition, are up 18%, with almost nine in ten apps now offering multi-factor authentication. Audit-trail and activity-log tools, once niche, are now present in nearly 60% of commercial interfaces, rising 11% in two years.

Collectively, these changes point to a sector rapidly professionalising its digital capabilities: shifting from transactional gateways to integrated command centres that give finance stronger oversight, security and control.

Understanding the evolving digital landscape is an imperative for financial institutions, from customer needs through to digital service delivery, so they can improve customer satisfaction, innovate with confidence, and stay ahead of the market.

Trend #3. Fintech acceleration: Personalisation as the differentiator

Fintechs are rewriting the rules of SME banking, and mobile is the new battleground. In 2025, half of UK SMEs (49%) and two-fifths of Hong Kong SMEs (38%) held a business banking product with a fintech, up from one-third (30%) five years ago. Our data shows that this surge is driven by frictionless onboarding, strong digital capabilities and constant innovation.

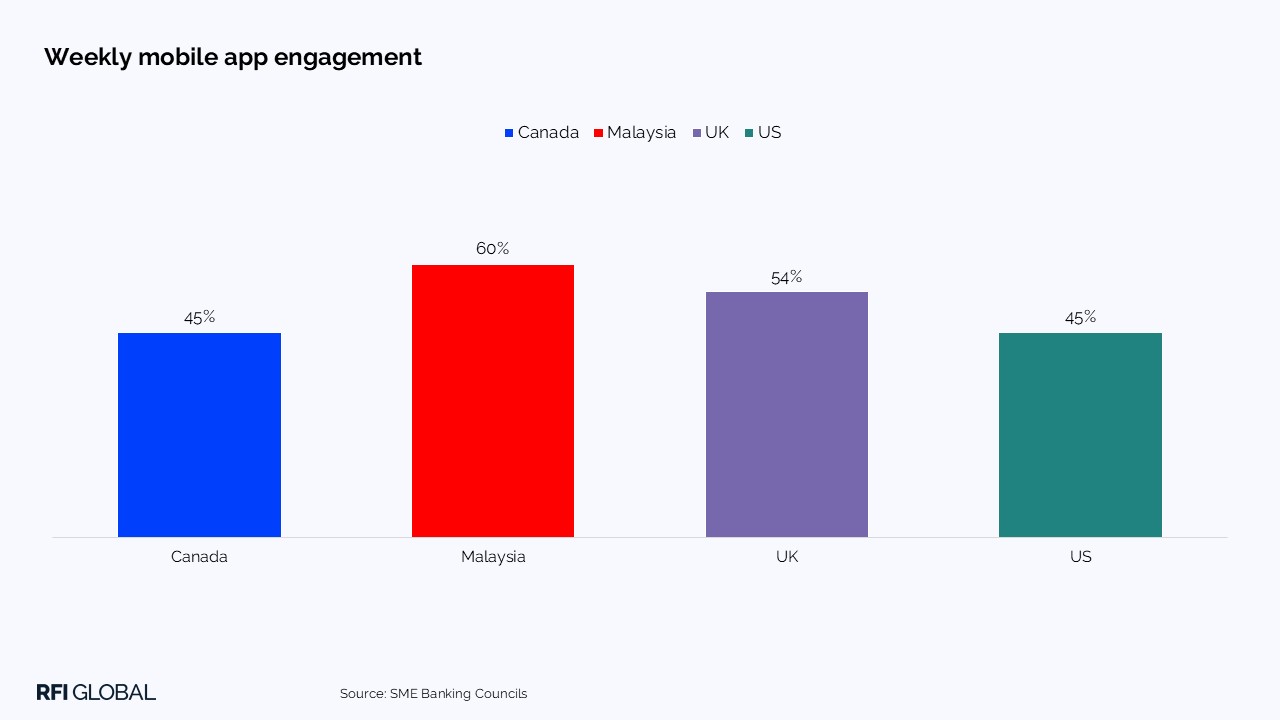

The knock-on effect of fintech is clear. In 2024, UK mobile banking app usage overtook online banking for the first time, a trend that’s continuing in 2025, and one that is replicated in other markets. Over 1 in 2 UK SMEs (54%) now use mobile banking apps weekly, with Canada and the US close behind at 45%. Meanwhile, Malaysia leads the way with 60% engaging weekly.

In this mobile-first landscape, the winners will be those delivering personalised, insight-driven experiences. Over 1 in 2 SMEs across markets crave better personalisation from their mobile banking app.

Tailored product recommendations, relevant business insights, and predictive tools will define the next generation of SME banking apps.

Trend #4. Cybersecurity: From operational risk to strategic value

Cybersecurity is no longer a back-office concern; it’s a frontline risk. As SMEs deepen their reliance on digital channels, the threat has evolved rapidly. In 2025, in the UK alone, major brands like Jaguar Land Rover, Marks & Spencer, and Co-op have suffered from cyberattacks that halted operations and exposed sensitive customer data. The ripple effects have hit thousands of SMEs in their supply chains.

Our data shows that 1 in 4 SMEs across the UK (24%), Canada (23%) and over a third in Australia (36%) now rank cybersecurity as their top business challenge. Yet many still lack the tools, knowledge or capacity to respond effectively.

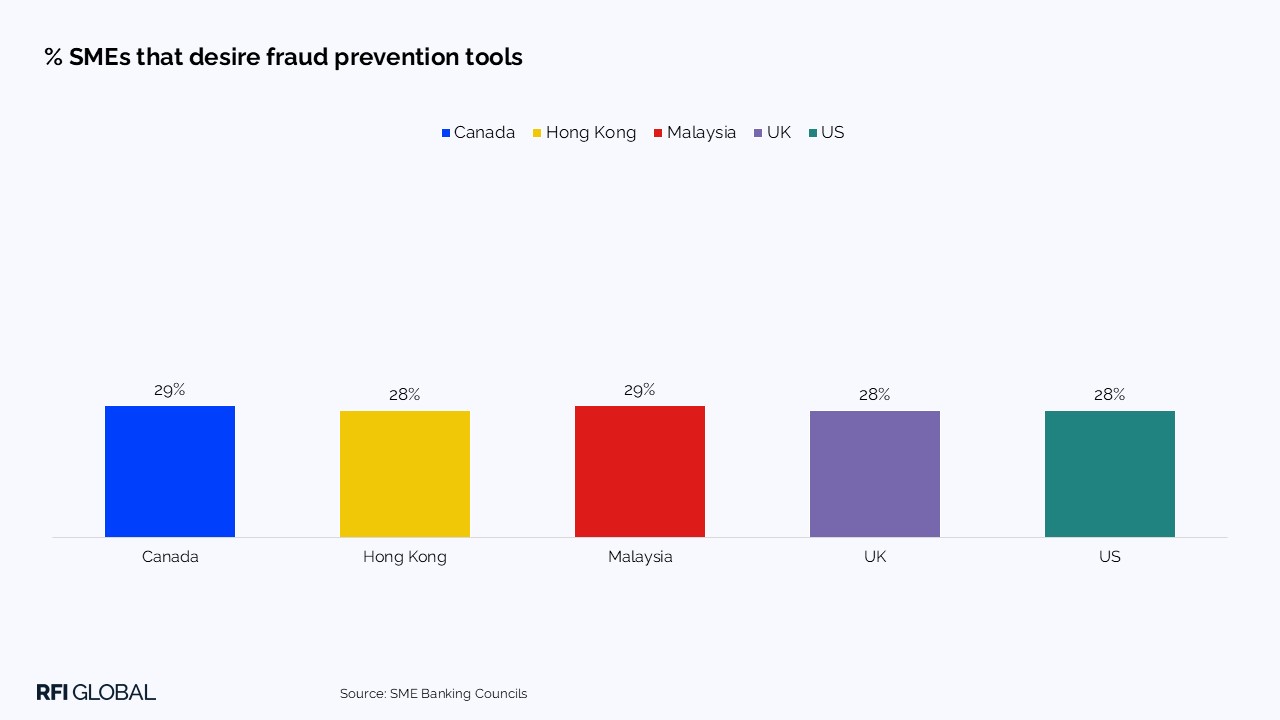

This is where financial institutions can play a vital role, by offering cybersecurity and fraud prevention tools that help SMEs actively defend against threats. Over 1 in 4 SMEs in the UK (28%), US (28%), Canada (29%), Hong Kong (29%) and Malaysia (28%) want their financial institution to offer these tools, the second most desired value-add tool after accounting solutions.

In a climate where cyberattacks are a growing threat, financial institutions can help develop resilience among SMEs, equipping them with the defences they need.

Trend #5. Growth: Becoming a strategic SME partner

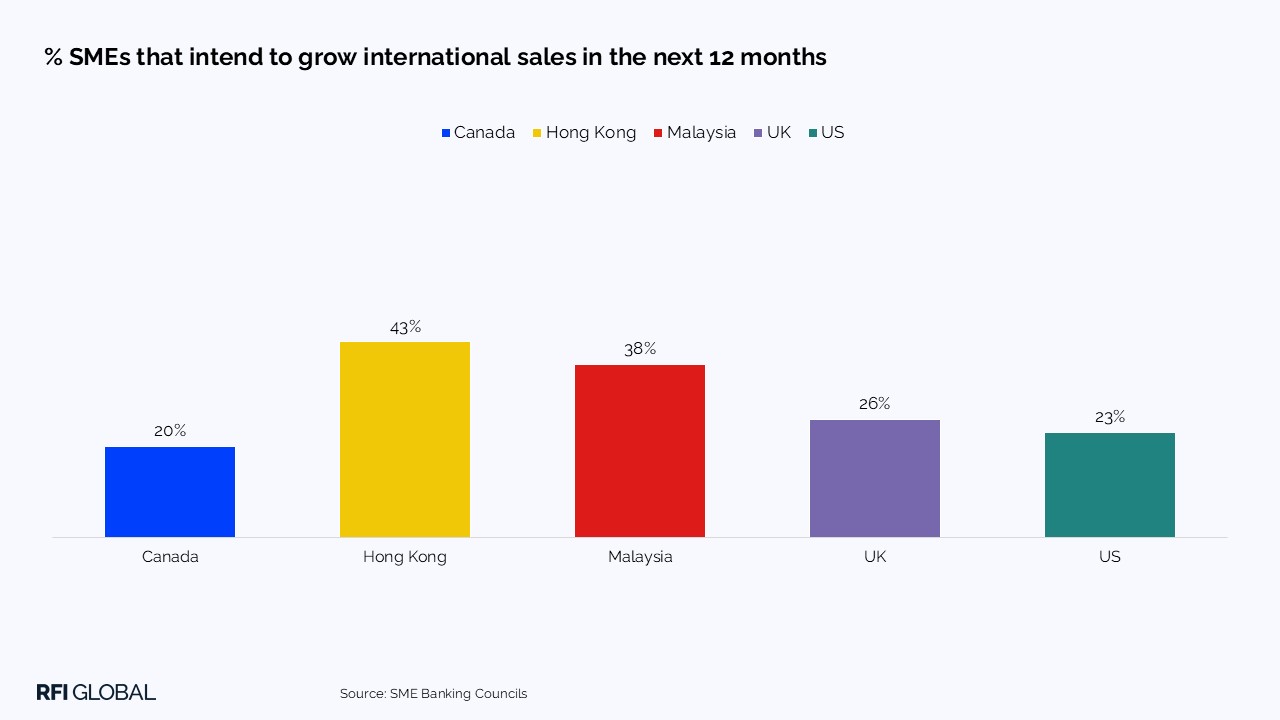

Despite economic headwinds, global ambition is alive and well among SMEs. In 2025, over 1 in 4 SMEs globally intend to grow international sales in the next year. APAC SMEs lead the way, with 43% of Hong Kong SMEs and 38% of Malaysian SMEs looking to do so. UK SMEs slightly outperform the average (26%), while the US (23%) and Canada (20%) trail.

Even amid trade uncertainty, SMEs remain resilient, with 28% of UK SMEs and 23% of Canadian SMEs planning to expand their cross-border operations.

This ambition underscores the vital role SMEs play as the backbone of global economies. However, as they scale internationally, their expectations of financial institutions are evolving just as fast. The role of financial institutions is shifting, from transactional facilitators to strategic growth partners.

Over 1 in 3 SMEs in the UK (34%) and Canada (38%) with international ambitions seek insights on business and industry trends in new markets, reliable information tailored to their specific needs, and tools that simplify cross-border payments and compliance.

The winning financial institutions will be those that act not just as service providers, but as strategic enablers of global SME growth.

Five key takeaways for SME banking in 2026

1. Artificial intelligence is now embedded in everyday business. Comfort levels for AI in financial services have grown over the last two years. Institutions that lead with trust and transparency will be best placed to unlock growth.

2. Mobile is the key battleground for SME banking. In a mobile-first environment, personalisation will define success, achieved via tailored product recommendations, relevant business insights and predictive tools.

3. Cybersecurity is a frontline business issue. Financial institutions can play a vital role in equipping SMEs with the tools they need, with fraud prevention the second most desired value-add tool globally, following only accounting solutions.

4. Global ambitions remain strong among SMEs. SMEs are looking for strategic partnerships that facilitate global growth. Providers that seek reliable insights on business and industry trends and provide tools that simplify cross-border payments and compliance, will lead the way.

5. Business digital experiences are changing rapidly, with strong growth in workflow automation, payment security and administrative control. Institutions that invest in digital capabilities will be better positioned to drive satisfaction, innovation and long-term competitiveness.

Get in touch for further insights from our reports and global SME surveys and download the full Financial Services Trends and Predictions 2026 report here.

Jon Ruston

Insights Director, EMEA & North America

Jon Ruston is an Insights Director at RFI Global, leading research programmes across EMEA and North America.

View full profileSME banking in 2026: Key questions answered

Q: What are the biggest business banking trends for SMEs in 2026?

The most influential trends shaping SME banking in 2026 are AI adoption, fintech-led personalisation, rising cybersecurity threats, growth, and rapidly evolving digital user experience. Together, these trends are redefining how SMEs choose and engage with financial institutions, with trust, insight and digital capability becoming key differentiators.

Q: How will AI change SME banking in 2026?

AI is becoming embedded in everyday business banking, improving efficiency, cost control and customer support. However, adoption depends on trust. SMEs want transparency around how AI is used, how data is protected, and where human expertise remains essential. Institutions that combine AI with clear governance and accountability will be best positioned to drive growth.

Q: Why is cybersecurity now a strategic issue for SME banking?

As SMEs rely more on digital channels, cybersecurity has become a frontline business risk rather than a back-office concern. Increasingly, SMEs expect their financial institution to provide fraud prevention and security tools. Banks and fintechs that embed protection into core services can help strengthen SME resilience and deepen long-term relationships.

Q: How can banks support SMEs looking to grow internationally

SMEs with global ambitions are seeking more than transactional services. They want strategic partners that provide market insights, simplify cross-border payments and reduce compliance complexity. Financial institutions that actively seek customer insight and combine it with tailored tools for international trade will be best placed to support expansion and capture sustainable growth.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.