Jon Ruston, Insights Director, EMEA & North America

What happens when banking as usual no longer works for businesses?

As digital channels redefine convenience and SMEs increasingly seek meaningful, human interactions, we in the financial services sector are being challenged to rethink what ‘optimal service’ really means.

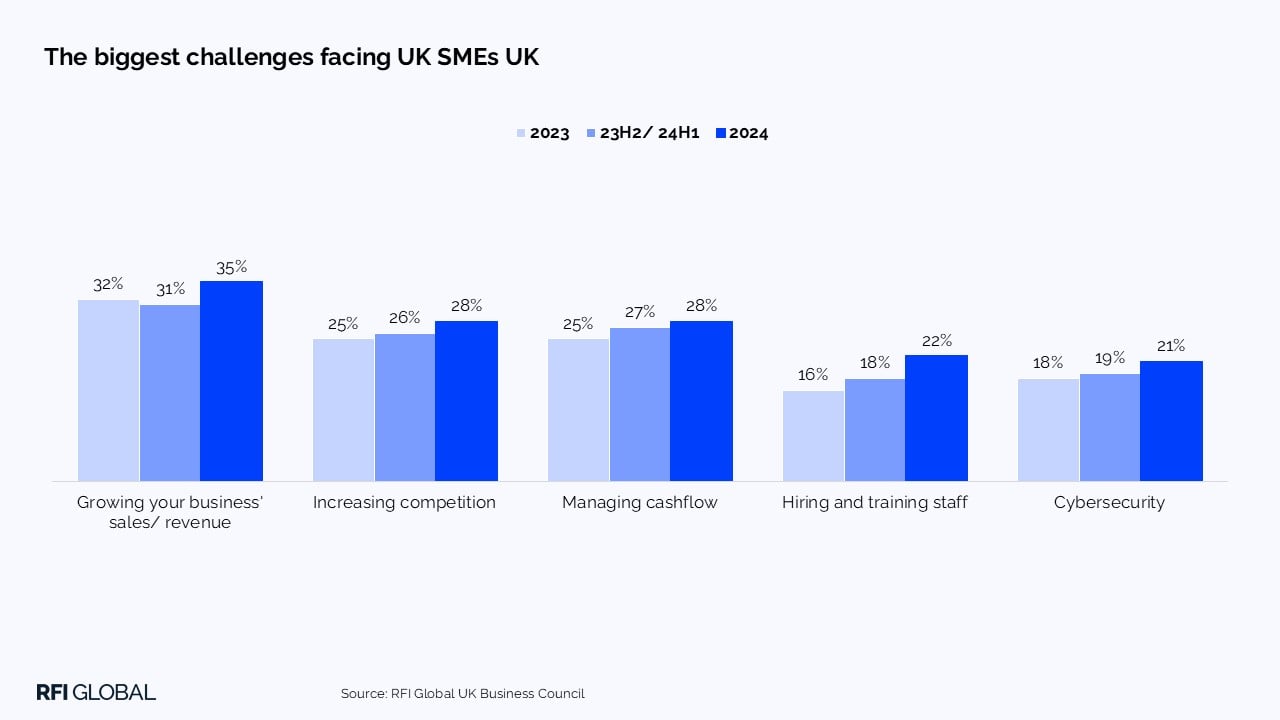

SMEs face increasing pressure – juggling daily operations, growth ambitions, and a fast-changing, competitive, global macro-economic climate. And over the last two years, we’ve seen the number of challenges facing SMEs increasing.

This is where digital channels have stepped in, helping to streamline complex tasks so business owners can focus on what they do best. After all, no one starts a business to spend their days doing admin and reconciling payments.

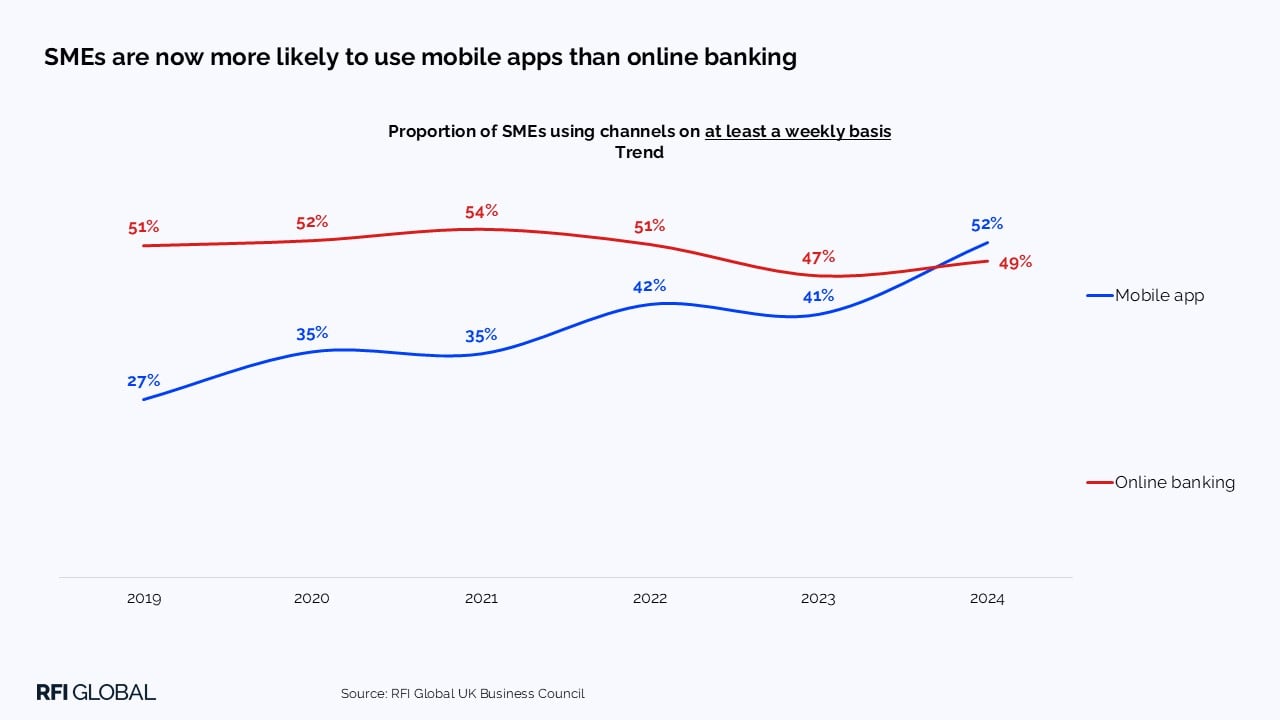

At RFI Global, we have tracked the growing shift to digital channels among SMEs, in the UK and worldwide, with our Business Council surveys, and in particular the growth of mobile banking.

At the end of 2024, SMEs’ weekly mobile banking app usage in the UK surpassed desktop banking for the first time, marking a significant milestone, and one we expect to continue through 2025.

Digital continues to drive competition

In 2025, there are a plethora of digital-only players available to SMEs, offering fast application processes, strong digital capabilities, and seamless integration with third-party tools. We have been tracking the rise of these players closely. Now, around half of UK SMEs use a fintech for their business banking needs. This has grown steadily in the last 5 years, when around a third of SMEs used fintechs. This has resulted in an increased demand for digital channels and convenience, with traditional providers also raising their game.

However, while offering convenience, digital channels can fall short when nuance, context, or reassurance is required. That is where the human element becomes essential. Therefore, the challenge for us isn’t forcing a choice between digital or face-to-face; it is designing a model that flexes to meet SMEs where they are, when they need it most.

Personalisation is paramount

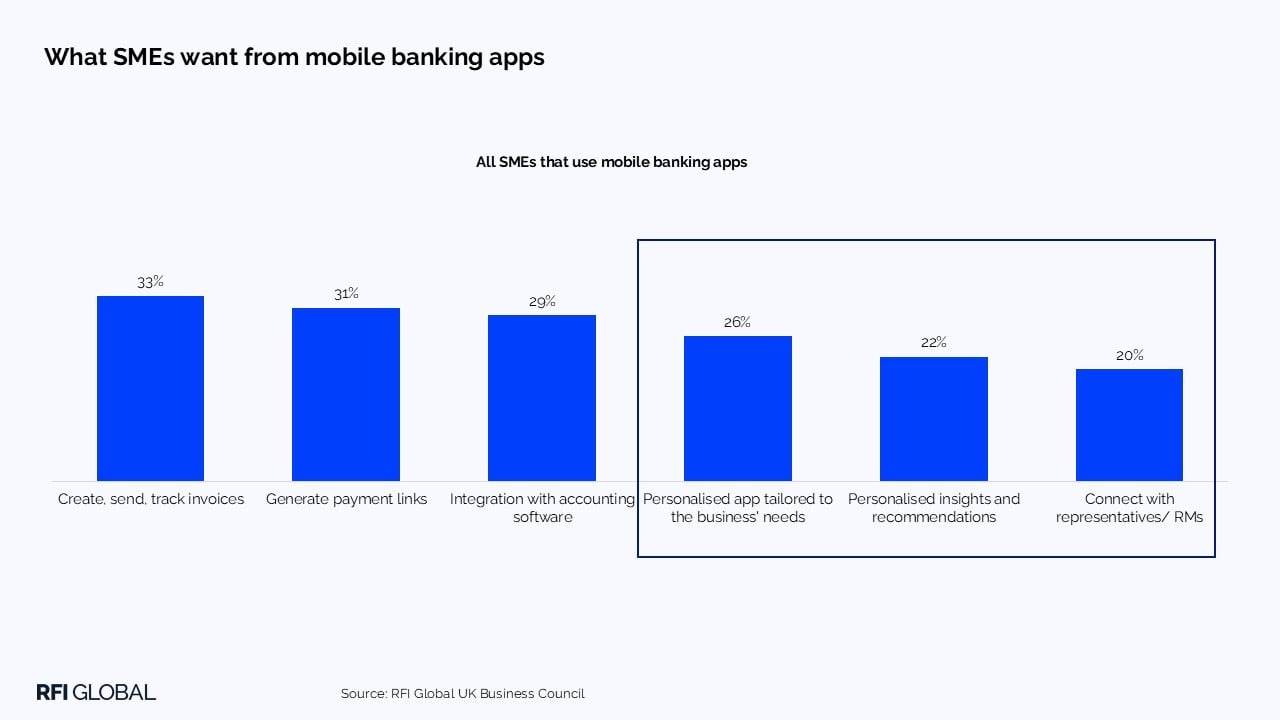

As a result, SMEs are now demanding a more personalised digital customer experience. Our data shows that one of the top unmet needs with UK mobile banking apps is the lack of tailored functionality.

SMEs want to log in and instantly see what matters most, whether that is key account insights, relevant product recommendations, or best-practice guidance for managing their finances.

More than 1 in 4 UK SMEs cite a personalised platform tailored to their business as the most desired feature they seek in a mobile banking app. Digging deeper, there is an important reminder of the role of personal touch within the optimal service model. One in five SMEs want the ability to connect directly with bank representatives/ relationship managers via their mobile banking app.

This further highlights the growing shift toward a mobile-first relationship in SME banking. SMEs see the mobile app, not just as a tool, but as the gateway to their broader financial ecosystem.

Rising expectations for human contact

Given the autonomy that digital delivers, with day-to-day account maintenance now just a tap away in SMEs pockets’, expectations are rising for what financial institutions can deliver, beyond digital tools, via the human touch. Our data shows that SMEs crave greater proactivity from their primary banking partner. Among UK SMEs, proactive advice has emerged as one of the top unmet needs over the past two years and continues to be unresolved. Less than 1 in 2 UK SMEs are very satisfied (8+/10) with the level of proactive advice offered from their primary banking partner.

The Opti-channel approach

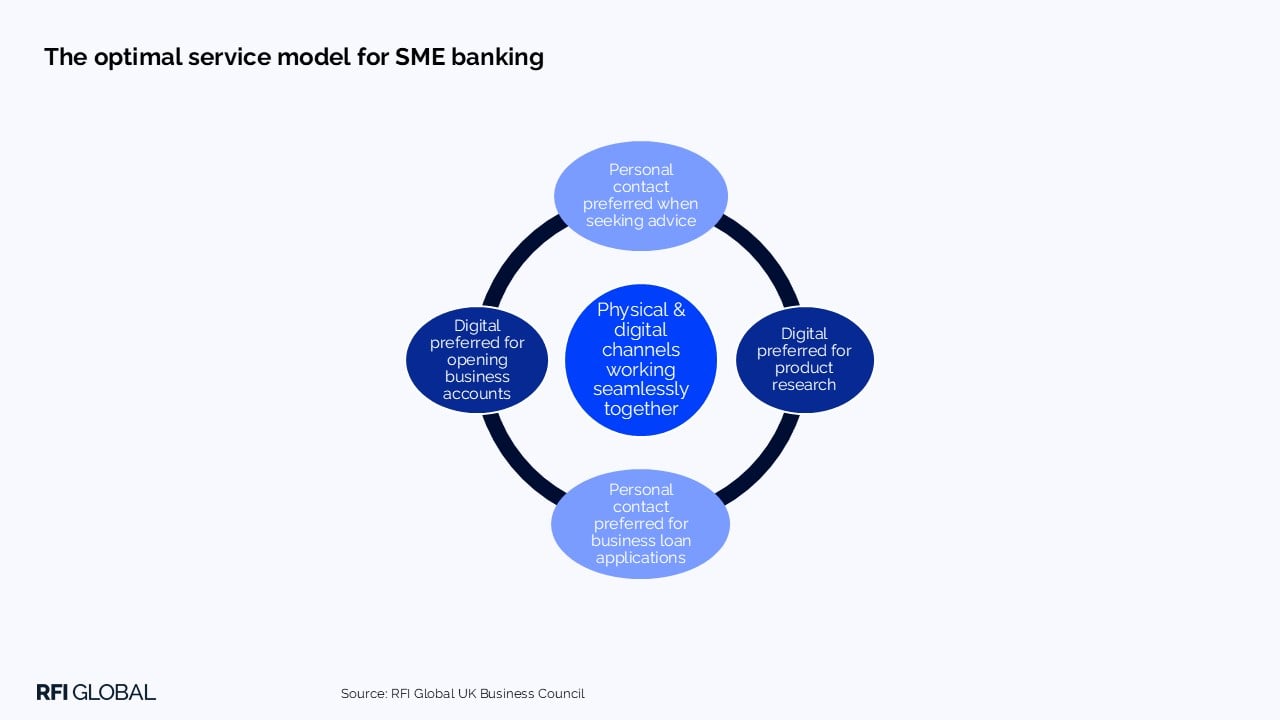

The importance of both digital and personal channels becomes very clear when exploring how SMEs prefer to engage with their financial institutions. This is where we lift the lid on what an optimal service model truly looks like.

Digital channels are preferred for product research or opening business accounts, offering autonomy and seamless application experiences. However, when it comes to more complex tasks, such as applying for a loan or seeking tailored advice, SMEs turn to personal contact. A one-size-fits-all approach is not a winning formula for SMEs in 2025.

Key takeaways for SME banking providers

Phrases like ‘omni-channel’ or ‘multi-channel’ are often used to describe optimal service. However, the most appropriate is ‘Opti-channel’, a model built around delivering the right solution, at the right time, through the right channel. Holding these principles close, it is this precision through personalised digital channels and human contact that holds the key to unlocking the optimal service model and delivering effective SME banking.

Here are some of the key criteria for an opti-channel model based on our surveys with SMEs:

1. Digital is essential, but not enough

Mobile usage has overtaken desktop for the first time, and fintech adoption continues to rise, but digital alone doesn’t meet all SME needs.

2. Personalisation is a growing priority

SMEs want mobile platforms tailored to their business, with relevant insights, tools and product recommendations front and centre.

3. Human connection still matters

One in five SMEs want direct access to a bank representative via their app, showing that digital should enhance, not replace, human interaction.

4. Proactivity is a missed opportunity

Fewer than half of SMEs are very satisfied with the proactive advice they receive, signalling a gap for traditional providers to close.

5. The Opti-channel model is the way forward

The most effective approach is not omni-channel for its own sake, but precision-led service, delivering the right support, in the right way, at the right time.

We’ve been tracking the evolving needs of UK SMEs since 2016, with new insights gathered from 3,000 small and medium businesses twice a year. Get in touch for more insights from our surveys if you want to explore what this means for your organisation.

Jon Ruston

Insights Director, EMEA & North America

Jon Ruston is an Insights Director at RFI Global, leading research programmes across EMEA and North America.

View full profileFrequently Asked Questions

Q: What are the biggest challenges UK SMEs face in 2025?

A: UK SMEs are under increasing pressure, with the top challenges including growing revenue, managing cashflow and staying competitive in a fast-changing economic environment. RFI Global data shows these challenges have intensified over the past two years.

Q: How are SMEs using digital banking in 2025?

A: Mobile banking is now the most-used channel among UK SMEs, overtaking desktop for the first time in late 2024. Many SMEs also rely on fintechs, with nearly 1 in 2 UK SMEs using a digital-only provider for business banking.

Q: What do SMEs want from their bank?

A: SMEs want more than just digital tools – they’re looking for personalised platforms, proactive advice, and direct access to relationship managers, all integrated into a seamless digital experience. 1 in 5 SMEs want to speak to a bank representative through their mobile app.

Q: How can banks better serve SMEs today?

A: Banks need to move beyond one-size fits-all service models. An opt-channel approach, blending digital convenience with human connection, helps deliver the right support at the right time, which is critical for meeting evolving SME expectations.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.