Jackie Greig, VP Marketing, Global

Over the past decade, female entrepreneurs have become an increasingly powerful force in the global economy. Yet, despite their growing presence, women remain a minority in the small to medium business sector (SME). RFI Global SME data shows that only between one-fifth and two-fifths of SMEs are owned by women, so we turned to our data in key markets to look at how financial institutions can better support the needs and growth of female business.

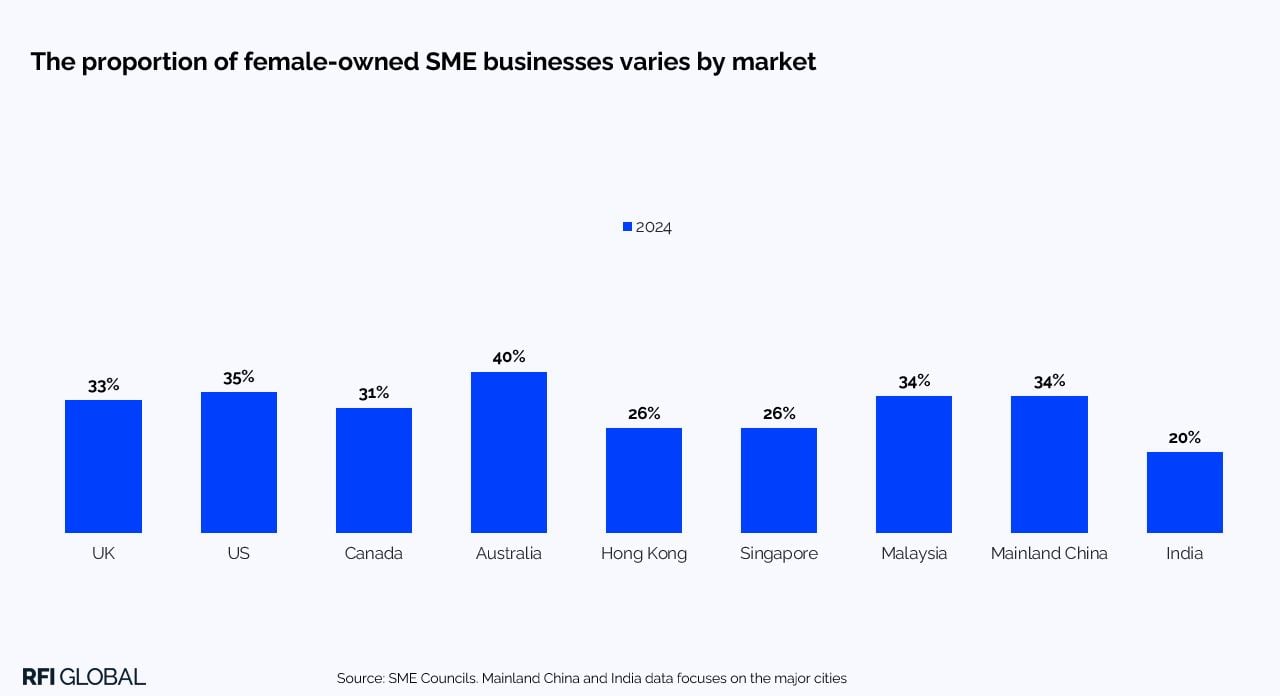

Which markets are leading the way?

Australia stands out, with 40% of SME’s led by female entrepreneurs. It is followed by the US, Mainland China, Malaysia and the UK,where women own around a third of businesses. At the other end of the spectrum, India lags significantly behind, with just 20% of SMEs owned by women.

The funding gap: An uphill battle for female entrepreneurs

One of the most pressing challenges for female entrepreneurs is access to capital. As women establish and scale successful businesses, they face greater hurdles in securing the funding needed for growth. According to the Harvard Business Review, venture capital investment in female-led businesses remains shockingly low: just 2.3% total VC funding goes to all-female-founded teams and 10.4% for mixed-gender founding teams.

This funding gap is not a reflection of ambition. Many female-owned SMEs expect to increase their annual revenue over the next 12 months – 52% in the US, 44% in Australia and 40% in Canada.

So, how can financial institutions better support the needs of this growing and ambitious segment?

The digital advantage: A more level playing field?

In a recent episode of our Banking Uncovered podcast, Kathryn Petralia, Co-founder of Kabbage and Keep Financial, and one of Forbes’ most powerful women in tech, explained how Kabbage attracted twice as many women and minority customers than the general business-owning population due to the anonymity and lack of judgement reflected in digital platforms. She explained that:

“People could [apply for a small business loan] anonymously, you go online, and you could apply online, you didn’t have to sit across from a loan officer in a bank who was judging you and maybe didn’t understand your business or you personally or you look different than they did. And the other thing is, we’re using just data, we’re using real-time data to make decisions, and the data was determining the outcome.”

It is no surprise that 37% of female entrepreneurs in the UK use fintechs vs 33% of men.

The challenges women entrepreneurs face

Female-led businesses often operate in industries that are hardest hit by economic downturns – such as retail, consumer services and B2B/public services. They are also more likely to need to balance home and caregiving responsibilities, which means their financial needs and expectations differ from men.

Some banks are starting to recognise this and offer tailored solutions, yet female business owners often don’t feel they get the support they need from their bank.

- In Australia, only 36% of female SME’s feel they are getting the support they need from their primary bank, compared to 49% of men, and only 29% of women vs 36% of men feel their bank consistently demonstrates that it values their business.

- In Canada female entrepreneurs are also less satisfied, with 60% being satisfied with the quality of service from their bank vs 71% of men.

- In APAC the picture varies, with lower levels of satisfaction with their main financial provider in Hong Kong (58% vs 66%) and Malaysia 68% vs 76%) but higher satisfaction in Mainland China (77% vs 72%) and Singapore (73% vs 65%).

- In the UK and US though, women feel equally if not more satisfied with the quality of service they receive from their main bank (UK 59% vs 52%, US, 59% vs 62%).

Growing sales and revenue is the biggest challenge for female-owned SMEs across the UK, Canada, the US and APAC. They often face greater challenges in accessing lending and credit compared to their male counterpart (14% vs 8% in the UK, 21% vs 19% in the US and 18% vs 16% in Canada). The situation in APAC is more equal – but a much higher proportion of both males and females face challenges when applying for credit and finance.

In Australia, cashflow and business demand are the main challenge, much more so for women than men (40% vs 29%).

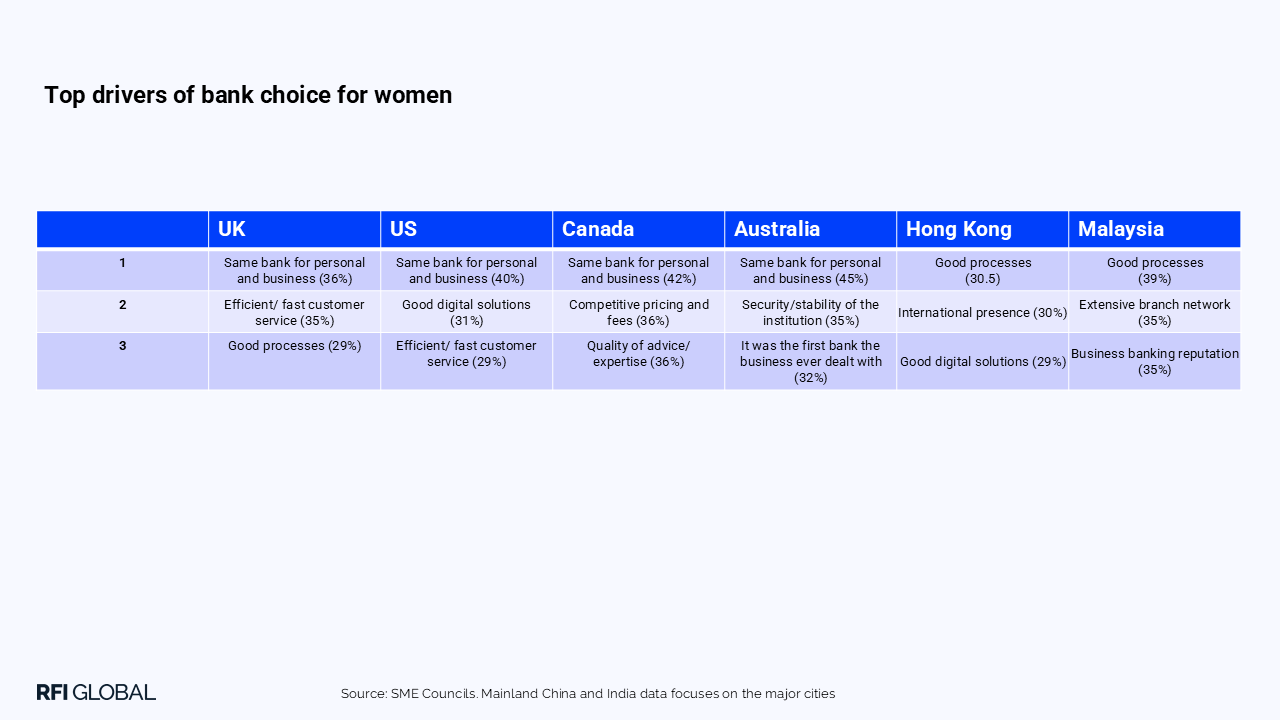

What female entrepreneurs want in the West

For female entrepreneurs in the West, convenience and familiarity drive bank choice in the UK, US and Canada. Around two-fifths of female SME owners simply stick with the bank they already use for personal banking. However, efficient customer service, high-quality advice, seamless digital solutions, competitive pricing and well-structured processes also play a crucial role in shaping their banking decisions.

Beyond this, efficient customer service, quality advice, good digital solutions, competitive pricing and good processes all play an important role.

Female-owned SMEs seek greater transparency in decision-making and more commitment to their long-term growth from their main banks. This is a key driver of advocacy and unmet needs. They prefer face-to-face interaction when seeking business advice and applying for loans, while they lean towards digital channels for banking product information and opening new accounts.

What female entrepreneurs want in the East

In Australia, familiarity is also the top driver of bank choice, with 45% of female SME using their personal provider for their business account. Over one-third also highly value the security and stability of the institution. However, female SME owners face unmet needs in areas regarding customer service and products that align with their business needs. Overall, Australian female SME owners are looking for tailored support from a reputable bank they can trust.

In Hong Kong and Singapore, efficient banking processes are the top priority for female entrepreneurs. Beyond that, reputation plays a significant role, whether through an international presence or a strong standing in business banking. Female SME owners in these markets seek banks that not only provide seamless operations but also demonstrate credibility and stability.

In Mainland China, Malaysia and India, the most pressing unmet need is access to financial products that truly align with business needs. Many female entrepreneurs in these countries feel that existing offerings are too generic and do not cater to the unique challenges and growth ambitions of their businesses. They are looking for more innovative solutions that provide flexibility and tailored support.

For female SMEs in Hong Kong, account management emerges as a critical gap. Business owners want stronger, more dedicated relationship management, with banks that take a proactive approach to understanding their businesses and providing strategic guidance. Meanwhile, in Singapore, greater transparency in decision-making is a key concern, with female entrepreneurs seeking clearer communication and rationale behind banking decisions, particularly in areas like lending and financial support.

These unmet needs highlight significant opportunities for banks and financial institutions to deliver more personalised, growth-focused solutions – helping female entrepreneurs not only manage their businesses more effectively but also scale them with confidence.

How banks can step up

The rise of female entrepreneurs presents a significant opportunity for banks and financial institutions to better serve this growing and ambitious segment. Yet, many female-led SMEs still face hurdles in accessing the financial support they need to thrive.

As Kathryn Petralia says, “there is a need to make financial services more accessible and less judgmental through data-driven decisions and online platforms. The appeal of this is evident in the growth of fintechs amongst women.”

Banks that offer adaptable funding solutions, proactive guidance, seamless processes and tailored solutions as well as a genuine commitment to the long-term success of female-led SMEs will be the ones to foster stronger loyalty and advocacy.

By addressing the unique needs of female entrepreneurs with smarter, more inclusive solutions, banks can empower women-led businesses to scale and grow.

Get in touch for more insights from our SME surveys where we speak to over 60,000 business leaders every year.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.