A few weeks ago, I opened a business bank account. It’s almost twenty years since I last did this, and during that time I have watched with interest as an industry participant as digital banking has emerged, developed and grown. At RFI Global, we have collected, analysed and reported on SME banking data since 2010, so this is my chance as a customer to see how much progress had been made.

I was also curious to understand the UX that the fintechs and neobanks now provide. While we track their increased market share and SME appetite for them with regular surveys, they didn’t exist last time I opened a business bank account.

I should at this point note that from a research perspective there is nothing more dangerous or prone to erroneous conclusions than a survey sample of one so I’ll look to qualify my experience with robust data.

High street bank or neobank?

I selected two high street banks in the UK and two neobanks. The first high street bank’s website froze a number of times and then suggested I email a help desk instead – so they were out. One of the neobanks required you to download an app, customer registration included various annoying questions before I even started – so they were out. I was now running a true AB comparison test between a single high street bank and a single neobank. After 45 relatively pain free minutes, I was done with the high street bank. All the new bank account details would be verified, and I would be contacted in a few days with the new account, and my card would follow a week or so after that. I then tried the neobank. Approximately 120 seconds later I was all done with the account set up and all the detail sent to me. On top of that the new card arrived the next day. I was stunned.

Frictions and pain points for SME’s

RFI data shows that SME owners have significantly more pain points and unmet needs than consumers. Up until now most neobanks have focused mainly on consumers. It is undeniable that in the US and UK they are making serious in roads into consumer market share. Nearly one in five (17%) new primary accounts are now with neobanks in the US. In the last two years the neobanks like Chime, SoFi and Synchrony have signed up more people than Chase and Bank of America combined.

It was fascinating listening to my cohost on Banking Uncovered, Chloe James, chat with Kathryn Petralia, co-founder of Kabbage and Keep Financial in this episode of the Banking Uncovered podcast. The exact same problems they were looking to solve back in 2008 still need to be solved today. In those days as Kathryn says banking services were being disaggregated and fintechs were providing single vertical solutions. Now SME customers want all their banking in one place and as she points out providers are now reaggregating their offerings using technology.

According to RFI data, the number one reason for switching away from the high street banks in the UK is to get better mobile banking. Kathryn talks about how when she was building Kabbage the goal was to provide transparency. As you can see below, the main drivers of switching bank in the UK are better innovation in digital banking and transparency.

As we can see below, the drivers of acquisition for the neobanks are simpler, easier, better quality and an easier and faster application process. If I think back to my survey sample of one and the 120 seconds it took me to apply then it appears that RFI’s quantitative statistically robust SME data validates my experience 😊.

If Kathryn was launching Kabbage almost twenty years ago to provide transparent and easy banking for SMEs, then how have we ended up here? Have the banks failed to up their game or are they just moving slowly? The recent closure of Zing by HSBC shows the struggle the big banks have, even with their huge resources if they fail to genuinely understand the customer pain points and the need in the market.

So, what can the high street banks do in the face of the onslaught from neobanks?

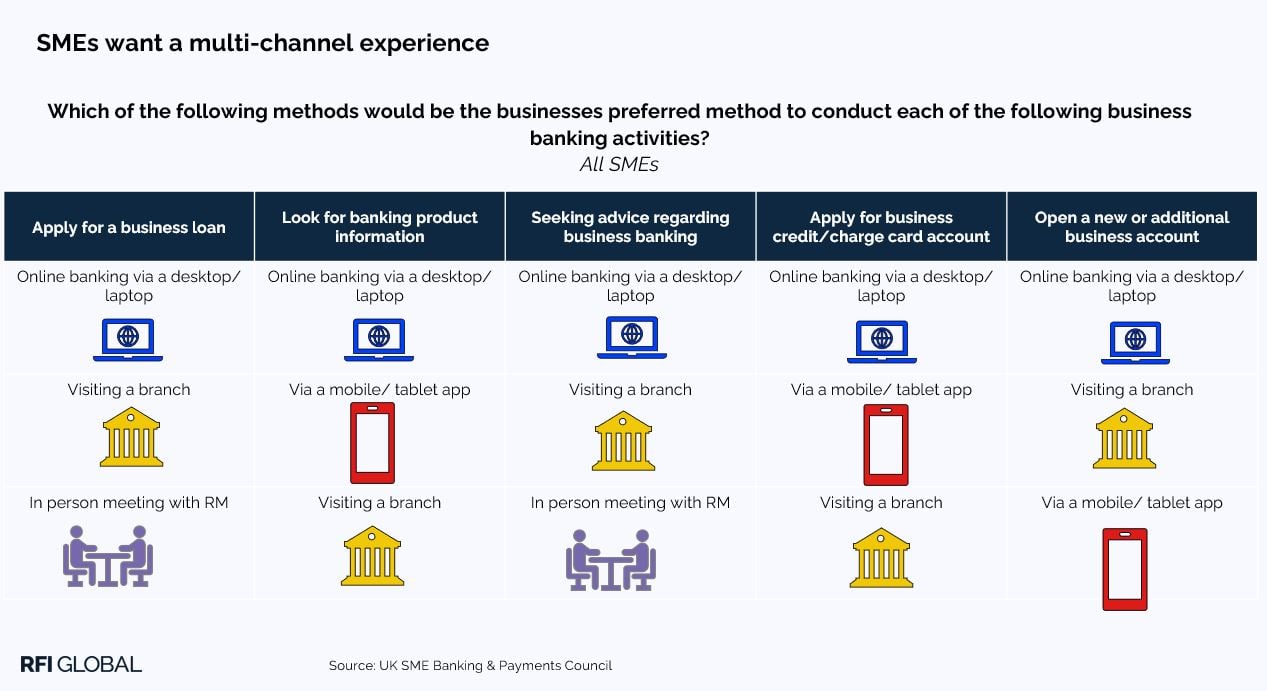

As our data shows, being digital isn’t enough. SMEs still want a multi-channel experience with visits to a branch and talking to a human still key to great overall UX. If they can focus on delivering a great digital UX they will have a competitive advantage with their RMs and their branch network. However, with the likes of Alica Bank providing innovative solutions to meet these same needs, hence their impressive ranking as Europe’s fastest growing tech co, and the neobanks continuing to improve their offering in this space, the high street bank’s timeline to achieve this is diminishing rapidly. This throws the recent decision by Lloyds to close a further 136 branches into sharp relief and we will watch with interest the impact this has on their SME clients.

Back to my survey sample of one and I’m still stunned by the 120 second start to finish application and the card in my hand the next day – don’t even get me started on how great the app is to use.

Get in touch for further insights from our UK SME study, and watch the podcast with Kathryn Petralia, co-founder of Kabbage and Keep Financial.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.