All bets are off in 2024 when it comes to retention – loud budgeting and the big switch

In the past I’ve written a lot about the cost of living and the way it is impacting on consumers. At the end of 2023, I focused on personal financial management (PFM) tools and the way that younger consumers valued them alongside support from their banks.

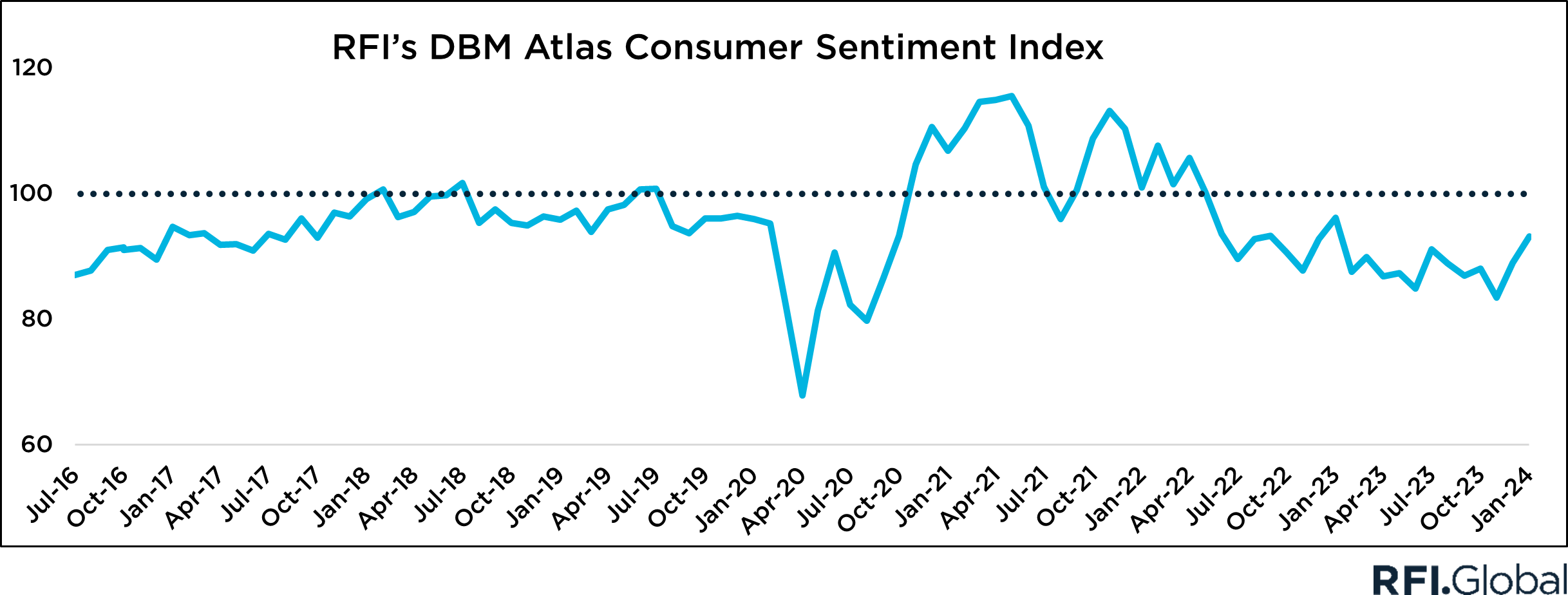

As at January 2024, RFI’s Atlas Consumer Sentiment Index was edging upwards, but I would categorize the movement as less negative rather than more positive. Consumers are still feeling the pinch when it comes to groceries, fuel and debt repayments and so I don’t see the desire to budget and be supported becoming less important in 2024.

Loud Budgeting

Against this backdrop, I learned a new term being used by young adults; “loud budgeting”. For those of you not as tapped into youth culture and TikTok as me (I am not on TikTok, I read about it in the Guardian), loud budgeting is the practice of sharing your fiscal intentions with your friends and family, rather than keeping them to yourself. The term was coined by TikTok comedian Lukas Battle as the new trend for 2024.

This makes a lot of sense, given what we’ve seen in our data. In 2021 RFI did a study of 1,000 16-21 year olds, which revealed that more than half (55%) were already budgeting in some way, 52% discussed banking and finance topics with their parents and 37% discussed these topics with their friends. In 2024, these 16-21 years olds are in the 18-24 cohort that is now leading the charge on loud budgeting.

A big switch?

With sentiment languishing and consumers stating publicly that they are going to be saving money and tightening their belts, I started thinking about what might happen in 2024 from a consumer perspective.

In a time of crisis, often barriers will come down and the environment presents challenges/ opportunities that otherwise would not have existed. In looking through RFI’s data I believe that retention will be the battleground that banks need to focus on.

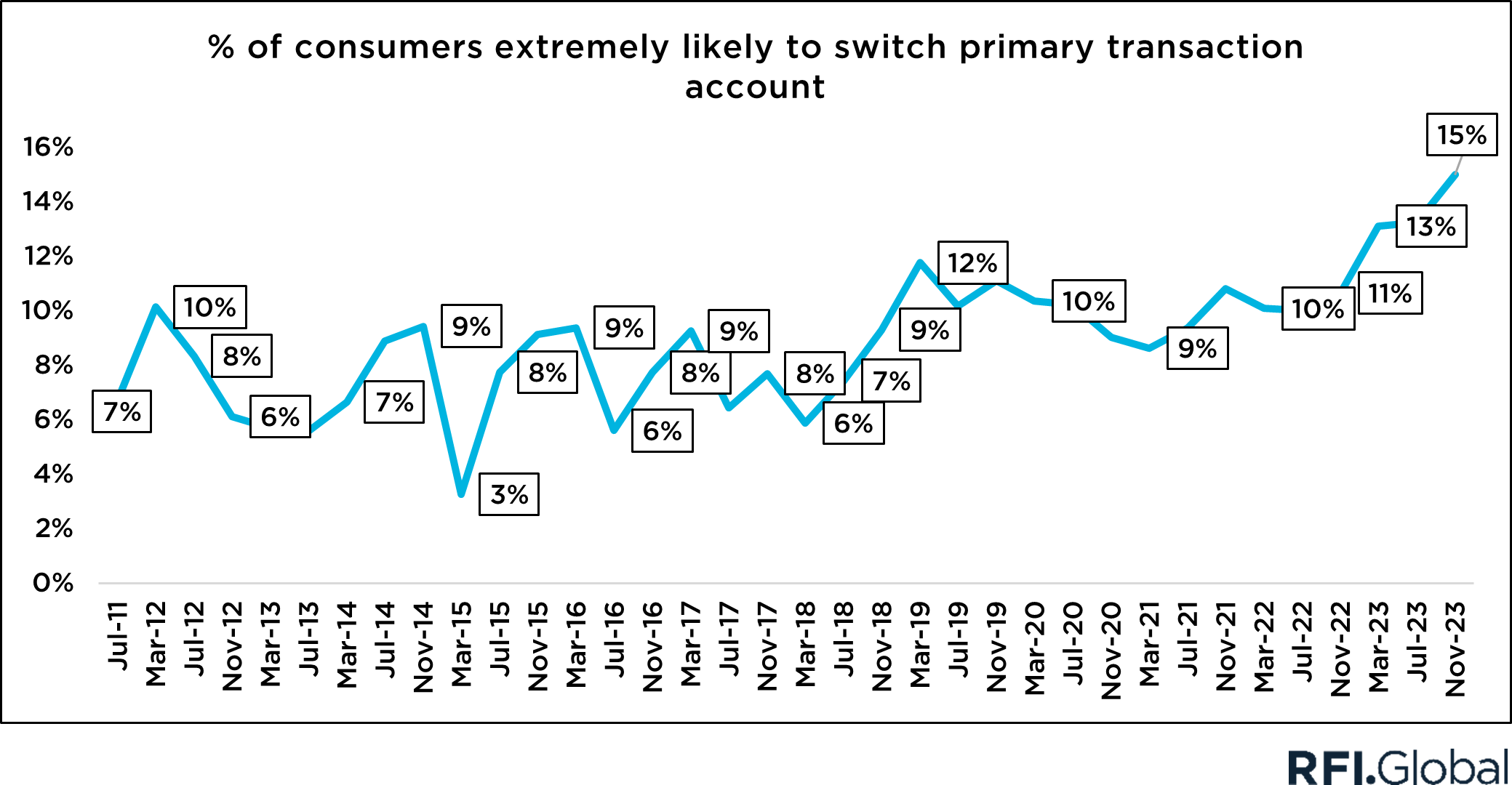

Since the early days of RFI we’ve always been keen to understand consumers’ propensity to switch banking relationships, which means that we have some fantastic longitudinal data to draw upon. This data shows that at the end of 2023, switching propensity for primary transaction accounts was higher than we’d ever seen it before at 15% – which is to say that one in six consumers said they were extremely likely to switch in the next 12 months. Not just a little bit likely. Extremely likely.

Do we care about primary transactional relationships? We ought to. The overlap between these and main bank relationships is 91%. Do we care about main bank relationships? JK.

And which group is most likely to switch? The loudly budgeting 18-24 year olds. One in four of whom (23%) describes themselves as extremely likely to switch.

All bets are off

So why are we seeing this trend? To a degree, all bets are off when consumers are in the trenches and struggling. They are changing the way they spend and save and they will change their underlying banking services if it makes sense to them and makes them feel smarter and more comfortable.

On the other hand, when consumers are in this mindset, they are also evaluating what they get back from their banking providers. Are they valued? And the answer from many is that they don’t feel like they are. The top three reasons cited by the 15% of potential switchers are:

- I am a long term customer and I have not been rewarded

- I want to access a better rate on my linked savings account

- I have been offered an incentive by another institution

It’s hard to argue that these are not about consumers demanding more in return for their custom.

So, what should banks do?

Clearly this is both a retention risk and an acquisition opportunity depending on your perspective. The success on both counts will lie in providing customers with the twin outcomes of greater support to manage their finances and a more tangibly rewarding experience as a customer.

These things sound different at first glance, but can be part of the same thing – by understanding customer needs at an individual level, banks should be able to look to leverage generative AI and other technologies to provide consumers with tips, nudges and tools that help them manage their finances in a smarter way, while ensuring they have access to discounts and loyalty rewards that are relevant and desirable.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.