With Christmas fast approaching – I caved into pressure and we put our decorations up at the weekend – and interest rates once again rising, there is a lot of talk in the media about the cost of living and the affordability of housing. Of course, rising costs of groceries, fuel, loans and accommodation don’t affect all consumers equally and it got me thinking about the segments of the population that are most impacted.

This coincided with me being asked to present to one of our nation’s banks on the needs and wants of the under 35’s. Of course, this is the very group of consumers that is staring into the housing affordability crisis and seeing the prospect of homeownership diminish.

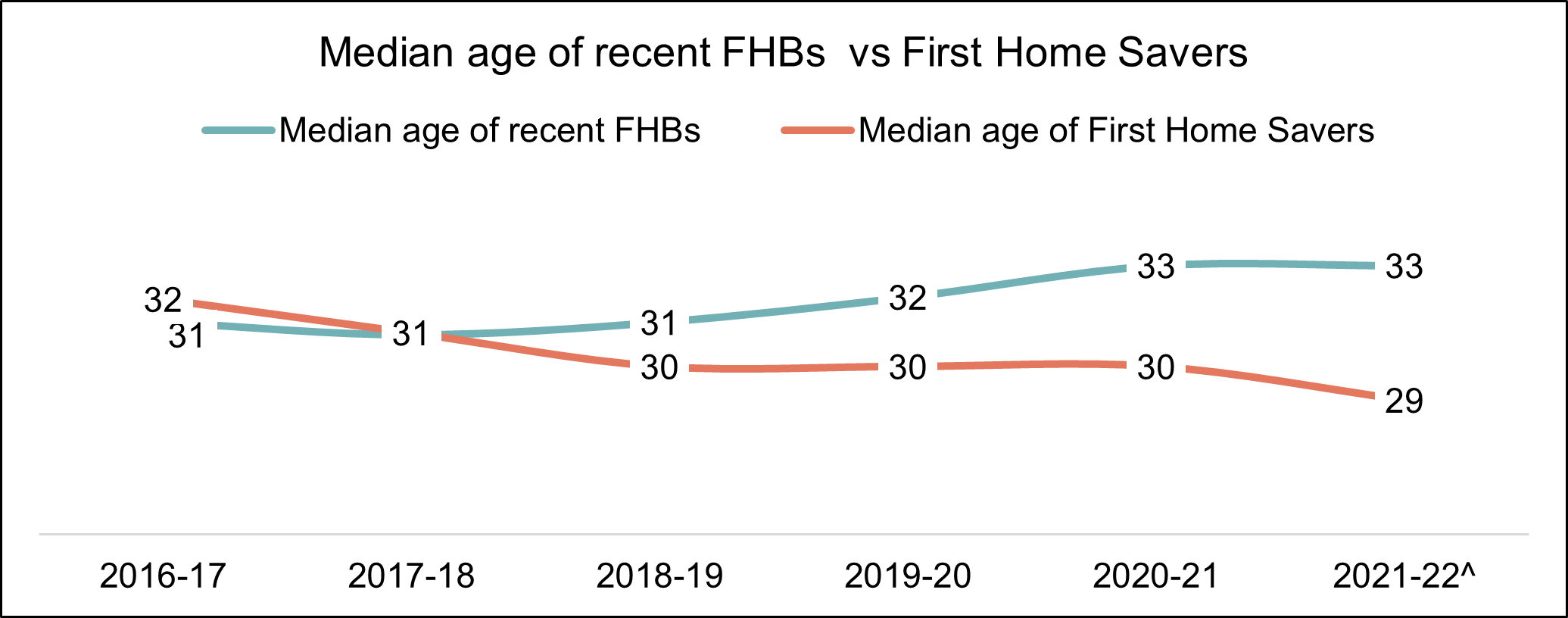

That is not to say that younger Australians’ desire to own property is waning – as RFI’s data shows, the median age of someone saving for their first home deposit is declining, while the average age of a first home buyer is increasing.

In addition to issues of housing affordability, going forward there will be the issues associated with an ageing population. In August, former Secretary of the Treasury, Ken Henry described what he saw as an intergenerational tragedy with young Australians today increasingly funding the cost of an ageing population through personal income tax.

How can banks help?

Clearly banks can’t help with taxation policy and their role in housing affordability is somewhat hamstrung by the cost of funding home loans. So what role can they play in helping younger Australians ensure they have a brighter future?

When it comes to needs, this is a group of consumers that uses and is open to using many different apps that make it easier for them to save, budget and monitor their spending. Indeed, while across the whole population nearly one in five use a personal financial management (PFM) tool, among the under 35’s this proportion is 32% compared to 6% among the over 45’s.

Here it seems banks can help. Who better to provide the tools that enable a consumer to manage their finances in a sensible way.

Are banks helping?

The question we must now ask is ‘are banks providing customers with the tools that they need?’. In order to answer that, let’s start with the pain points that consumers have with their banks and because we’re talking about 18-34 year olds, let’s focus on mobile banking – which is the predominant way this group interacts with their bank.

When we look at an experience quadrant of mobile banking among the under 35’s we see that there are certain attributes that are highly correlated with mobile banking satisfaction (those elements in the right hand quadrants) and certain attributes that are less than satisfactory (those elements in the bottom two quadrants).

Across the entire banking landscape for 18-34 year olds there are two elements that fall in the bottom right hand quadrant, which I will call the pain points. And one of those is ‘accessing savings and budgeting tools’. In fact this is the element that is most highly correlated to overall mobile banking satisfaction and it’s not satisfactory.

Specifically what is needed?

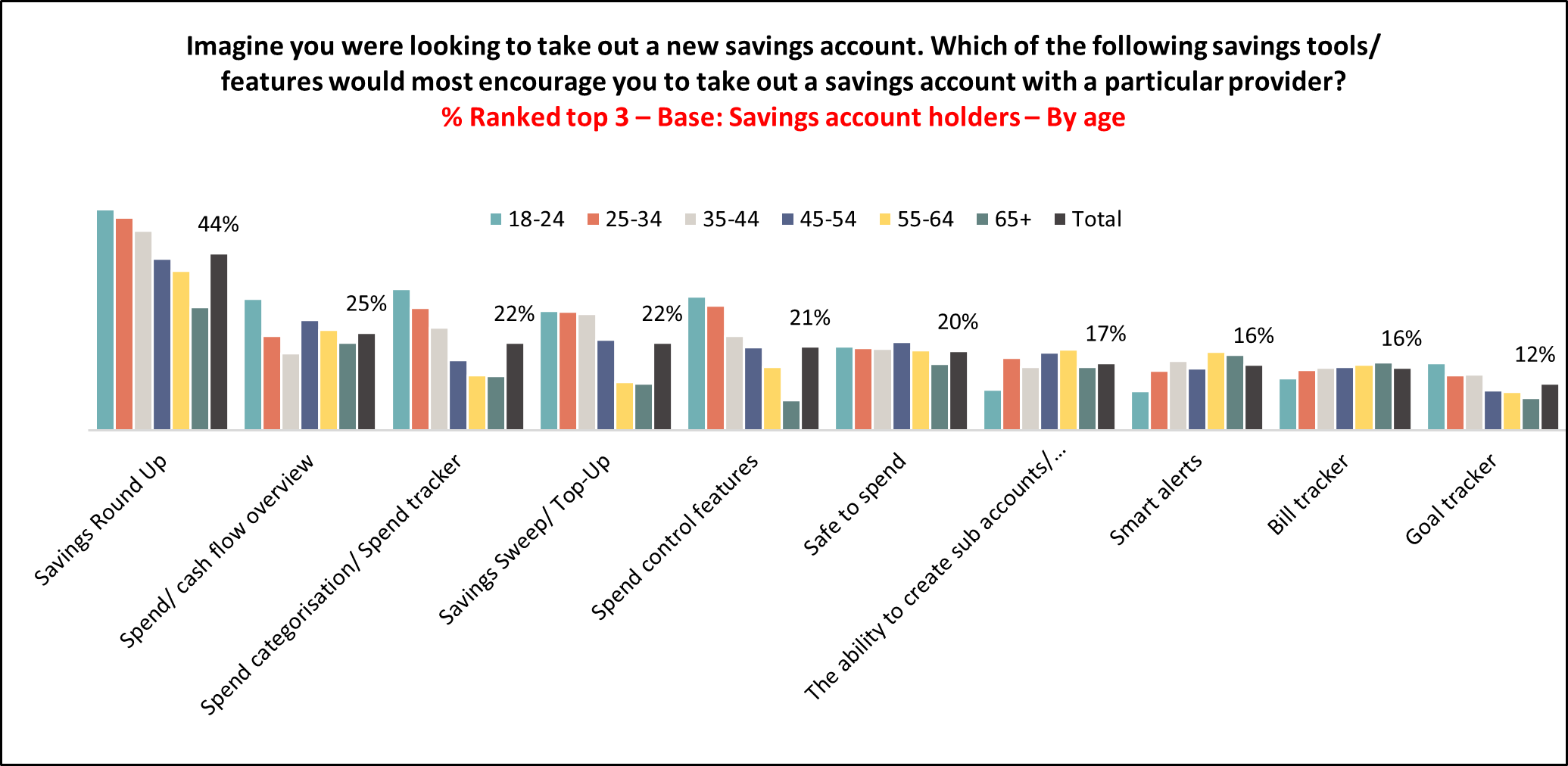

So what tools would these 18-34 year olds like to see from their banks? RFI’s study of savers conducted in August this year showed that they want the following five things the most:

1.Savings round up features

2.Spend/ cash flow overview

3.Spend categorisation

4.Savings sweep/ top up

5,Spend control features

All of these help them to better understand their outgoings and their budget position, while making it easier for them to save by using small incremental movements of money in their accounts.

So will these features add value?

The sceptics among you may ask whether a bank might invest in all of these things an end up with a customer base that either doesn’t use them or doesn’t value them. Let me leave you with one final piece of data.

When we look at the NPS scores among 18-34 of Australia’s digital banks (who lead the way on NPS nationally), then we find that the number of PFM features they offer to customers decreases with their NPS score. I.e. the bank that offers the most PFM features has the highest NPS among 18-34 year olds.

These consumers are going through a rapid increase in financial complexity in their lives at a time when there is a cost-of-living crisis, a housing affordability crisis and (in the words of Ken Henry) a looming intergenerational tragedy.

So, will these features add value? Yes. Maybe not in time for Christmas, but for the future.

* AFR stands for Any Financial Relationship and means that it includes ALL customers of the bank** The fourth ranked bank’s NPS is in the ascendancy and if it continues it will overtake the third placed bank in the next couple of months

*** The fifth ranked bank has an additional mobile app that is not available to all customers

**** The sixth ranked bank launched a new app with more features in June 2023

Get in touch for more insights.

Subscribe to get the latest RFI data and insights.

About the Author

Alan Shields is the co-founder and a director at RFI Global, he oversees the design, roll-out and delivery of syndication and custom products to RFI Global’s clients globally. Alan has more than 20 years’ experience in research analysis and has spent his entire career focused on financial services across the globe including Europe, North America, the Middle East and Asia Pacific.

He has worked on syndicated and bespoke projects with every bank in Australia and New Zealand, with most major banks in the Asia Pacific region, as well as the major global banks. Prior to setting up RFI Global in 2006, Alan was Head of Financial Services – Asia Pacific at global research firm, Datamonitor, establishing Datamonitor’s financial services business in the Asia Pacific region in 2004, after relocating to Sydney from London. Alan began his career with Reuters in London as a financial services consultant, where he worked on the Nasdaq Europe project before moving to Singapore and focusing on wealth and risk management in the region. He is a regular speaker at thought leadership events across the US, Canada, Europe, Asia and Australia and authors regular articles on the latest global consumer banking trends.

He has a Bachelor of Science Degree in Physics from the University of Birmingham and studied his License de Physique at the Universite de Bordeaux I.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.