Edward Smith, Lead Analyst, North America & EMEA

Annuities are carving a niche among affluent consumers looking to guarantee their retirement income. Our data shows that annuity owners are proactive retirement planners, focused mainly on transferring their wealth to the next generation.

Historically considered to be overly complex and rigid, annuities have not had the best reputation. While most US households still hold this sentiment, our MacroMonitor household survey reveals that total market ownership of annuities has steadily increased from 12% to 16% between 2016 and 2024.

Financial institutions can uncover better ways of promoting annuities and associated advisory services by examining the conditions that encouraged annuities to flourish, the wider financial goals of annuity owners, and the new dynamics of annuity relationships.

Retirement concerns grow

Ensuring sufficient savings for retirement has always been a key financial goal for US consumers. Among retired households, 58% express concerns about living on a fixed income. For the non-retired segment, the years surrounding the average retirement age are fraught with anxiety, as indicated by the stark uptick in interest among those aged 55-64 to boost their income before they retire.

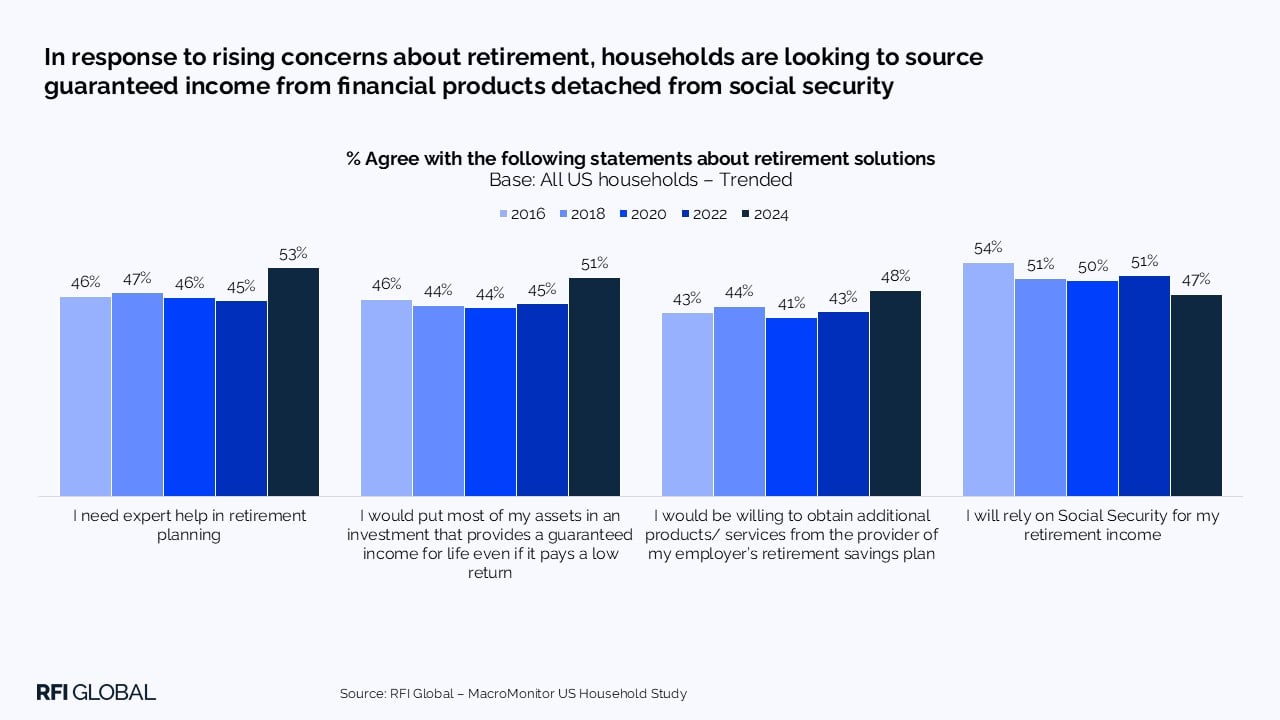

Consumer confidence has also worsened since the pandemic: in 2024, 64% of US households worried about having adequate income for retirement, up from 59% in 2020. More households are worried about outliving their retirement savings and many fear that they will need to either work past their expected retirement age or make significant changes to their lifestyle to live comfortably after employment.

Guaranteed retirement solutions gain popularity

In response, 2024 marked a significant shift in attitudes towards retirement solutions. ‘Guaranteed current income’ displaced financial security as the primary factor driving household choice of savings and investment vehicles. Half of households said they were willing to invest in low-return solutions that guaranteed lifelong returns.

With fewer households relying on social security and demand for expert retirement advice surging, annuities are well-positioned as a low-risk solution for those looking to diversify their retirement savings. This deal is sweetened by the relatively high annuity rates of recent years.

Annuity owners focus on what comes next

In their financial goals, annuity owners share the same priorities as the average household, like paying off debts, financing big-ticket items and taking vacations – except for two key areas:

- Annuity owners are significantly more likely to consider providing for future medical needs (36% prioritize vs 22% of non-owners).

- Annuity owners are almost twice as likely to be considering how they can provide for heirs, children or grandchildren (31% vs 17%).

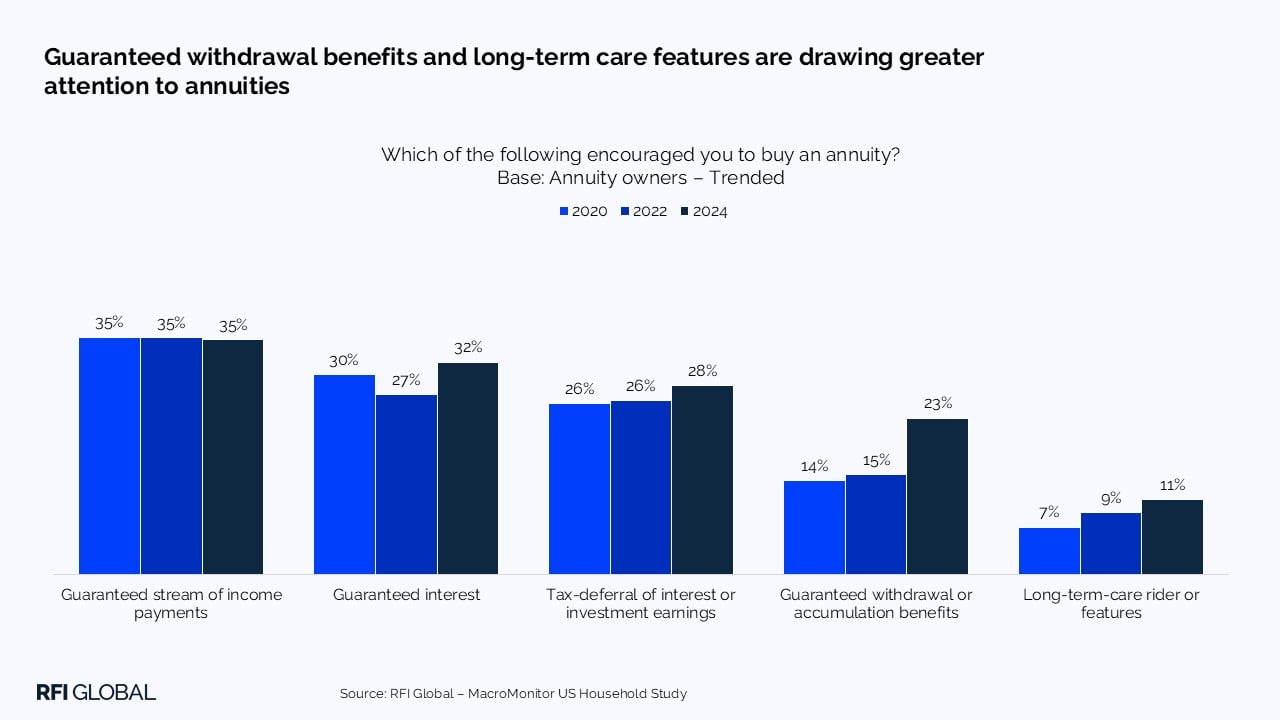

When asked why they took up their annuity, buyers usually cite access to a guaranteed income stream as the main reason, with interest guarantees and tax-deferral being similarly influential drivers. Withdrawal and accumulation benefits have also drawn more attention to the product, indicating that recent steps to make the restrictions of annuities more palatable are effective for encouraging uptake.

Annuity owners essentially leverage the stability that annuities afford to focus on what matters most to them: handling long-term-care needs and managing assets in service to transferring wealth to dependents. Given that buyers care greatly about the welfare of their wider family unit, promoting estate planning services as part of the annuity package would further reinforce the value proposition.

Our data shows that this would be doubly effective for the growing segment of Asian and Hispanic annuity owners who have traditionally received less exposure to comprehensive retirement planning.

Trust and consistency shape annuity relationships

Customer engagement with annuities has transformed over the last decade. Take the point of sale, for example. Before the pandemic, households typically purchased annuities from financial-planning or insurance company agents; since then, buyers are more likely to go through independent financial planners or bank representatives. As such, having a trusted point of contact is increasingly vital for annuity adoption.

The means by which annuities are funded has also changed. Ten years ago, a lump-sum purchase from a savings pot was the norm for many annuity owners. Nowadays, most annuity owners pay into annuities through fixed or variable payments. Moreover, while salary contributions remain the primary source of funds, a growing proportion of annuity owners add contributions from deposit accounts, tax refunds and stock dividends—in other words, they are consolidating small, excess returns into their annuities.

Combined, policy holders are more likely to be forward planners, demonstrated by the declining proportion of annuitized annuities (34% in 2018 vs 26% in 2024). Recognizing that buyers are in for the long haul, annuity providers should look to introduce annuities to prospective customers earlier, ahead of retirement, and highlighting ways for buyers to aggregate funds separately for household longevity and dependent support.

Annuities: A proactive solution to market instability for the future-minded

The picture of market trends in retirement attitudes, household priorities and product interaction is tailor-made for annuities to establish a firm niche for affluents keen on transferring wealth. To stand out from the competition, financial institutions should:

- Establish their brand as a reliable source of retirement information as early as possible and take steps to formalize this relationship when the customer is around their mid-forties. For care-conscious customers, position annuities not as a personal investment, but as the supportive backbone to their future care plan.

- Involve customers’ dependents in retirement product propositions. Annuities are often taken out with the implicit purpose of supporting the family unit, so ensuring these other members are engaged can minimise friction if the original buyer passes. Additional cross-sell is a potential bonus.

- Advocate for early adoption by presenting annuity payments as a consolidation method. Savings pots for regular spending are increasingly popular, and an equivalent for longer-term retirement savings would complement this nicely—particularly if accompanied by a transparent tool that helped users identify what excess funds would be best in an annuity or a higher-return alternative.

In closing, it’s important to acknowledge that awareness of annuities is still somewhat limited. Even among those that hold them, a sizeable amount are unsure of the exact conditions of their annuity, demonstrating that institutions have a long way to go before interaction with annuities is normalised.

Get in touch to explore further insights from our MacroMonitor survey of US household financial behavior.

Edward Smith

Lead Analyst, North America & EMEA

Edward Smith is a Lead Analyst at RFI Global, covering financial services trends across North America and EMEA.

View full profileFrequently Asked Questions about annuities

Q: Why are annuities becoming more popular in the US?

Annuities are becoming more popular in the US because households increasingly prioritize guaranteed retirement income over higher investment returns. MacroMonitor data shows annuity ownership rising from 12% in 2016 to 16% in 2024 as retirement income anxiety grows.

Q: Are US households willing to accept lower returns for guaranteed income?

US households are willing to accept lower returns because guaranteed income reduces the risk of outliving retirement savings. Half of households say they would invest in low-return solutions if they provide lifelong income, reflecting concerns about fixed incomes and retirement security.

Q: Who typically owns annuities in the US?

Annuities are most commonly owned by proactive retirement planners approaching or in retirement. These households are more likely to prioritize long-term care needs and providing for heirs, children or grandchildren compared with non-owners.

Q: How should financial institutions respond to rising annuity demand?

Financial institutions should engage customers earlier and position annuities as part of a broader retirement income and wealth transfer strategy. Trust-based advice, family involvement and flexible contribution models are increasingly important.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.