In the rapidly evolving financial services landscape, US companies are increasingly targeting diverse groups such as Black, Asian, and Hispanic populations. This strategic focus is driven by several key incentives: the potential for market expansion as these demographic groups continue to grow, the opportunity to unlock significant buying power in historically underserved communities, and the need to align with regulatory mandates like the Community Reinvestment Act. Additionally, as public pressure mounts for more inclusive practices, companies are embracing diversity initiatives to foster trust, loyalty, and competitiveness.

By addressing the unique needs of these populations, financial firms are not only seizing growth opportunities but also positioning themselves for long-term success in an increasingly diverse economy.

Understanding financial needs

The financial landscape is marked by significant disparities, with many households struggling to achieve financial stability, while others live in affluence. However, these challenges—and the solutions required to address them—vary significantly across different demographic groups. To build a more equitable financial future, it’s crucial for financial services providers to recognize and address the unique needs of these diverse communities.

Data from MacroMonitor, the largest survey of the financial needs, attitudes and behaviors of US households, uncovers the specific needs of often hard-to-reach minority groups including Black, Hispanic, and Native households.

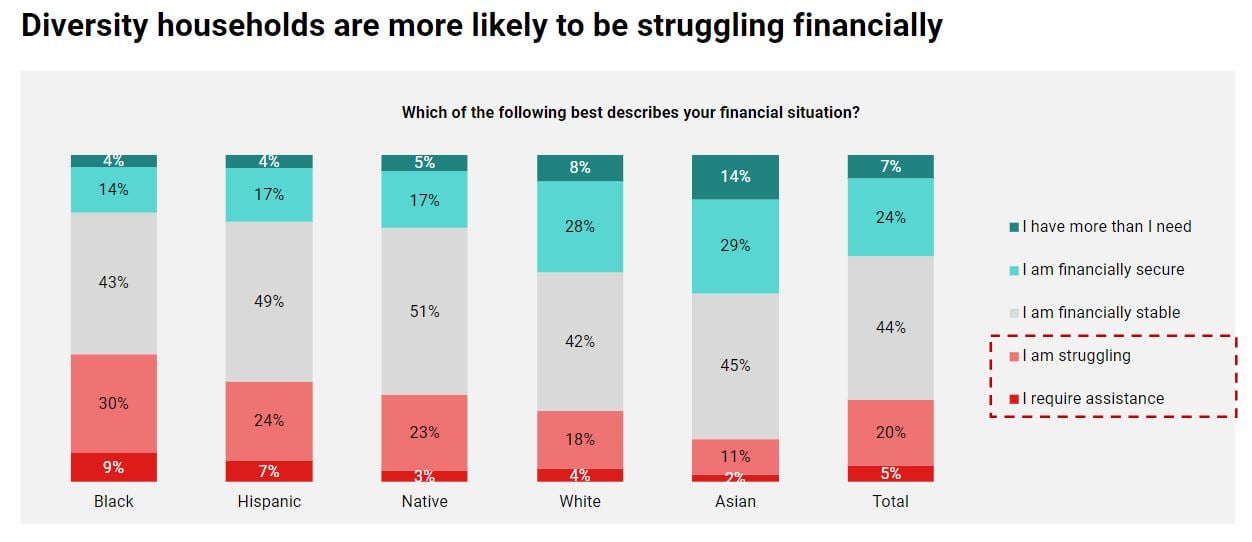

A significant portion of US households, particularly those within Black, Hispanic, and Native communities, are vulnerable, they face considerable financial difficulties. We have defined vulnerable households as those who have no savings or investments, are underbanked, regularly overdrawn or struggling financially. With one in four households struggling financially, there is a clear and urgent need for targeted support from the financial services sector. The data shows that Black households are significantly more likely to face financial challenges and require assistance.

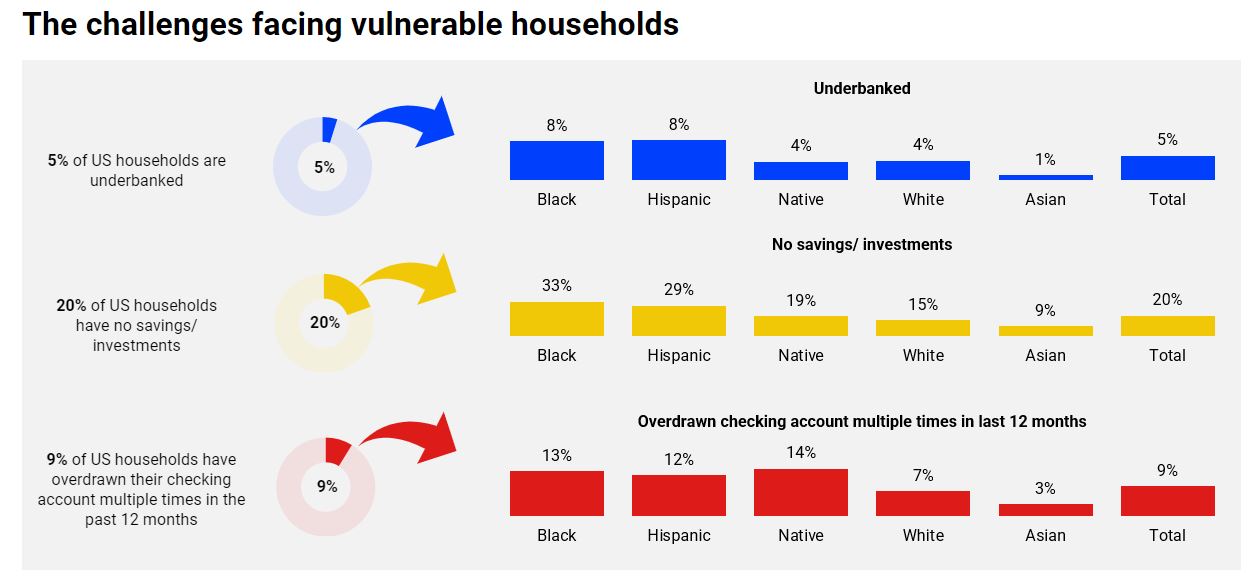

The challenges facing vulnerable households

One in three vulnerable households is concerned about their debt levels. Financial services can address this by offering debt management tools, financial counseling, and more flexible repayment options tailored to individuals with lower credit scores.

About 5% of households are underbanked, lacking sufficient access to traditional financial services like checking or savings accounts. Financial institutions can address this by expanding services in underserved areas, offering low-fee accounts, and increasing financial literacy efforts to help these households better manage their finances.

Savings and investment access

A staggering 20% of households have no savings or investments, leaving them vulnerable to financial shocks. Financial services can support these households by providing accessible savings products, encouraging micro-investments, and offering incentives for building emergency funds.

Developing products that cater specifically to the needs of vulnerable households can make a significant difference. For example, creating savings accounts with no minimum balance requirements or offering small-dollar loans with reasonable interest rates could help bridge the gap.

Financial education programs

Financial literacy is crucial for helping households manage their money more effectively. Financial services can play a vital role by offering workshops, online resources, and one-on-one counseling to improve financial understanding and decision-making.

Innovative financial technologies

The growing interest in financial innovations like Buy Now Pay Later (BNPL) services among sub-prime credit households indicates a need for alternative financial solutions. Financial institutions can develop and promote products that offer flexibility while helping customers avoid excessive debt.

Empowering Asian households through Financial Services

Asian Americans represent one of the fastest-growing wealth segments in the United States. Unlike many vulnerable groups, Asian households tend to have stronger financial positions, with higher levels of education and investable assets. However, financial services can still play a crucial role in supporting their unique financial goals and preferences.

Asian households are significantly more likely to have a financial strategy, and their confidence in achieving financial goals increases with assets. Financial services can further support these households by offering advanced financial planning tools, personalized advice, and products that align with their long-term goals.

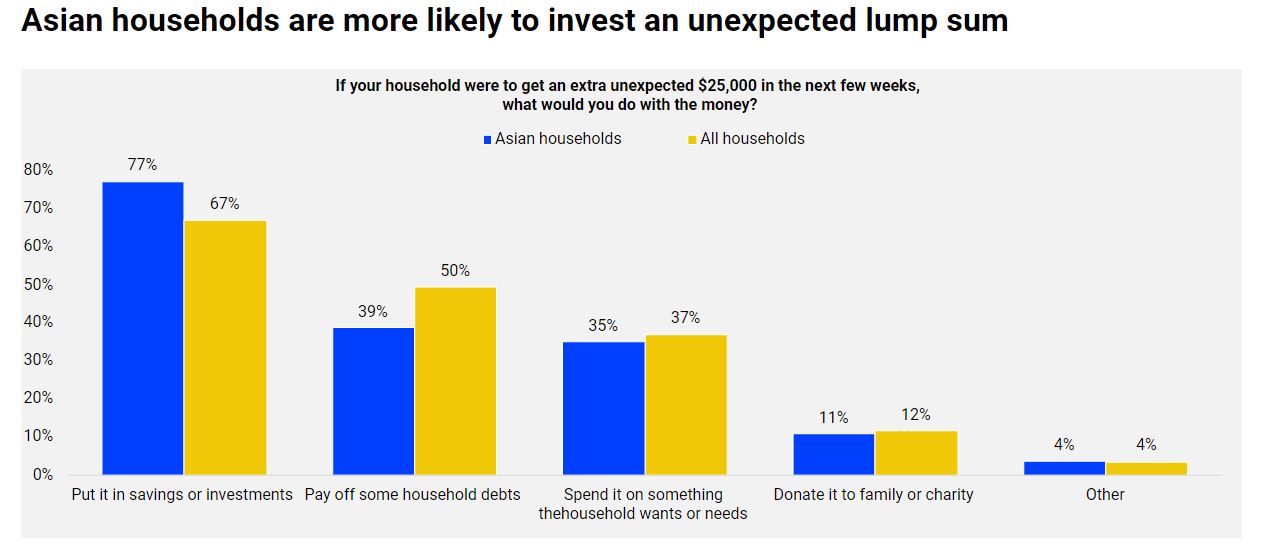

Asian households also exhibit a strong preference for savings and investments. They are more inclined to invest an unexpected lump sum into these products, prioritizing goals like retirement, emergency funds, and travel. Financial Services can cater to these preferences by providing a wide range of investment options, from low-risk savings accounts to higher-risk securities.

While Asian households are generally more willing to take on investment risk, they also value professional advice before making major financial decisions. Financial institutions can support these households by offering comprehensive advisory services, personalized investment strategies, and risk management tools.

What Asian households want

Tailored investment products: Investment products specifically designed to meet the needs of Asian households, such as tax-efficient investment accounts, education savings plans, and diversified mutual funds appeal to this audience.

Comprehensive financial planning services: Offering holistic financial planning services that encompass retirement planning, wealth management, and risk assessment can help Asian households achieve their financial goals more effectively.

Enhanced advisory services: Financial institutions can provide dedicated financial advisors who understand the specific cultural and financial needs of Asian households. This could include multilingual support and personalized advice that aligns with their financial values and goals.

Building a more inclusive financial future

To create a more equitable financial landscape, financial services providers must recognize the diverse needs of different communities and tailor their offerings accordingly. By addressing the unique challenges faced by vulnerable households and empowering groups like Asian households with the right tools and resources, financial institutions can help bridge the gap and ensure that all households have the opportunity to build a secure and prosperous future.

Investing in diversity not only benefits the communities served but also strengthens the financial sector as a whole. A more inclusive approach to financial services will lead to a more resilient economy, where all individuals, regardless of their background, can thrive.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.