Tiffany Ng, Client Executive, North America

Despite predictions of their decline, bank branches remain an essential part of the US financial services landscape. Our latest MacroMonitor data shows that more than half of households (53%) visit their current primary bank or credit union branch. And critically, over a third (37%) report talking with a teller in person for a routine transaction at least one to four times a month. These numbers are high, given that most households now rely on mobile apps (77%) and the internet (58%) to manage their finances. Far from being relics, bank branches still play a critical role in how households manage money, make decisions, and build trust with institutions.

The difference is why people use them. Our MacroMonitor data shows that motivations diverge sharply: Baby Boomers turn to branches for long-term relationship building and estate planning, Gen X for guidance during their peak earning years, and Millennials and Gen Z, though highly digital, still seek in-person reassurance at pivotal financial moments.

Boomers: The relationship builders

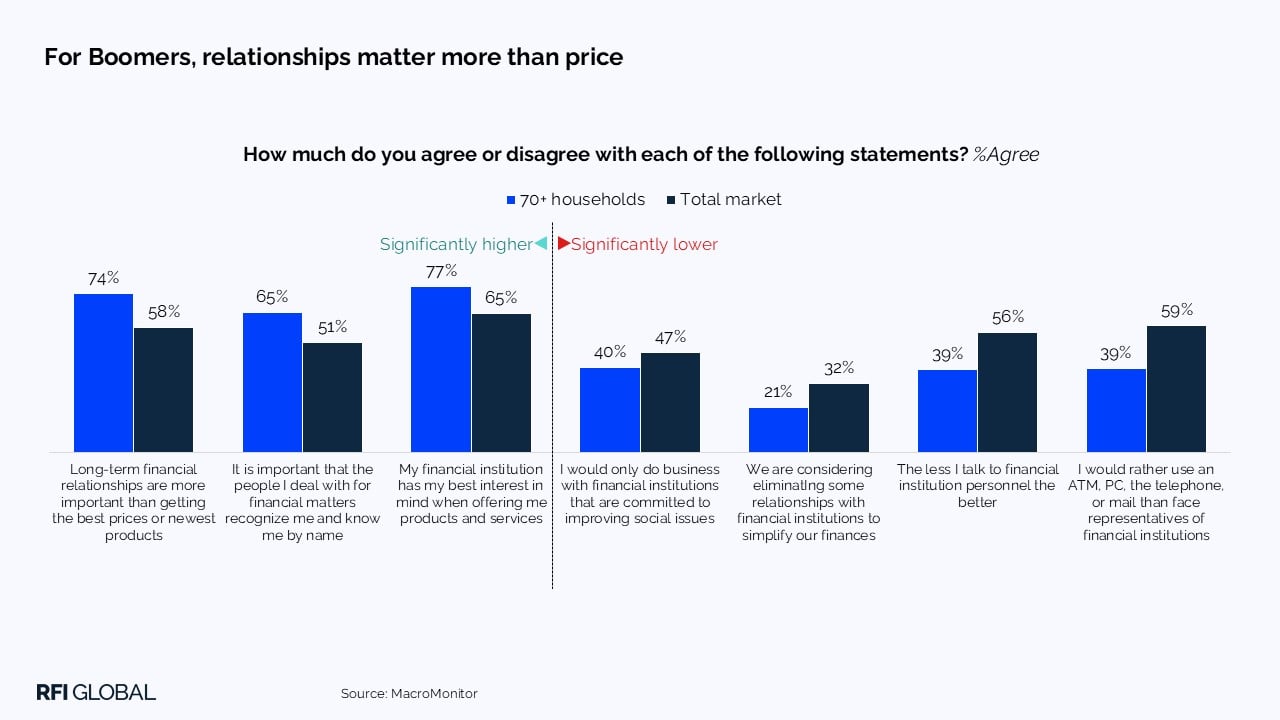

Boomers grew up when branches were the default channel for banking, and that early habit has evolved into a strong preference for personal service today. Our data shows that 74% of households aged 70+ place greater importance on building long-term relationships with financial providers than on always getting the best price, compared with 58% of the average household. 65% also want representatives to know them by name, far above the national average (51%).

They also face major wealth-transfer decisions. Households aged 70+ are projected to transfer $45.05 trillion to the next generation. For this group, branches are not about convenience but about trusted spaces to navigate complex decisions with human advisors.

Gen X: the juggling pragmatists

Gen Xers are in their prime earning years, often balancing children, aging parents, and retirement planning at once. This has earned them the moniker of the ‘Sandwich Generation‘.

Gen X households are more financially established, with 12% reporting annual incomes between $150,000 and $199,900, higher than other cohorts. They are confident using digital tools for routine tasks, with 23% using mobile apps to pay bills compared with 19% of Boomers. Yet they remain cautious about relying solely on technology for financial advice. Nearly half (49%) cite low trust in robo-advisors, and 19% say they require personal interaction to do business with a financial institution.

This combination of financial responsibility, digital comfort, and skepticism toward automated advice underlines why branches remain indispensable for Gen X. They rely on them not for everyday transactions, but for navigating complex, high-stakes decisions such as retirement planning, funding education, and managing multigenerational financial responsibilities.

Millennials: the digital adopters

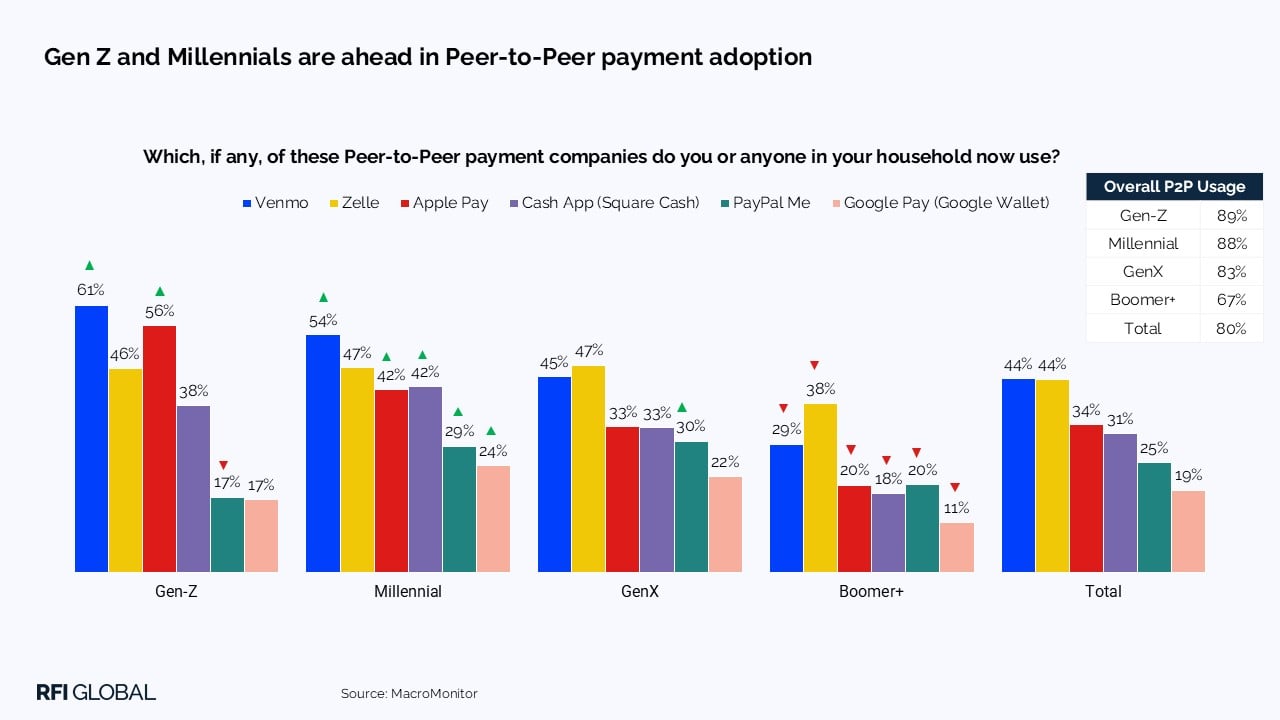

Millennials are strong adopters of digital banking. Our data shows that 48% are aware of Peer-to-Peer payments (P2P payments), compared with 42% of Gen X and 33% of Boomers, underscoring their comfort with mobile tools. This familiarity translates into usage: nearly half of Millennials (42%) use Apple Pay and more than half (54%) use Venmo, significantly higher than Gen X (33% Apple Pay, 45% Venmo) and Boomers (20% Apple Pay, 29% Venmo).

Yet when it comes to advice, Millennials prefer the human element. Only 10% reported getting financial advice online, while 39% cited in-person interaction with their primary financial advisor in the past two years. This contrast shows why branches remain valuable: they provide reassurance and education during milestones such as buying a home, first-time investing, or starting a business.

Banks are adapting accordingly. JP Morgan Chase has piloted ’community branches’ that host financial literacy workshops and provide advisory services. These models reflect how branches can evolve into empowerment hubs rather than transaction centers.

Gen Z: the confidence seekers

Gen Z use apps for everyday banking with MacroMonitor showing 55% make deposits via apps, 52% use them for transfers, 25% open or close accounts, and 31% even obtain credit cards.

But when financial stakes rise, digital isn’t enough. Only 9% obtained investment advice online in the past two years, while 25% interacted with their primary financial advisor in person. This shows that despite their digital comfort, Gen Z still turns to branches for trust, confidence, and legitimacy in milestones like opening their first accounts, applying for loans, or beginning to invest.

As Steve Weston, Head of Everyday Money Management at Barclays, explained on the Banking Uncovered podcast, “in-person advice is especially important for this generation during formative financial moments. For Gen Z, branches are about building confidence and legitimacy, not routine transactions”.

The implications for banks

Generational differences make it clear: branches must evolve from transaction centers into advisory hubs. Younger cohorts don’t need branches for deposits or bill payments; they want guidance, coaching, and milestone support. To capture this opportunity, banks should:

1. Reposition as advisory hubs: Staff should act as financial coaches, not just service reps.

2. Blend digital and human: Customers might start a mortgage application online but want to finish it in-branch with an advisor.

3. Create milestone-driven experiences: Host first homebuyer seminars, credit coaching, and investing workshops for Millennials and Gen Z.

4. Signal trust and legitimacy: Branch design and service must reinforce credibility and comfort.

Case in point: Capital One Cafe

Capital One Café’s hybrid spaces double as ’third places’ to work, meet, and relax while also offering banking. Instead of tellers, Café Ambassadors support accounts, while Money & Life Mentors help customers set financial goals. With craft coffee and a welcoming environment, these cafés merge lifestyle and finance, appealing directly to younger cohorts.

As Jim Marous, Host of Banking Transformed Podcast, puts it:

“Rather than viewing [branches] as legacy liabilities, forward-thinking institutions are reimagining them as differentiation points in an increasingly digital-first competitive landscape.”

The future of bank branches

Branches remain relevant across generations, but their role is shifting. Boomers depend on them for complex financial advice around wealth transfer, Gen X for navigating challenges of their peak earning years, and Millennials and Gen Z for reassurance and guidance at key milestones.

The renewed investment in branches by major banks underscores their enduring value. For banks, the opportunity lies in adapting branch design, function, and experience to meet generational needs. Done well, branches can serve as powerful relationship anchors in a digital-first world.

Discover how generational insights from MacroMonitor, the largest survey of US households’ financial services, can shape your branch strategy—get in touch.

Tiffany Ng

Client Executive, North America

Tiffany Ng is a Client Executive at RFI Global, supporting financial institutions across North America.

View full profileFrequently asked questions about branches

Q: Why do bank branches still matter in the digital age?

A: Despite widespread digital adoption, over half of US households still visit a branch. Branches remain essential for building trust, accessing financial advice, and making complex decisions that customers prefer to handle in person.

Q: How do different generations use bank branches?

A: Boomers value personal relationships and advice for estate planning, while Gen X seeks guidance for complex financial decisions. Millennials and Gen Z, though highly digital, visit branches for reassurance and confidence during major milestones, such as buying a home or starting to invest.

Q: Are younger generations abandoning bank branches?

A: No. Millennials and Gen Z continue to use branches strategically. While they rely on apps for daily banking, they prefer in-person advice for high-stakes financial moments, highlighting that trust and human interaction remain key.

Q: What should banks do to keep branches relevant?

A: Banks should evolve their branches into advisory hubs that blend digital convenience with human expertise, offering financial coaching, milestone-driven workshops, and experiences that build credibility and foster long-term relationships across generations.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.