Jackie Greig, VP Marketing, Global

Born between 1996 and 2010, Gen Z is estimated to have a global spending power of $450 billion, with many just entering their peak earning and spending years. For banks and financial institutions, this generation is not only the next wave of customers but also a powerful force reshaping financial services.

What do Gen Z expect from financial providers?

At the time of writing, Gen Z is between 15 and 29 years old. In this article, we focus on those aged 18–29, drawing on RFI Global data from six key markets, the UK, US, Australia, Singapore, Malaysia and Hong Kong, to uncover how this generation approaches money, banking and financial decision-making.

Our findings reveal striking regional contrasts. Despite being the first mobile-native generation, Gen Z’s financial behaviours defy simple assumptions. Mobile wallets are central, yet debit cards remain dominant in the US, and cash is still used by around two-thirds in the UK and Hong Kong. BNPL is much more widely used in Australia than in any other market. Branches continue to play a meaningful role, while social media is emerging as a key gateway for financial research. Gen Z also shows a greater willingness than older generations to switch banks in search of better rewards, rates or digital experiences.

As their influence grows, understanding Gen Z’s behaviour and attitudes, how they bank, pay, discover and switch, is critical to building relevance, trust and long-term growth.

1. Beyond digital: why branches still matter to Gen Z

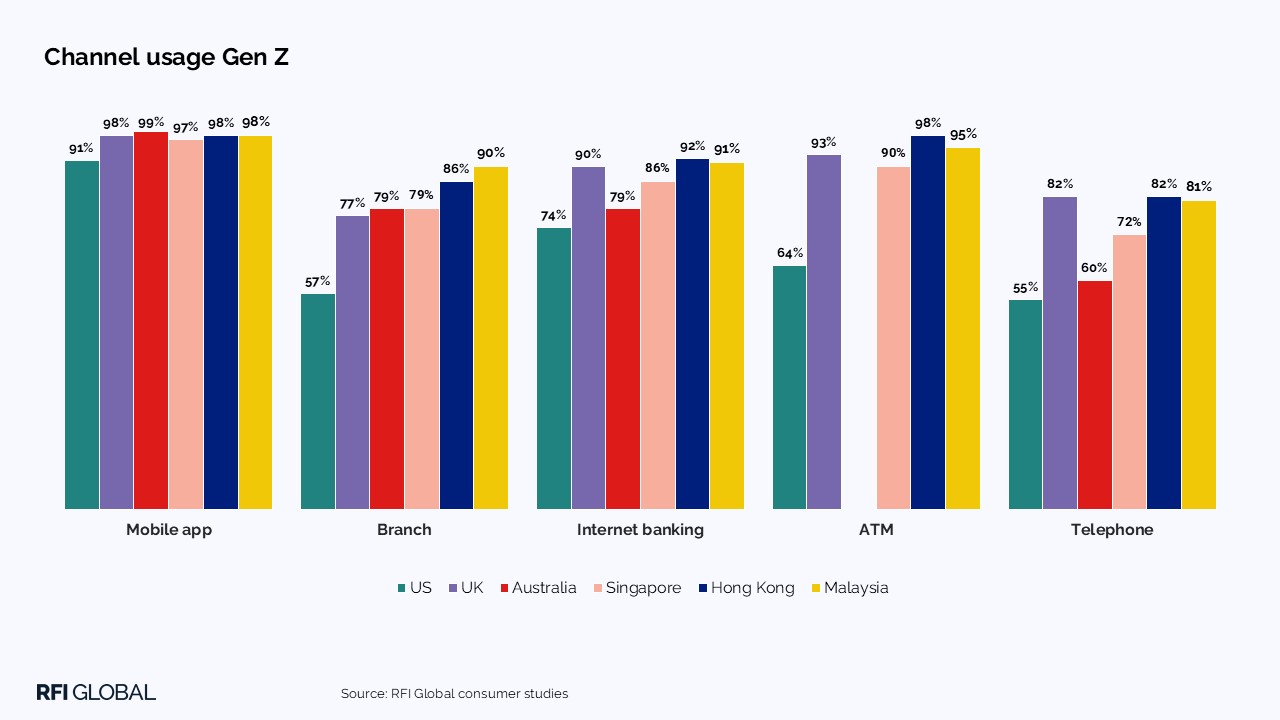

Gen Z is often described as a mobile-first generation, and our data confirms that. Mobile app usage is almost universal across markets, reaching 99% in Australia, 98% in the UK and Malaysia, with the US slightly behind at 91%. But the picture is more complex than a purely digital story.

Branches remain surprisingly relevant. In fact, in most markets outside the US, branch usage among Gen Z mirrors that of the wider population, suggesting the need for in-person advice and guidance for this segment. As Steve Weston, Head of Everyday Money Management at Barclays, explained in our Banking Uncovered podcast:

“Gen Z are the heaviest users of branches in the UK – 42% use them monthly, higher than any other demographic.”

ATMs are also important for this cohort, even as cash declines across markets. And while telephone banking sits further down the channel mix, adoption is still significant in the UK, Hong Kong and Malaysia.

Implications

Gen Z wants choice. Mobile-first design and UX are essential, but not sufficient. Financial institutions must deliver hybrid experiences that balance digital convenience with physical access and provide in-person advice as they grow financially, especially in markets where branch networks continue to play a critical role.

2. Tap, swipe, split: Gen Z’s evolving payment preferences

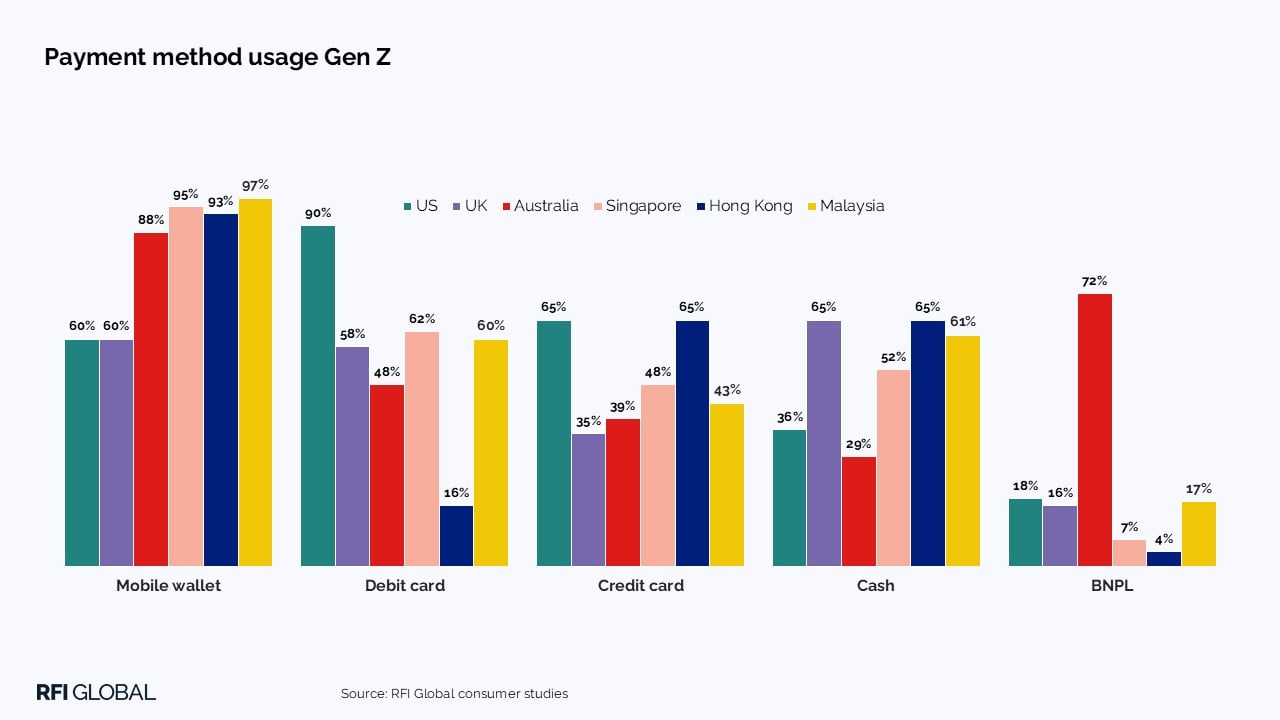

The global payments landscape is fragmenting, and Gen Z diverges from the wider population. Mobile wallets are now central to everyday spend, particularly in Asia, with adoption among Gen Z near universal in Malaysia (97%), Singapore (95%) and Hong Kong (93%).

Debit cards remain important, but usage varies. In the US a huge 90% of Gen Z use debit cards – the same proportion as the total population. Gen Z in the UK (58% vs 70% population) and Australia (48% vs 54% vs population) are more likely to use debit cards, whereas usage is lower in Singapore (62% vs 41%) and Malaysia (60% vs 55%). Hong Kong trails (16% vs 27%).

Credit cards are under pressure. Usage is lower among Gen Z than the total population in most markets, except for Hong Kong, showing more caution over debt. Two-thirds of Gen Z still use credit cards in the US and Hong Kong, but usage is much lower in other markets.

Cash usage varies sharply. The UK and Hong Kong are the most cash-dominant markets, with 65% of Gen Z still using it. Cash is also significant in Malaysia (61%), while only around a third of Gen Z in Australia (29%) and the US (36%) use cash.

Alternative payments are gaining ground. Buy Now Pay Later (BNPL) is particularly strong in Australia (72% of Gen Z vs 28% for total population) and shows modest increases in Malaysia (17% vs 13%) and Singapore (7% vs 4%), while adoption is lower among Gen Z in the US (18% vs 27%) and stable in the UK (16%) and Hong Kong (4%).

Implications

Mobile is foundational. Financial institutions must prioritise app performance, security and personalisation to stay competitive. Mobile-first payments are now table stakes, while BNPL drives engagement in Australia and parts of Asia, and cash remains critical in the UK and select markets. To win with Gen Z, banks must offer payment options that meet both digital expectations and market-specific habits.

3. The social signal: Gen Z’s financial decisions start on social media

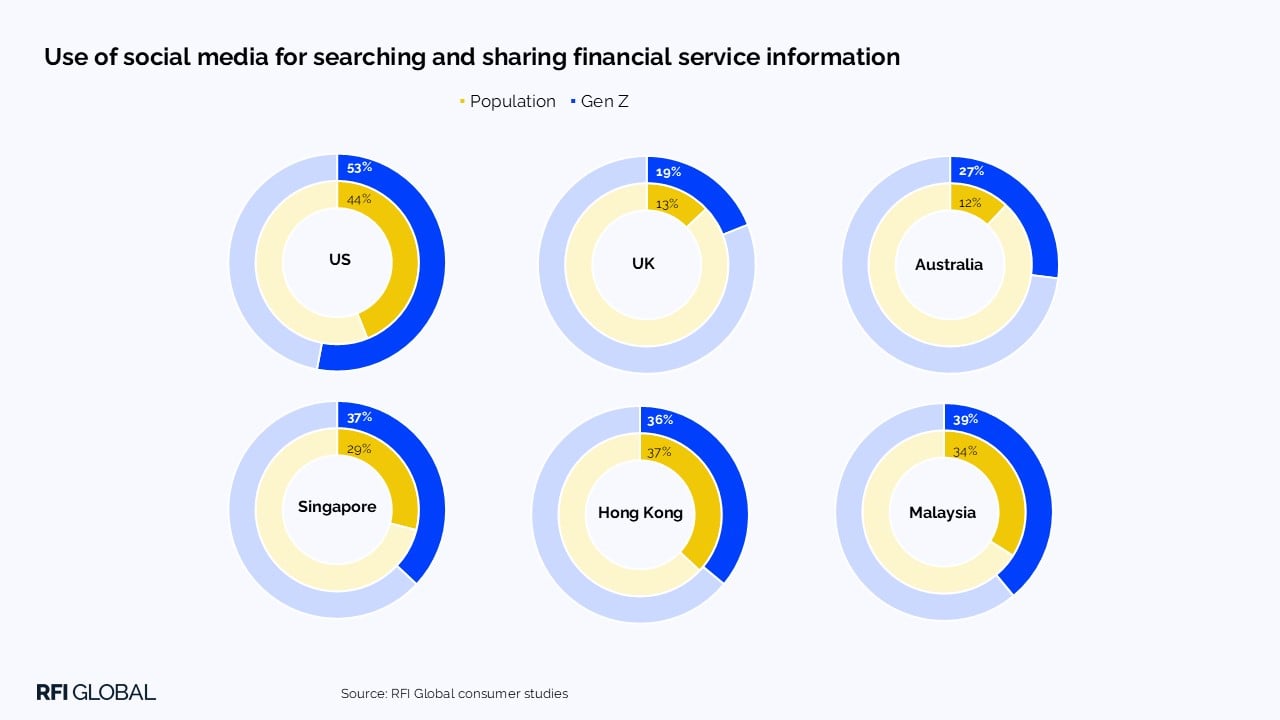

Social media plays a much bigger role in financial decision-making for Gen Z than for the wider population in all markets except Hong Kong. The US leads, with more than half of Gen Z (53%) using social platforms to research financial providers. Malaysia also shows high engagement (39%). Gen Z in the UK are less likely to use social for financial information at just 19%.

In the US, Gen Z gravitates towards platforms that blend peer voices with accessible content. YouTube (20%), Reddit (18%) and TikTok (18%) are the leading sources of financial information, but Facebook (17%) and Instagram (16%) are also influential. By contrast, professional or niche platforms see limited traction, LinkedIn (6%), X (7%), Snapchat (6%), WhatsApp (2%) and Pinterest (1%).

Implications

Social media is no longer just a marketing channel but a strategic space for discovery, education and trust-building. To win Gen Z, providers must meet them where they are, on the platforms they trust, in the formats they prefer, while tailoring strategies to local market norms. Those who engage authentically will gain an edge with a generation reshaping financial services.

4. Loyalty on the line: What drives Gen Z to switch financial providers

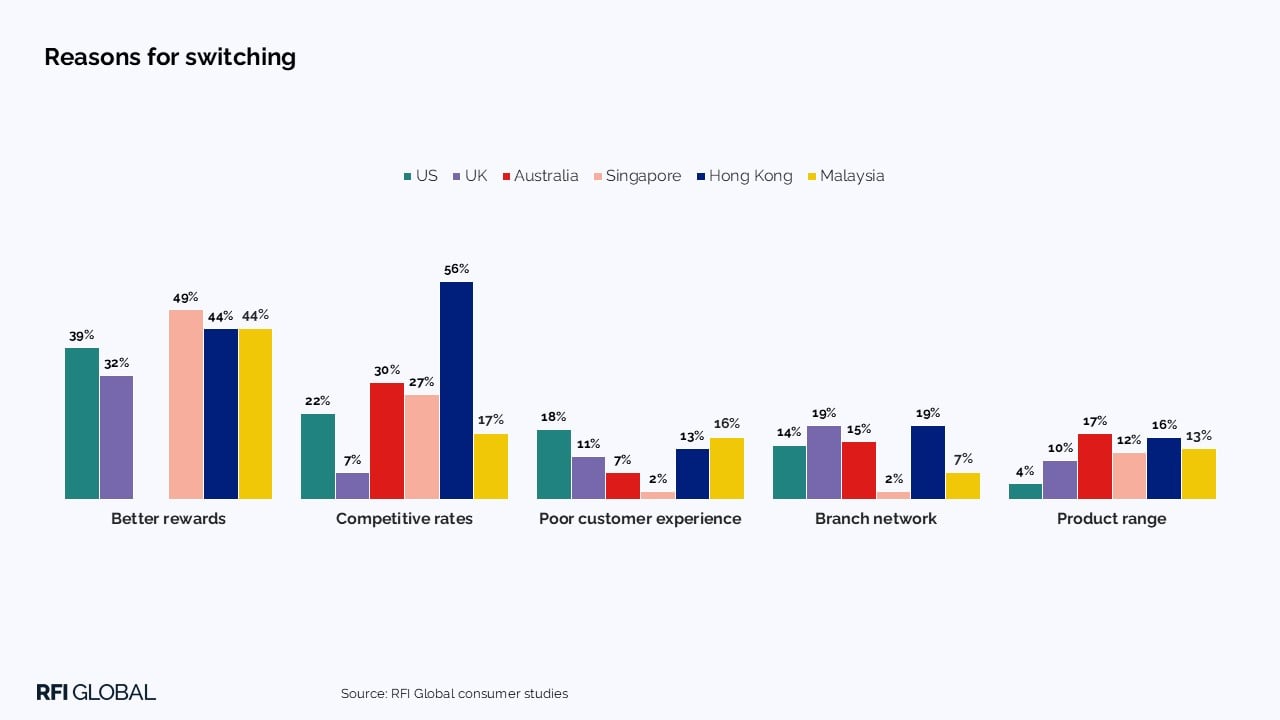

Gen Z is more likely than older generations to reconsider their banking relationships when their expectations aren’t met. Across markets, switching intent among Gen Z is consistently higher than the population average, except for Hong Kong. The US (32%), Singapore (20%) and Malaysia (19%) show the strongest appetite for change. By comparison, older cohorts like Boomers have a much lower intention to switch providers.

The reasons for switching highlight pragmatism and high expectations. Rewards are the strongest motivator: close to half of Gen Z in Singapore and Malaysia and nearly four in ten in the US say they would switch for better loyalty benefits.

Competitive interest rates, of course, are another powerful driver, especially in Hong Kong (56%) and Australia (30%). Customer experience also matters for Gen Z, particularly in the US and in Malaysia, citing poor service as a reason to leave. In some markets, branch access and product range still influence decisions, particularly in the UK and Hong Kong.

Implications

Gen Z expects seamless digital experiences, responsive service and personalised rewards. Institutions that fail to deliver risk higher churn, while those that invest in loyalty, innovation and customer care will build lasting relationships with this critical generation.

The next generation opportunity

Gen Z is already reshaping financial services, and their influence will continue to grow. For providers, the challenge is not just keeping up with digital expectations, but understanding the nuances of how this generation bank, pay, researches and switches across different markets.

We have a depth of insight on this important generation in our surveys, so please do get in touch if you’d like further insights.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileFrequently Asked Questions

Q: How is Gen Z reshaping financial services globally?

A: Gen Z is driving a shift toward digital-first experiences, with mobile wallets, social media research and higher willingness to switch providers reshaping banking behaviours across markets.

Q: Which financial channels and payment methods does Gen Z prefer?

A: Mobile wallets dominate in Asia, while debit cards and cash remain significant in the UK, Hong Kong and Malaysia. Branches continue to play a role in certain markets, and BNPL is increasingly popular in Australia and parts of Asia.

Q: How does Gen Z research and switch financial providers?

A: Gen Z frequently uses social media, particularly in the US and Malaysia to discover and evaluate providers. They are pragmatic and willing to switch banks for better rewards, competitive rates, or superior customer experiences.ise further in the coming years.

Q: What should banks do to engage and retain Gen Z customers?

A: Banks must offer hybrid, mobile-first experiences, optimise app performance and security, provide personalised rewards and tailor payment options to local market preferences to build trust and loyalty.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.