Edward Smith, Lead Analyst, North America & EMEA

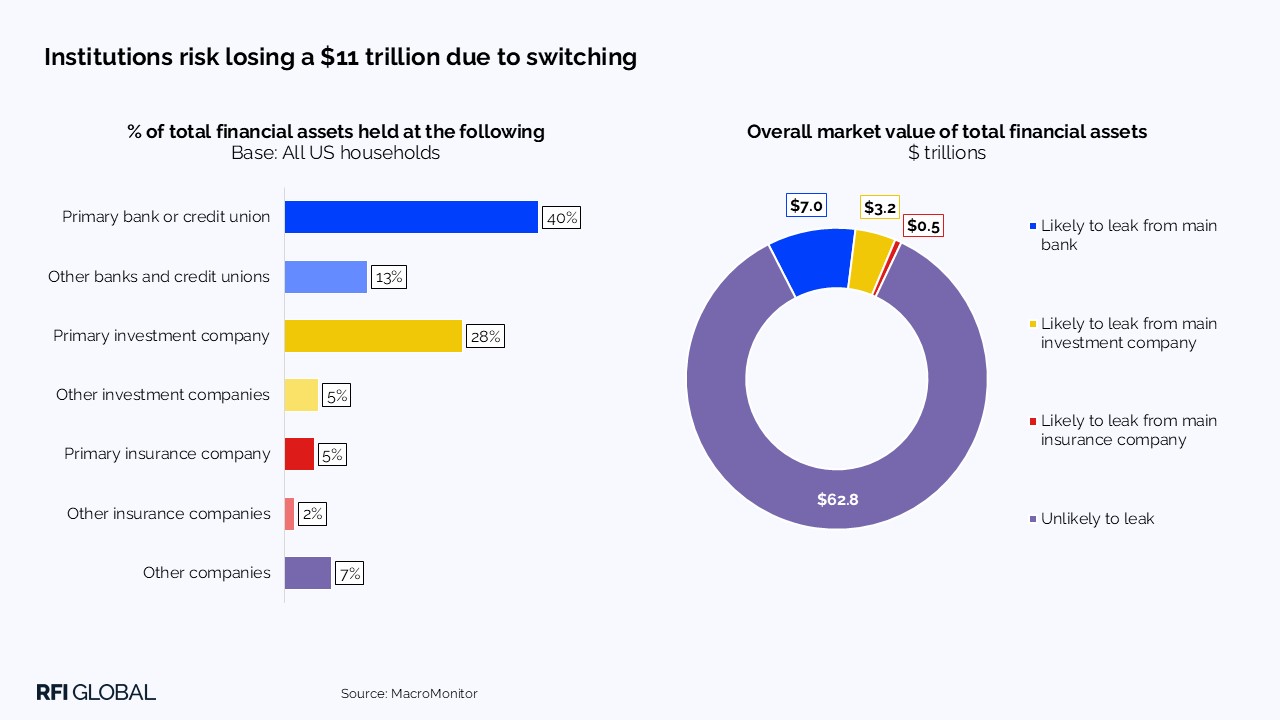

Intentions to switch bank and investment providers in the US have reached a 10-year high, with 1 in 4 households now considering changing their main provider. Together, primary banking, investment, and insurance relationships account for 73% of the average household’s assets, putting around $11 trillion, 15% of all financial assets, at risk of being redistributed due to switching.

Plugging this leakage should be central to institutions’ acquisition strategies. Using data from MacroMonitor, the largest study of US household financial behaviors, we uncover the trends and attitudes driving customers to seek new products beyond their primary relationships, and more crucially, to understand what pushes customers to transfer their primary relationship to rival institutions.

Drivers of switching: Push and pull

Two broad factors fuel a household’s decision to switch its primary bank:

1: Pull factors. Demand for better rewards, more competitive rates and incentives are the most common reasons for switching. While less loyal customers are more likely to move between brands to chase immediate benefits, this behavior has accelerated with the growing disparity between standard deposits and the digital-only, high-yield offerings. Comparisons are unavoidable, and banks need to provide more than just a viable alternative to quash switching intentions.

2: Push factors. A notable cohort of switchers have poor experiences with their banks, reflected in their lower advocacy scores (with an NPS of -44, vs +35 among non-switchers). Some pain points are disproportionately impactful, though, as limited access to relevant products, wealth services, and branches correlate most strongly with low satisfaction. Failure to communicate appropriate cross-sell opportunities is the catalyst that can turn an otherwise engaged customer relationship into attrition.

While incentives are the most common drivers, switching due to poor product and service access is more indicative of a relationship at risk of being lost entirely.

Who is most vulnerable to switching?

Low tenure relationships—those under 5 years for banks and 3 years for wealth providers—are at most risk, stressing the value of high-rate options and an effective onboarding process.

Younger Gen Z and Millennial households are highly susceptible to switching, mostly as digital platforms make opening new accounts easier and social media allows these customers to be savvier about financial solutions.

High-net-worth households are more open to switching, primarily as switching incentives can be tailored to their needs.

Customers of traditional providers tend to be more vocal about switching than those using neobanks. As emerging technologies and AI-powered services become more entrenched, the power of being a frontrunner in innovative financial services will only grow.

The need for financial simplification

Rising switching is strongly linked with a heightened demand among households for consolidation. Interest in consolidation has been widespread for over a decade in the US, as most households (82%) prefer to use a single provider to meet most of their needs. This sentiment is now beginning to translate into activity, as more US households are considering eliminating some relationships to make financial management easier, up from 23% in 2020 to 31% in 2024. Appetite for reducing relationships among switchers is far greater at around 2 in 5, emphasizing their need to streamline their finances.

Why simplification?

As many households look beyond existing relationships for better deals, product holdings are fragmenting. In 2018, 48% of households were actively shopping around for financial services. This figure is now 64%. Product uptake has seen the largest shift, as the percentage of savers using secondary providers increased from 24% to 39% across the same period. Product leakage to secondary providers is one of the key precursors to switching; likely switchers hold 48% of their products outside their main bank, vs 42% among those unlikely to switch.

Competitive acquisition should emphasize how the brand can help customers streamline their products in order to better leverage the services most applicable to their needs.

Crafting the digital edge

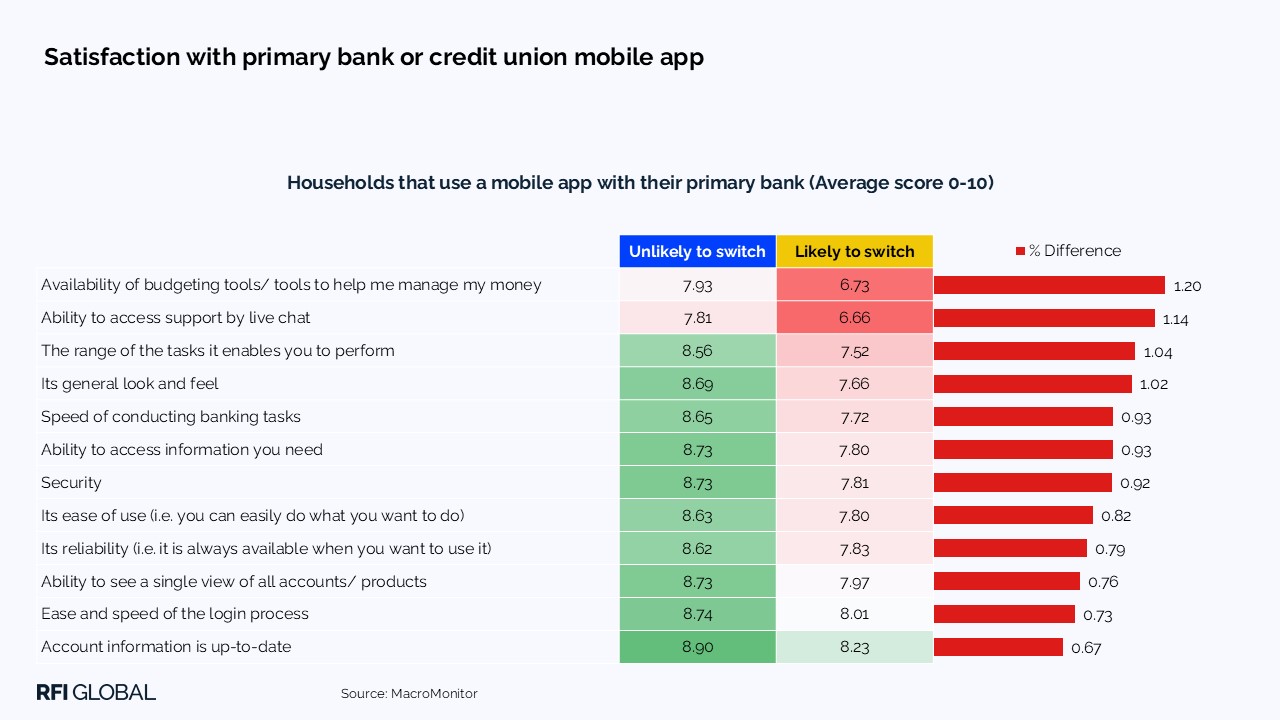

Digital platforms are the means to action this strategy. Our data shows that switchers are more likely to rely on mobile channels, and that the significance of mobile banking on a household’s choice of provider has increased steadily over the last decade. Despite their greater dependence on mobile, switchers are often less satisfied with their overall mobile experiences, principally due to limited functionality. Mobile apps are essential for making a good first impression and ensuring customer engagement, so focusing on their development should be a top priority.

Reinventing the mobile app as a unique selling point should be the first step. Budgeting tools such as savings pots and spending categorization are in demand for switchers, which could facilitate more advanced personal financial management technologies with further investment. Better provision of live chat support, like elevating the service to provide AI-powered advice, would also be a unique value add-on. Users should feel empowered by these tools, equipped to make informed decisions in a way that no other service provider can. Associating the brand with this sense of greater personal control should be the goal for mobile app development.

How to bottle the Genie: The key takeaways

In an environment where the retention is harder to achieve than ever before, financial providers need to keep the following in mind:

1. Switching momentum is growing.

Drivers of switching are becoming more significant. Cross-sell opportunities need to be identified and capitalized on quickly to funnel growth in the customer relationship.

2. Reasons for switching.

Rewards and incentives are the main drivers for switching indicative of customers moving between brands in search of short-term benefits. Switching due to poor access to premium products, by contrast, reflects the loss of a strong growth opportunity due to poor service communication

3. Switching segments.

Younger, more affluent cohorts traditionally open to switching are more likely to act on their intentions as the barrier to entry is much lower via digital platforms.

4. Simplification means decisions.

With the renewed focus on financial simplification, households must choose which provider to prioritize. If their relationship with their main provider is already weak, it’s much more likely that they will transition to another institution.

5. Active innovation.

Providers should create innovative solutions like interactive learning tools, financial management aids, and AI-powered support features. These reward customers who hold most of their assets with their main provider, offering valuable insights unavailable from market competitors.

Get in touch for more insights on switching behavior, consolidation trends, and customer expectations from our survey. We have more insights available for your institution and your competitors. See how you measure up and where the opportunities lie.

Edward Smith

Lead Analyst, North America & EMEA

Edward Smith is a Lead Analyst at RFI Global, covering financial services trends across North America and EMEA.

View full profileFrequently Asked Questions

Q: Why are more Americans switching banks in 2025?

A: US consumers are increasingly switching due to poor service, lack of relevant products, and the growing appeal of high-yield, digital-only banking alternatives. Demand for simpler financial management and better mobile tools are also key motivators.

Q: Who is most likely to switch banks or investment providers in the US?

A: Gen Z, Millennials, high-net-worth households, and customers with newer banking relationships are the most likely to switch—especially those using traditional providers, who are more vocal about leaving compared to neobank customers.

Q: How is digital banking influencing customer loyalty?

A: Mobile banking is critical to customer retention. While switchers are more dependent on this channel for engagement, many are dissatisfied with the current app functionality. Features like budgeting tools and AI-powered support can turn digital platforms into loyalty drivers.

Q: What can banks do to reduce switching and improve retention?

A: Instead of focusing solely on rates, institutions should offer personalized financial tools, proactive cross-sell strategies, and seamless digital experiences to encourage consolidation and build long-term loyalty.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.