Edward Smith, Lead Analyst, North America & EMEA

Coming into 2025, many leading US banks and economic commentators expected interest rates to be chopped – a safe prediction as rates were trending downwards from an August peak of 5.33% to 4.48% in December. Instead, cuts were less substantial than anticipated, holding at 4.33% since January. Recent reports from the FED indicate that rates will hold until inflation is quashed. The tariff turmoil throws more uncertainty into the mix.

The consumer perspective

Understanding how US consumers intend to navigate this situation is essential for financial institutions, as these challenges will prompt customers to reorganise their holdings and re-evaluate their relationships.

Our Financial Services Trends and Predictions 2025 report highlights market volatility as one of five key trends shaping the future of financial services globally this year. We identified three global undercurrents influencing consumer decision-making:

1. Consumers are becoming increasingly sensitive to macroeconomic pressures, namely inflation. General sentiment emphasizes saving more, spending less, and borrowing less.

2. Savers are more willing to shop around and are more likely to hold a secondary savings account. Liquidity and product flexibility have greater value, which poses a churn risk.

3. There is a significantly higher chance of households refinancing as they struggle to manage debt. Customer retention will be far more difficult for lenders.

What does this mean for US financial institutions?

US households are leveraging the high-rate environment to safeguard their regular income and simplify their debt burdens. This presents unique acquisition opportunities through high-yield, fixed-term products. Most importantly, even when rates drop, customers are likely to retain high expectations of what a competitive offering includes.

With new data from MacroMonitor, the largest survey of US households’ financial behavior, we revisit the volatility trend to further explore consumer savings and lending in the US, and highlight how providers can capitalize on these dynamics.

Shifting household concerns and priorities

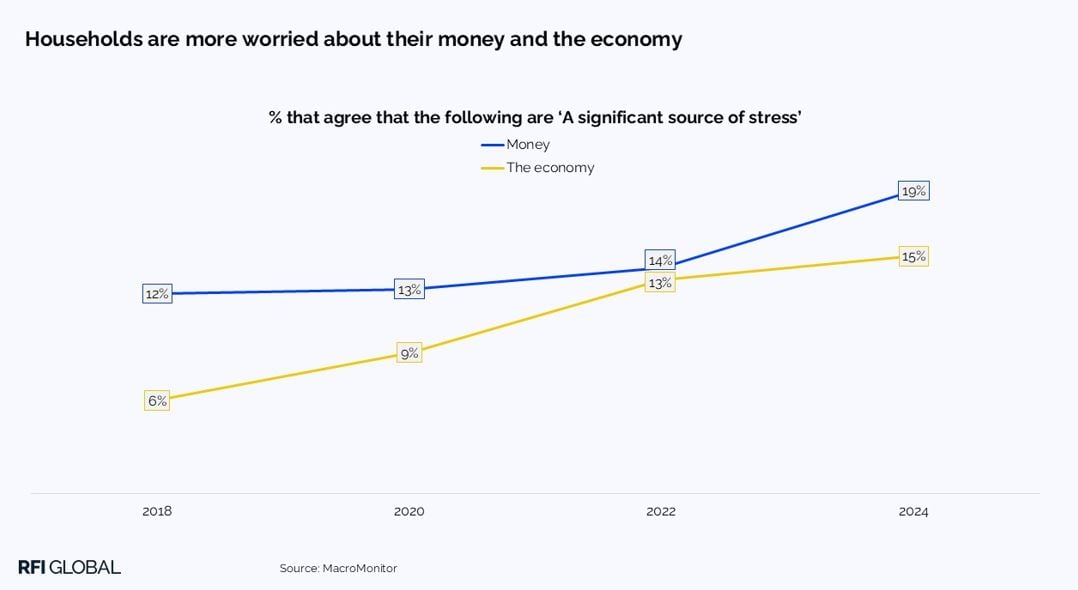

Even before the explosive tariff announcements, it was difficult to avoid news about the precarious state of the US economy. Ballooning national debt, declining spending power and rampant inflation all weighed heavily on US consumers. Our data quantifies this change: In 2018, only 6% of households reported that the economy was a significant source of stress, and 12% were equally concerned about their personal finances. At the end of 2024, these figures rose to 15% and 19% respectively.

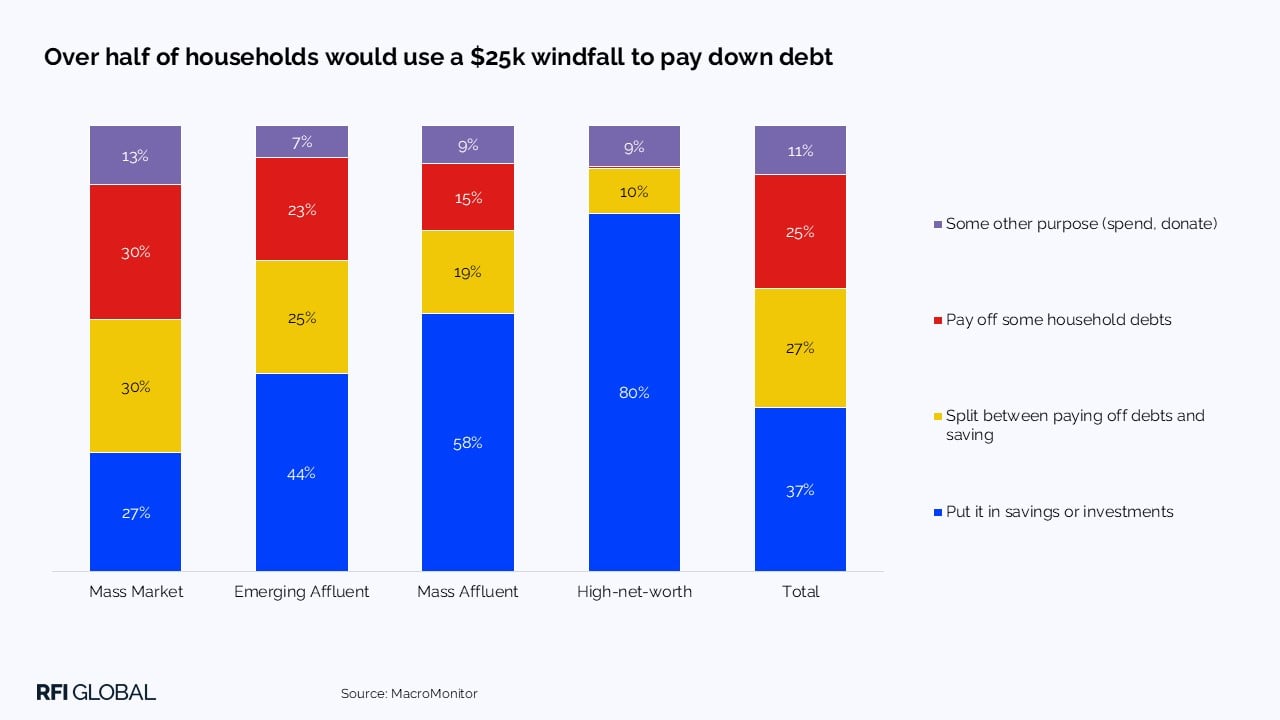

Sentiment towards saving and lending reflects these growing concerns. When asked what the household would do with an unexpected windfall of $25k, 37% prioritized investing the majority into savings, whereas 25% would use it to pay off outstanding debts. A further quarter would split the funds between these two tasks. Savings and lending solutions are going to become front-of-mind considerations for households feeling the squeeze on their finances.

Debt repayment tops the household priority list

The growing appetite for debt consolidation is a consequence of this shift. Around 2 in 5 households identify debt consolidation as a top priority, and 9% intend to take up a loan for this purpose in 2025 – up from 4% in 2019. Demand for simplified debt management speaks not only to households struggling to balance their budget, but also to the want for streamlined management. While lenders can directly benefit from promoting this product offering, financial providers should more broadly consider how they can help customers better visualise their in-goings and out-goings if they want to strengthen engagement.

What’s driving interest in savings products?

Our data shows that, before 2024, most households used a savings provider to access deposit protection via government insurance. Households now prioritize a guaranteed rate of return, in support of sustaining a consistent income. Liquidity and potential for large, short-term gains have also become more central. Combined, this reveals a far more engaged customer base of savers, and their need for more frequent interaction could be justification for integrating more savings tools and advisory services into engagement channels.

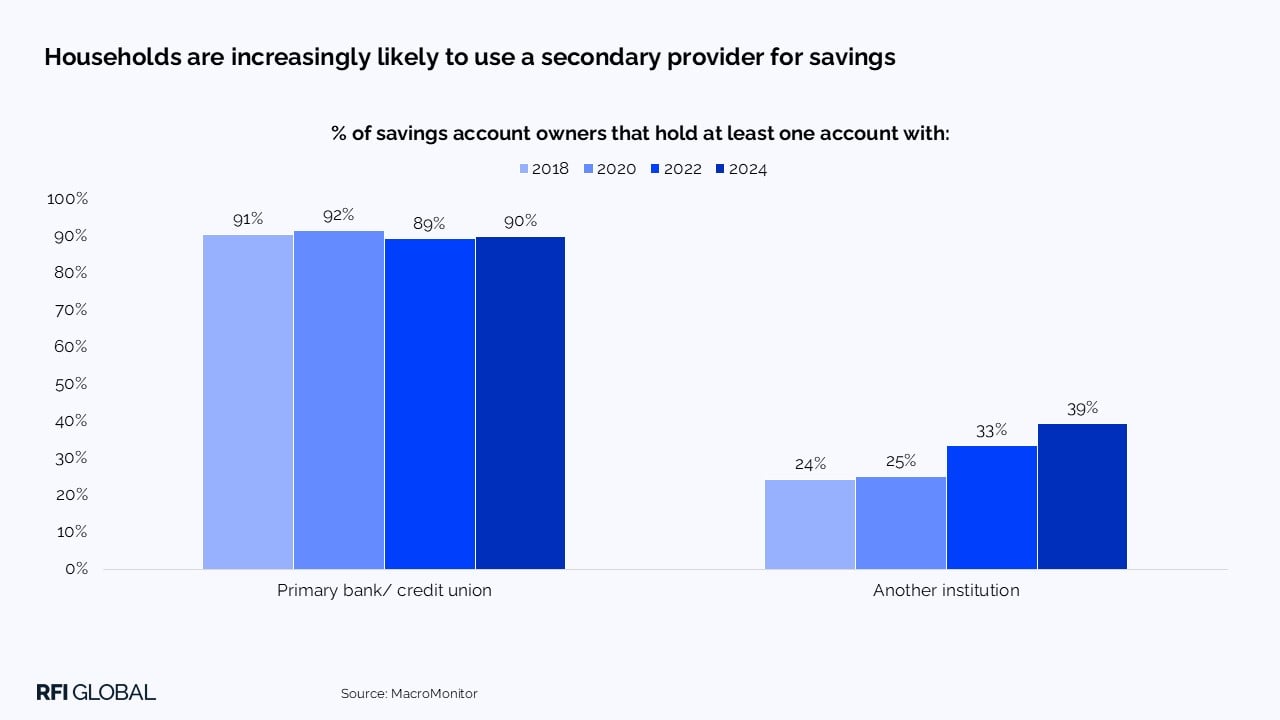

The immediate implication for banks and savings providers is the greater risk of attrition. With the heightened demand for instant gratification, new account rate incentives are a stronger motivator for switching. Twelve percent of US households claimed that interest rates were the top driver of choice for their primary deposit provider at the end of 2024, up from 8% in 2022. Even when the main account status is not at risk, uptake trends still threaten to weaken the primary relationship. In line with our previous predictions, the number of savings account holders using a secondary provider has increased consistently up to 2025, with 2 in 5 savings owners using a provider other than their main bank for their savings needs.

Unless providers are willing and able to continually compete for the top market product, they need unique service features to prevent savings balances from leaking from the core bank relationship.

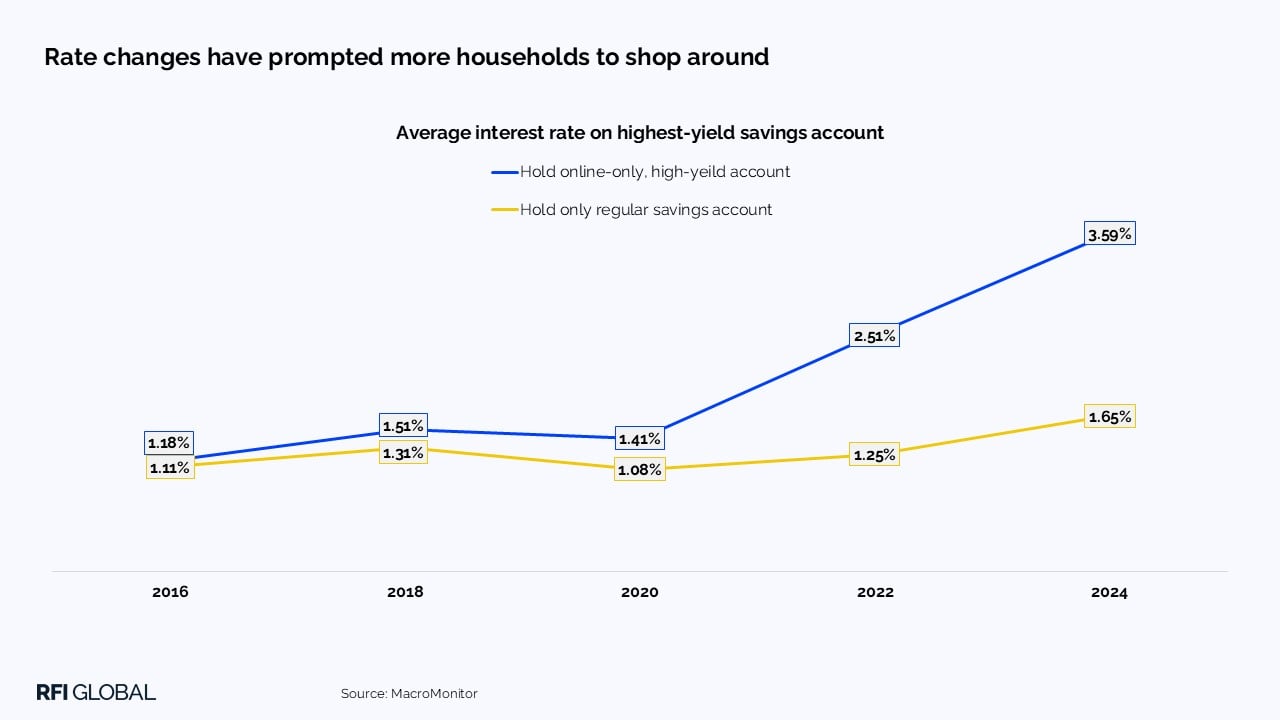

The rate race

Two in five households claim that changes in interest rates influenced their choice of savings product in 2024, a significantly higher number than prior years. This sentiment is reflected in the mass adoption of online-only accounts; 9% held one in 2018, and the figure has nearly doubled to 17% in 2024. Moreover, recent uptake coincides with the divergence of product rates. Most high-yield offerings were on par with regular accounts prior to 2020, but now consumers have access to rates double that of standard provisions. While this has benefited acquisition in the short term, the expectation that high-yield accounts should remain this competitive will likely stick.

Affluent households turn to CDs amid rate uncertainty

Although rate-chasing is usually indicative of less loyal customers, the recent mass adoption of Certified Deposits (CDs) shows another side of the story. 2023-2024 saw the largest increase in CD ownership for the last decade, up from 11% in 2022 to 15% in 2024. Uptake has been mostly from affluent cohorts.

The average CD is around four times the value of a typical regular savings account deposit ($82k vs $22k) and slightly more than the holdings of high-yield account holders ($62k). In the overall market, about 12% of funds held in savings accounts in 2022 have been reallocated to CDs in 2024. Many may have opted in due to expectations that interest rates would decline, yet nonetheless the willingness of affluent consumers to lock their savings into less liquid products presents a strategy opportunity for providers wishing to avoid perpetual competition.

Implications for the savings and investment market

Given the curveball of federal rates plateauing, the high-rate environment will persist to have a significant influence over consumers’ saving and lending relationships.

Financial products have entered a new, ever more competitive phase, and the way customers take advantage of these offerings represents a fundamental change in their engagement with saving and borrowing. They are actively shopping around for high-return solutions and are more willing to go outside their main bank relationship to acquire these offers.

Digital-only, high-return accounts are facilitating a greater degree of rate chasing, but potential customer turnover could be mitigated by CDs and savings tools that help customers better evaluate their savings goals. Similar advice applies to lenders, who should prioritise debt consolidation products and equivalent services that emphasise clarity and ease of use.

What next?

Want to find out more about how US consumers are responding to today’s financial landscape? MacroMonitor offers rich, actionable insights into household financial behavior—helping you to stay ahead of the evolving consumer landscape and build propositions that truly resonate.

Edward Smith

Lead Analyst, North America & EMEA

Edward Smith is a Lead Analyst at RFI Global, covering financial services trends across North America and EMEA.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.