Luke Allchin, Director, North America

In November, RFI Global published the Financial Services Trends and Predictions report, an analysis of our extensive global data exploring pivotal changes set to shape the industry in 2025. I had the pleasure of working on this report with my fellow financial services experts worldwide. We focused on the challenges the sector faced in 2024, shifting consumer sentiment, the year that lies ahead and the implications for financial institutions.

But what does the future hold for financial services in the United States?

The financial services industry in the US saw dramatic change throughout 2024, driven by shifting economic conditions, technological advancements, and with it, evolving consumer expectations. As Americans grappled with high interest rates, inflation, and a volatile job market, their approach to banking and financial decision-making changed.

A growing preference for convenience, digital solutions, and value-driven products has reshaped how financial institutions interact with customers. Against this backdrop, the financial services landscape is poised for even greater shifts in 2025, and below, I delve into the trends we identified, share my data-driven predictions for 2025 and examine their implications for the US market.

1. Winning loyalty in a world of change: Customer retention in turbulent times

Switching intentions among US consumers have never been higher, with 1 in 4 households thinking about switching their primary banking relationship. As the US economy stabilizes and interest rates begin to decline, retaining customer loyalty will become a critical focus for financial institutions.

In recent years, loyalty programs – particularly those tied to credit cards – fell short of meeting consumer expectations (for example, 26% of US cardholders would consider switching credit card providers to access a better points program). Many long-term customers felt underappreciated, prompting them to seek alternatives that offered tangible rewards for their continued business.

The key to addressing this challenge lies in innovation. Banks must design loyalty programs that go beyond credit card incentives and appeal to a broader demographic, including younger Americans who favor debit cards and digital wallets. For example, initiatives like cashback rewards, personalized discounts, and gamified prize draws – like Australia’s CommBank Yello program – can drive engagement and satisfaction among US consumers.

Additionally, as Americans become more financially conscious, banks that position themselves as allies in smart money management will stand out. Rewarding behaviors such as saving, budgeting, and investing through integrated platforms will be key to strengthen customer relationships and retention in an increasingly competitive market. Data from our extensive MacroMonitor study of US household financial behavior not only shows that there is a growing number of US households struggling to keep up with their financial commitments, but also that many perceive budgeting as being more trouble than it is worth. This suggests many households could benefit from smart money management platforms and would see value in them.

2. The digital edge: Fintech, AI and the future of financial services

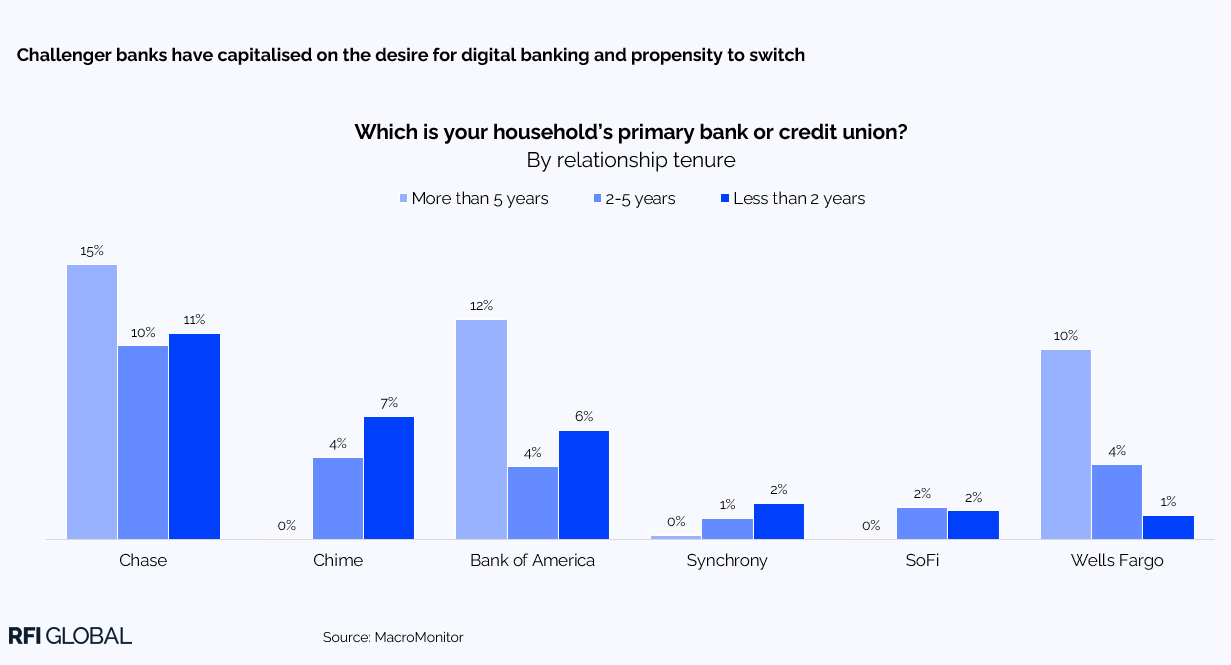

The digital revolution continues to redefine financial services in the US, with fintech firms leading the charge in offering innovative, user-friendly solutions. US consumers increasingly prefer digital banking over traditional in-person services, valuing speed and convenience. Fintech challengers excel in this space, often providing streamlined interfaces, low fees, and instant support that resonate among the younger generations.

In the US, challenger banks have capitalized on the desire for digital banking and consumer propensity to switch. Collectively, Chime, Synchrony and SoFi account for 1 in 10 primary bank accounts opened in the last two years.

AI’s transformative potential will continue to play a pivotal role in the industry’s evolution. While consumer trust in front-end AI tools like robo-advisors is growing slowly in the US, back-end applications such as fraud detection and risk management have already demonstrated significant value in countries such as Canada. Data from RFI Global’s Consumer Banking, Payment & Innovation Council shows that 55% of Canadians feel comfortable with AI powering fraud detection and prevention, a higher proportion than all other applications AI could help facilitate within financial services. For US banks, leveraging AI to improve security and operational efficiency can help to build trust and loyalty among their customers.

Generative AI tools are also reshaping customer engagement. For instance, AI-driven chatbots and co-pilot technologies are enhancing customer service by delivering instant, accurate responses to queries. This is especially important as digital-first relationships dominate the banking landscape and will become ever more important in 2025 as a greater number of consumers seek assistance from their financial providers in light of the struggles they will inevitably face.

3. Navigating market volatility: The impact of rate shifts on consumer saving and borrowing

Interest rate movements remain a key driver of consumer behavior in the US financial services sector. With rates expected to decline in 2025, US consumers may prioritize flexibility in their financial products, seeking options that allow them to adapt quickly to changing conditions. This trend presents both opportunities and challenges for financial institutions.

On the savings front, lower rates will push banks to focus on value-added offerings to retain deposits. For instance, bundling savings products with transactional accounts or providing tools that help customers manage and grow their wealth can deepen relationships.

On the borrowing side, refinancing activity is likely to remain elevated as borrowers seek to take advantage of falling rates. Although, the rise of financial stress among borrowers shouldn’t be overlooked. With 25% of US households struggling to make ends meet, and many still grappling with repayment concerns, we will likely

continue to see lenders offering flexible loan structures throughout 2025, even if rates do begin to fall. As I mentioned earlier, robust support services will be essential for maintaining customer trust and satisfaction among borrowers in the coming year.

4. The wealth advantage: The rise of the emerging affluent

The Emerging Affluent is a segment that is growing in importance in the US. This group, characterized by growing wealth and a forward-looking approach to financial planning, is particularly interested in sustainable investments.

In 2025, to cater to this segment’s unique needs, we are likely to see US financial institutions double down on ESG (Environmental, Social, and Governance). Emerging Affluent households in the US are more interested in purchasing socially responsible investments than Mass Market and Mass Affluent households. They prefer investing in companies with a sound record of protecting the environment. ESG investments are likely to gain further traction, as the Emerging Affluent prioritize aligning their financial decisions with personal values.

To further capture the attention of the Emerging Affluent, financial institutions must provide tailored advice and cutting-edge digital tools. Robo-advisors, enhanced by AI, are well-suited to meet these preferences, offering data-driven insights at a fraction of the cost of traditional advisory services. Banks that integrate these solutions into their offerings would be well positioned to establish themselves as leaders in this rapidly growing segment.

The year ahead for financial services in the US

As we look toward 2025, the US financial services industry must navigate a complex landscape shaped by technological innovation, evolving customer expectations, and economic uncertainty. The themes of loyalty, digital transformation, market volatility, and demographic shifts will be a focal point in the year ahead.

What next?

The key to thriving in this dynamic environment lies in adaptability. Whether leveraging AI to enhance security and personalization, designing innovative loyalty programs, or addressing the unique needs of emerging demographics, the institutions that respond to these changes will be best positioned to win in 2025.

2025 will not just be a year of challenges, but a year of opportunities to redefine the banking experience and lay the foundations for the next generation of retail banking consumers in the United States of America.

Subscribe to get the latest RFI data and insights.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.