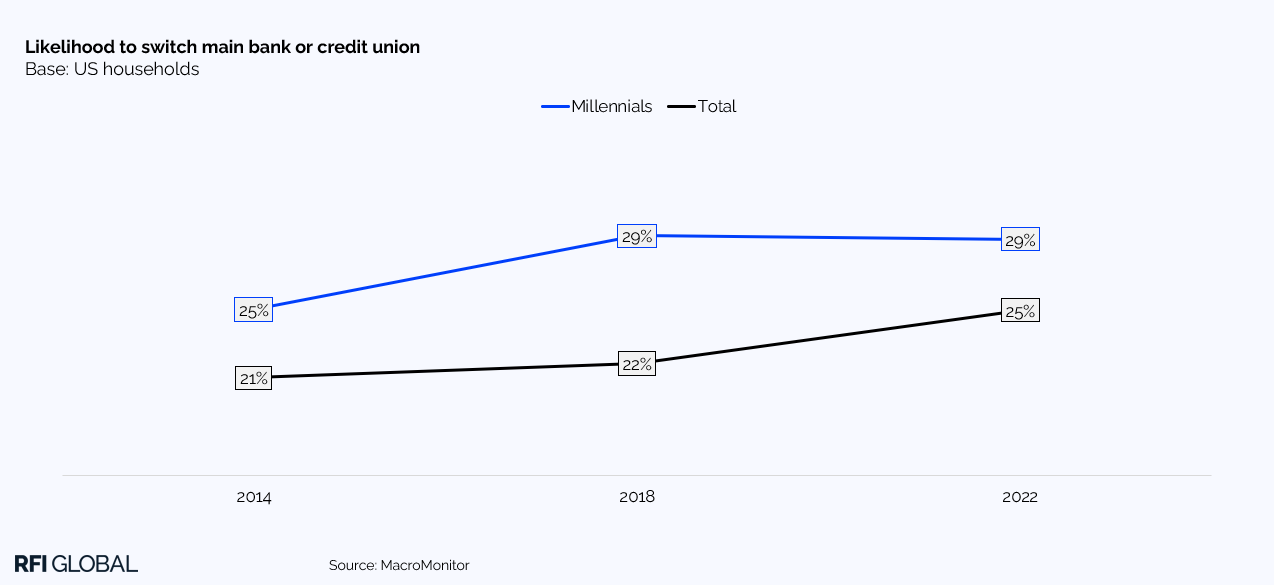

In 2024 fintechs have finally ‘arrived’. Monzo has 10 million accounts, Revolut has a banking license and the top 10 fintechs globally have more retail banking customers than the top 20 retail banks. At the same time, bank switching rates have hit historically high levels with all major markets seeing a significant increase. In the US in the last ten years according to RFI Global’s MacroMonitor data customer switching has jumped from 20% to 25% and among millennials that same stat has jumped to 30%.

The age of the fintech

So, as the age of the fintech dawns, what does this mean for the primary banking relationship that has historically been revered by bankers? As Jim Marous, global speaker and co-publisher of The Financial Brand, says in our Banking Uncovered podcast, people used to switch banks by opening one account and at the same time closing another. Today this has all changed. Customers now simply open another bank account without closing their previous one. This has implications for the primary banking relationship.

The implications for banks

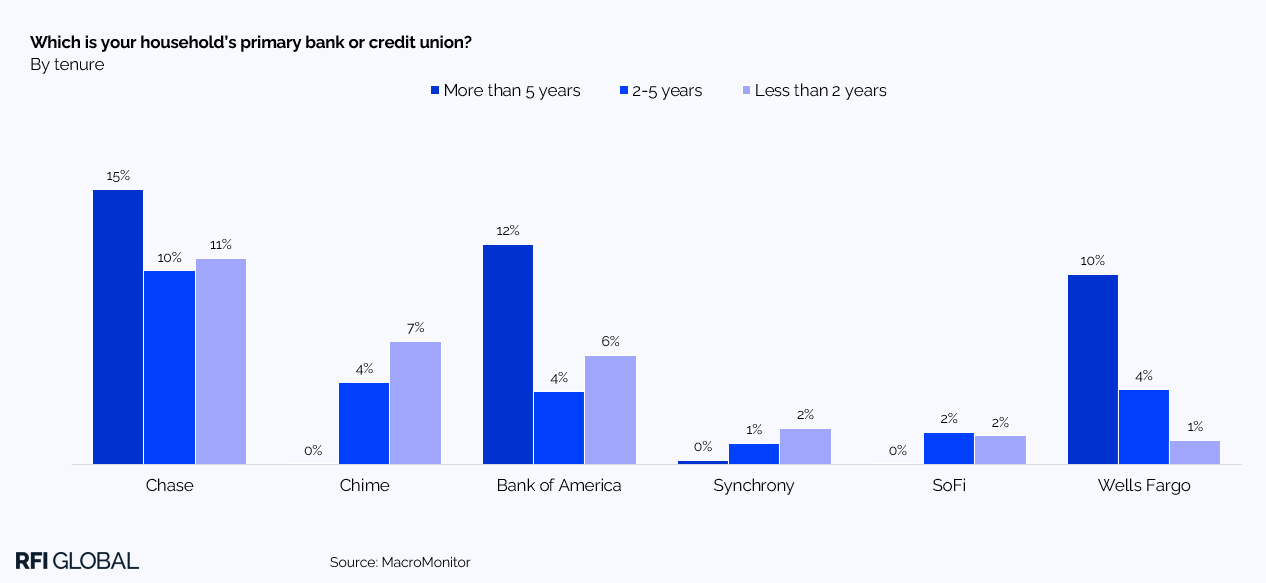

Banks now need to have a much greater understanding of which customers would actually consider them to be their primary financial relationship. According to RFI Global’s MacroMonitor data, in the US in the last two years, Chime has had more new primary account openings than Wells Fargo and Bank of America combined. On top of that, if you combine Chime with SoFi and Synchrony, they now account for more than 10% of primary banking relationships for the entire US market. As Jim says, “Traditional banks are becoming just warehouses for deposits”.

Creating a financial wellness plan

This is due to a number of reasons. Firstly, as consumers become more sophisticated, they are starting to use their previous traditional bank as a warehouse for deposits and then using their new providers for very specific directed transactions and payments. They are, in effect, creating a financial wellness plan for themselves with lots of providers. The very specific use cases that some smaller fintechs provide have enabled them to win accounts. Another reason is that banks are still too slow to open accounts. As Jim says traditional banks take up to 15 minutes to open an account which, in this day and age, is simply unacceptable. By comparison, SoFi and Chime take four minutes each to open an account.

On top of that, banks are not engaging with customers like other apps. If you get an Uber to pick you up at an airport and take you to your hotel, along the way Uber will ask if you’re going out to dinner and suggest restaurants, and if not suggest food that Uber Eats can send straight to your hotel for your arrival. When you follow a route using GPS in your car, it no longer tells you just where to go but it suggests Starbucks, restaurants, and other retail stores along the way. In both these examples as Jim points out, ‘Intellectually they are learning who you are and how you act and react’.

So, what can banks do?

They need to provide empathy. In other words, they need to provide engagement with customers as opposed to just an experience. AI and Generative AI can help banks crack this. Banks need to use these new tools to increase personalisation.

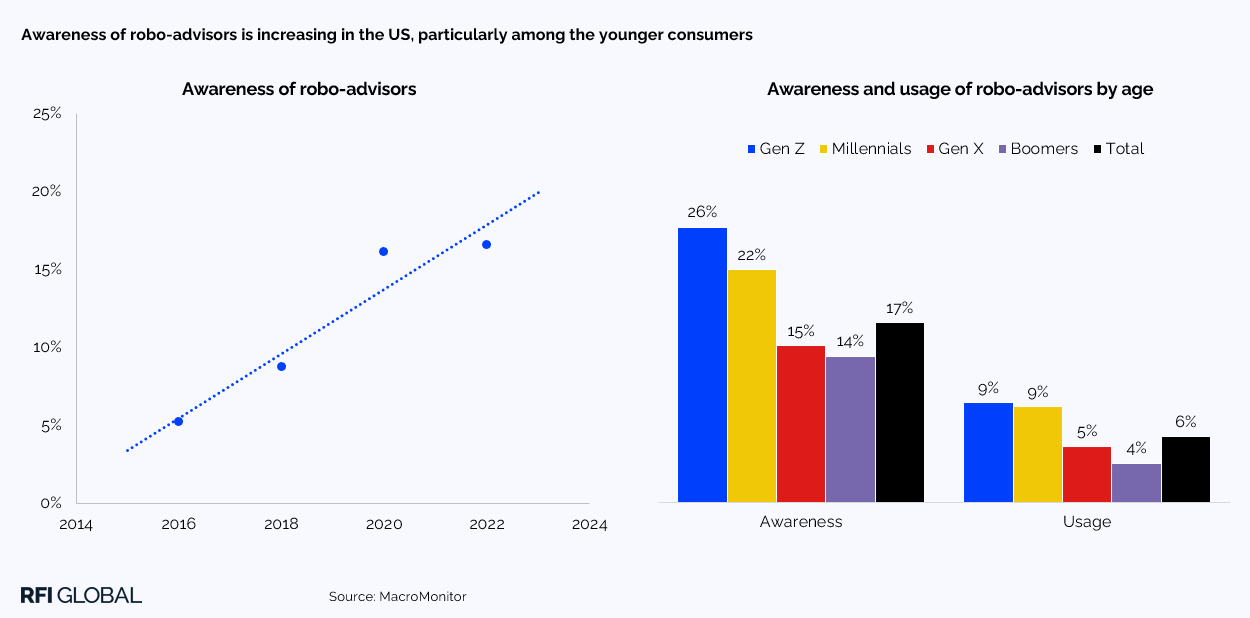

Personalisation is key and it is up to banks to understand the balance consumers want between human and digital. As opposed to their historical one-sided conversations they need to understand how customers act and what they want and then banks can act on that to create prompts and suggestions. This is what creates engagement. Whether it’s robo-advice or personalisation customers are more than happy to provide information that will allow banks to do this or even work with AI to decide how they want to invest.

The top 5-7 banks in the US are starting to do well, but they already know more about their customers than probably most of their customers are aware of. This isn’t the issue. Jim says it is the deployment of solutions based on this knowledge that is the problem.

The fintechs are now definitely here. They are engaging with customers. Unless banks leverage AI to create personalisation and engage with customers, fintechs will continue to increase market share at the expense of traditional banks.

Listen to the Banking Uncovered podcasts with Jim Marous to find out more:

Futureproofing finance part 1 – Digital innovation, AI and the dawn of the fintech

Futureproofing finance part 2 – Customer engagement, branding and next-level innovation in banking

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.