Luke Allchin, Director, North America

US households are grappling with financial challenges at levels unseen since the 2008 financial crisis. Inflation, fluctuating markets, and economic uncertainty have forced many people to re-evaluate their financial plans, explore new financial products and even switch their financial providers. Yet, despite the rising need for financial advice, fewer consumers seek guidance from experienced financial professionals. This begs the question: Why are people avoiding professional advice when they’re unsure about their financial future?

Financial decision-making

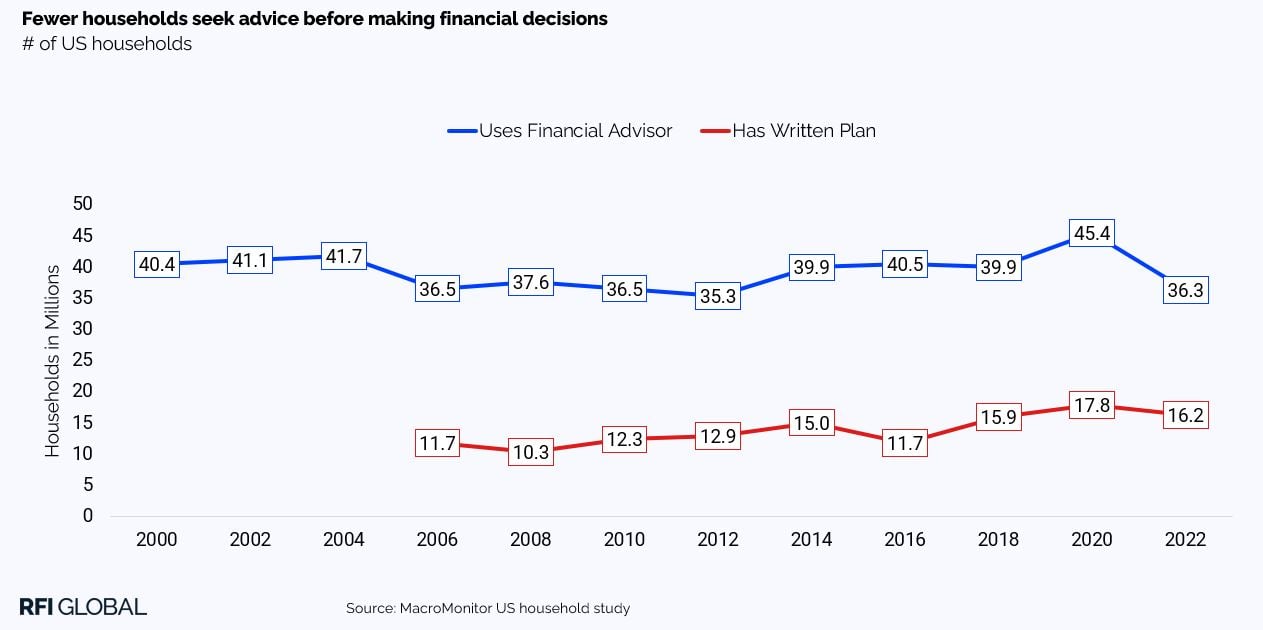

Households that seek advice before making major financial decisions consistently report more confidence in reaching their financial goals, according to MacroMonitor data. Yet, the number of households getting financial advice before making financial decisions has sharply declined since 2020.

In contrast, 61% of US households are willing to accept some level of risk in their investments, but the majority (58%) express doubt about their ability to choose appropriate products and accurately assess risk.

This gap between financial confidence and the reduced use of professional advisors is significant. This trend is exacerbated when examined by household wealth. Mass market households (those with less than $100k in investable assets) display the lowest level of confidence and face the greatest risk of making ill-informed decisions, yet they are the least likely to seek expert advice.

Is financial advice a luxury purchase?

One key factor contributing to this decline is cost. Many families now view financial advisory services as a luxury, especially in an era where inflation has tightened household budgets. As discretionary spending shrinks, so does the willingness to pay for services once deemed essential.

Simultaneously, the rise of affordable digital alternatives – personal finance management (PFM) apps and robo-advisors – has empowered consumers to take a more DIY approach to financial management. These platforms offer financial insights, budgeting tools, and investment advice at a fraction of the cost of traditional advisory services, reinforcing the perception that paying for professional guidance is unnecessary.

Digital tools and social media

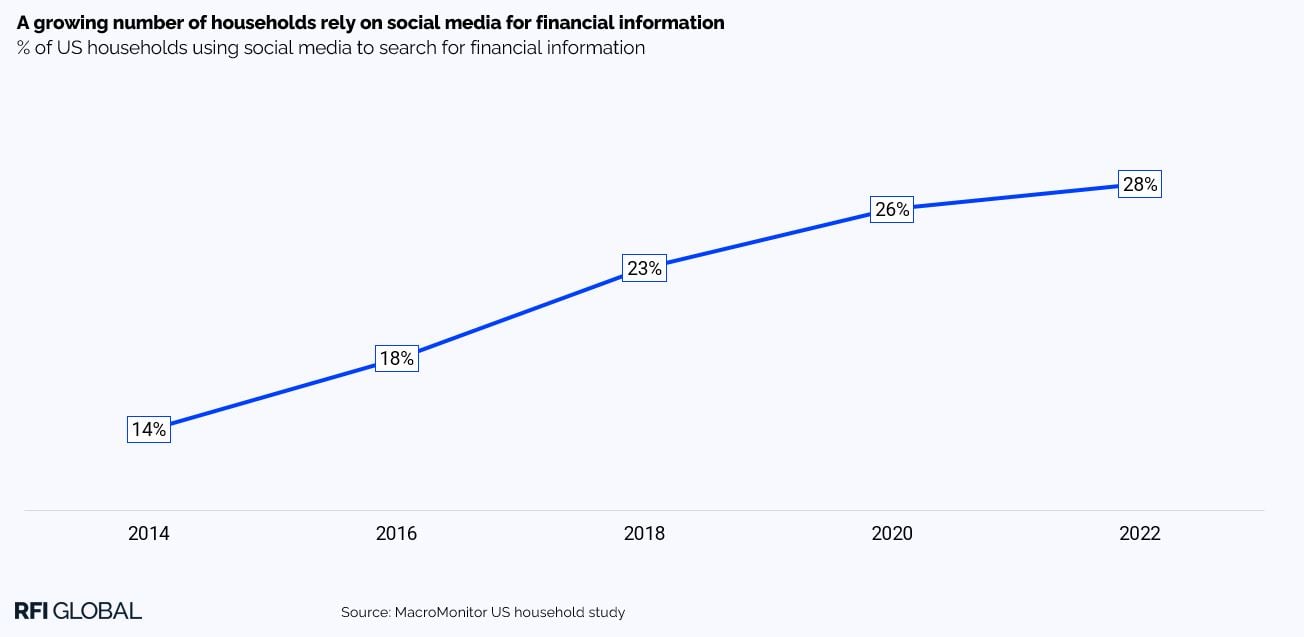

This shift toward digital solutions has been fueled not just by cost considerations but also by the growing availability of financial information online. From blogs and podcasts to webinars and social media platforms, consumers have access to an ever-growing library of financial information and advice online.

Social media has emerged as a key player in this transformation. Consumers, especially Millennials and Gen Z, are increasingly turning to “finfluencers” and online communities for guidance. Platforms like YouTube, TikTok and Facebook have become vital sources for financial education, from health insurance tips to investment strategies. Interestingly, while younger generations lead this trend, older generations are also engaging in social media, closing the digital gap, and displaying a growing comfort in using online tools for their financial management.

While these platforms have democratized financial knowledge, they have also introduced risks. The rise of self-directed investing, fueled by social media recommendations, can create a false sense of confidence. Consumers, particularly those new to investing, may follow trends without fully understanding the risks, leading to financial missteps.

The inflationary push toward riskier investments

In the current economic climate, consumers are also becoming ever more willing to take on greater risk in their investment strategies. The quest to outpace inflation has driven many households to move away from conservative investment strategies, opting instead for higher-risk, higher-reward options.

This marks a significant shift from the post-2008 financial crisis period, where consumers largely became risk averse. Now, with inflation looming large, the appetite for risk is on the rise again. However, for some, this growing willingness to embrace risk is paired with a lack of confidence in navigating increasingly complex financial markets. This highlights the need for personalized, strategic advice – whether from a human advisor or a sophisticated digital tool.

Striking a balance between digital tools and human expertise

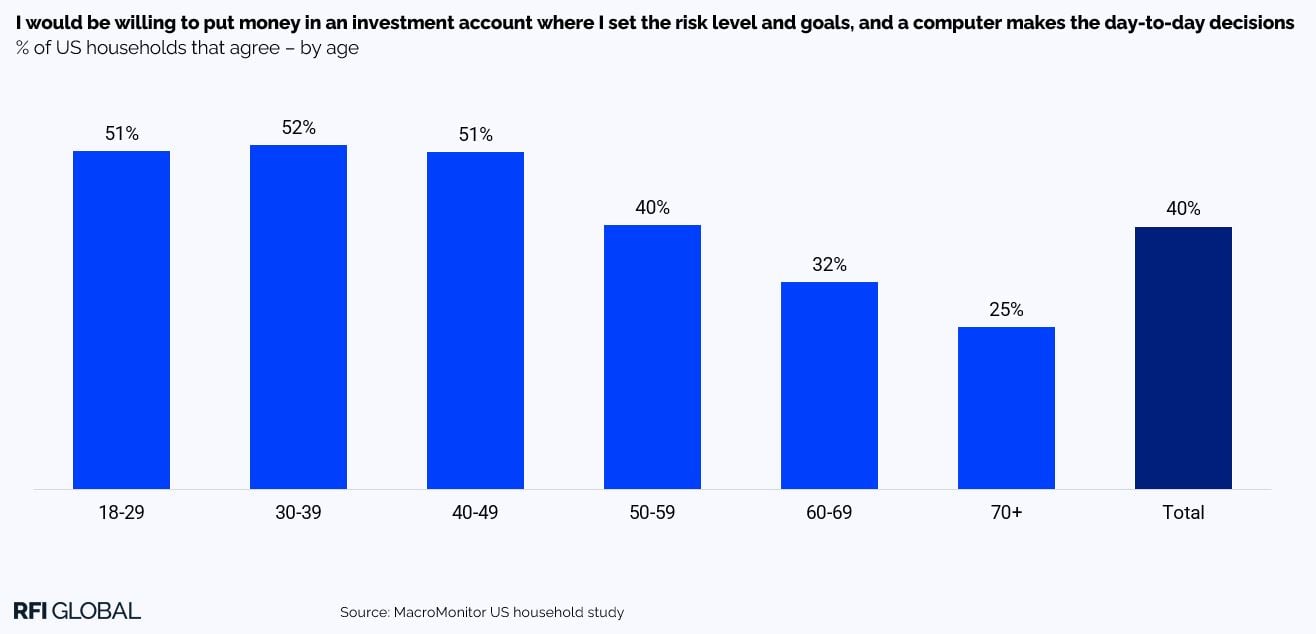

As the complexity of financial markets continues to evolve, so too does the role of wealth advice services. One of the most significant innovations in recent years has been the rise of AI-powered robo-advisors. These platforms have democratized access to professional-grade investment management, making it accessible to individuals who may not have had the assets to engage traditional advisors.

Despite consumers displaying greater trust in traditional advisory services, compared to the alternatives, many are still willing to allow AI to manage their day-to-day investment decisions, with consumers aged 30-49 being the most trusting of robo-advisors.

While robo-advisors provide cost-effective, automated solutions, they lack the human touch necessary for more complex decision-making. Which begs the question: Does the future of financial advice lie in hybrid models? Models that combine the efficiency and scalability of AI with the personalized insight and empathy of human advisors.

The future is hybrid

The shift toward digital solutions, coupled with the ongoing economic challenges, means that financial institutions must adapt quickly to meet consumer needs. The convenience and affordability of digital tools have created a new standard, but there’s still a vital role for human advisors.

Hybrid models that integrate digital tools and AI-powered robo-advisors with human expertise will provide the flexibility, cost-efficiency, and personalized service that today’s consumers demand. With inflation pushing consumers toward riskier investments and the increased rate of financial product uptake and switching, expert guidance is more critical than ever.

In these uncertain times, consumers are hungry for both control and confidence. Financial institutions can be the ones that offer them that. It comes down to striking the right balance between offering digital tools to help consumers manage their finances independently while also providing affordable, personalized advice when needed.

Subscribe to get the latest RFI data and insights.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.