Luke Allchin, Director, North America

The US housing market has stagnated over the past two years, primarily driven by the economic consequences of high mortgage rates, affordability challenges, and slow construction growth. Though mortgage rates are beginning to ease for borrowers, they remain significantly higher than before. This shift has left many potential buyers on the sidelines and altered the behavior of homeowners and first-time buyers.

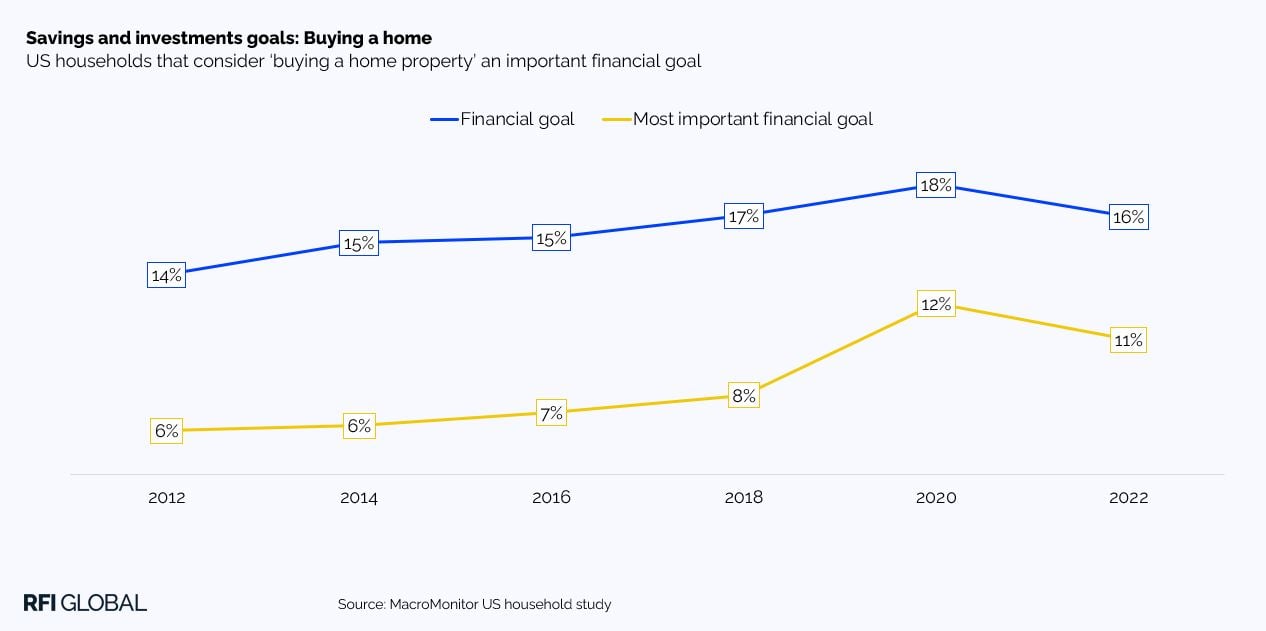

MacroMonitor data shows how households’ financial goals have shifted over time. In the decade leading up to 2022, households focused more on achieving their homeownership goals. This steady increase is reflective of the reality that it takes the average household longer to achieve this financial goal than previously.

More recently, the cost-of-living challenges faced by many households have forced some to reevaluate their financial goals and focus their efforts elsewhere, which is why the goal of homeownership dipped in 2022. While buying a home remains an important financial goal for 16% of households, it is possible that some now view it as unobtainable, resulting in them abandoning this once important financial goal.

High interest rates and the lock-in effect

The surge in mortgage rates since the start of 2022 has been a central factor in the housing market’s current state. While rates have started to fall, they remain elevated compared to the historical lows experienced the decade prior. The average 30-year fixed mortgage rate reached lows of 6.08% in September, down from 7.79% in late 2023 . These higher borrowing costs have created a significant barrier for home buyers and sellers.

For homeowners who locked in historically low mortgage rates before 2022, the prospect of selling their current homes and purchasing a new one at today’s higher rates is financially daunting. Many homeowners are effectively ’locked in’ to their existing mortgages, resulting in a reluctance to list properties for sale. This lack of new listings has been a key driver of stagnation, with fewer homes available to meet buyer demand.

The reduction in home listings has supported the rise in house prices. According to Redfin, the median sales price of an existing home reached $416,700 in August 2024, marking the 14th consecutive month of year-over-year price increases. Despite rising interest rates, sellers remain steadfast on pricing, which continues to impose affordability challenges on would-be buyers.

Rising construction costs and supply constraints

New home construction, which could have been a solution to the tight supply of homes for sale, has also been hampered by rising construction costs. The cost of building materials and labor shortages have pushed up the prices of new homes, making it difficult for builders to meet the growing demand. As construction costs rise, so do home prices, creating a self-reinforcing cycle that further tightens supply and limits buyer options.

This supply constraint has significant implications for market dynamics. Rising home prices in an environment of elevated borrowing costs have led to a growing affordability crisis. As affordability worsens, homeownership becomes increasingly out of reach for many consumers, particularly first-time buyers, who struggle to save for down payments amid rising everyday living costs.

Home ownership: The end of the American Dream?

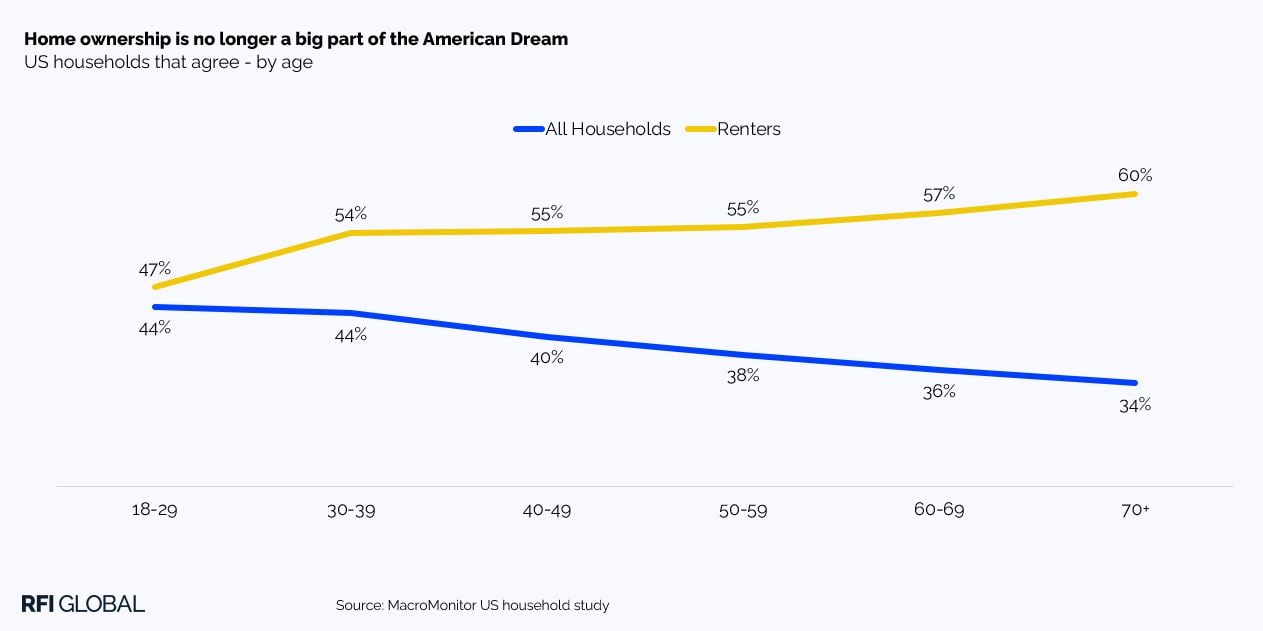

Affordability concerns and high borrowing costs have fundamentally shifted consumer attitudes toward homeownership. MacroMonitor data shows that 38% of US households believe homeownership is no longer a significant part of the American Dream. This sentiment is particularly prevalent among the younger generations.

Hopes of homeownership diminishes the longer a household rents and the notion that ‘Home ownership is no longer a big part of the American Dream’ becomes more strongly felt by renters.

Moreover, 77% of US households say they would never take out a mortgage with an adjustable interest rate, indicating a strong preference for financial stability in uncertain times. This reluctance to take on variable-rate loans limits the flexibility of lenders and suggests a continued preference for fixed-rate products.

Navigating a changed market

For lenders, these market dynamics present both challenges and opportunities. The stagnation in housing transactions, combined with high mortgage rates, has dampened demand for new mortgages and refinancing activities. Lenders must adapt to an environment where many homeowners choose to stay put rather than sell or refinance their existing homes.

However, as rates gradually decrease, there could be an uptick in refinancing activity from homeowners seeking to lock in lower rates. Lenders may find opportunities to target existing homeowners with favorable refinancing offers or home equity lines of credit (HELOCs) as an alternative source of liquidity.

Another area of opportunity lies in product diversification. Given the strong consumer preference for fixed-rate products, lenders may need to innovate around hybrid fixed-rate options or adjustable-rate mortgages (ARMs) with capped increases to attract more risk-averse borrowers. This could allow them to offer competitive rates without fully embracing the volatility of traditional ARMs.

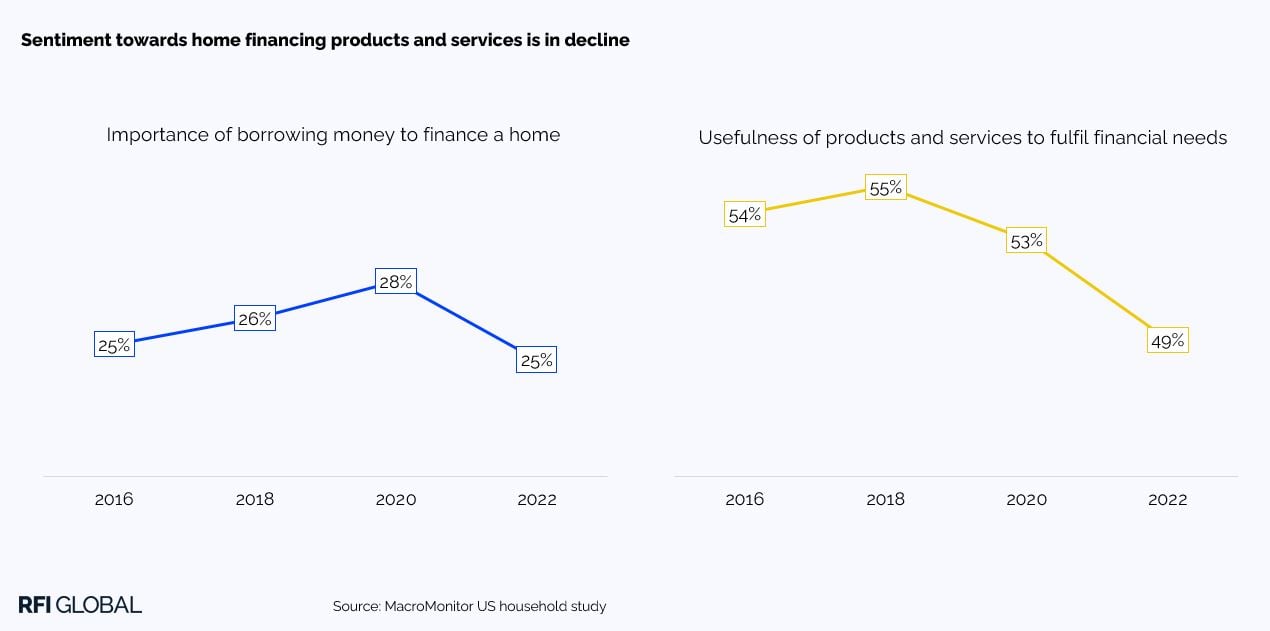

Our data shows that consumer sentiment towards home financing products and services has been in decline since 2018, with less than half of US households considering the products and services provided by lenders useful.

Managing risk and growth

The current economic environment also forces lenders to carefully manage risk. Rising interest rates and higher home prices may lead to increased credit risk as more borrowers find themselves stretched financially. Lenders must be cautious in their underwriting standards to avoid creating conditions like the 2008 housing crisis, where overly aggressive lending practices led to widespread defaults.

Furthermore, regulatory oversight remains a crucial consideration. Regulators are paying closer attention to lending practices, particularly in the context of rising home prices and affordability challenges. Lenders must ensure compliance and find ways to remain competitive in a stagnating market.

What to expect in 2025 and beyond

As we look toward 2025, the future of the housing market centers around several key factors. First, the trajectory of mortgage rates will play a significant role. If rates continue to decline, we could see more homeowners willing to list their homes, increasing new listings and alleviating some of the supply constraints. However, a sharp drop in rates could reignite demand and push prices even higher, exacerbating affordability challenges.

Second, the pace of new home construction will be critical. If construction companies can ramp up production and address supply shortages, it could help stabilize home prices and offer more affordable options for buyers. However, ongoing cost pressures in construction remain a concern.

Finally, consumer sentiment around homeownership will be an essential factor to monitor. If younger generations increasingly view homeownership as unattainable or unnecessary, it could lead to long-term structural shifts in the housing market. Lenders may need to adapt their product offerings to cater to changing preferences, such as focusing on rental financing or innovative co-ownership models.

While the US housing market has become a more challenging environment, opportunities still exist for the lenders willing to innovate and respond to evolving market trends and changing consumer preferences.

Subscribe to get the latest RFI data and insights.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.