Edward Smith, Lead Analyst, North America & EMEA

Comprising around 25 million US households at the end of 2024 (up from 5.6 million in 2004), Hispanic consumers represent one of the fastest-growing cohorts of the US market. Historically underserved by financial institutions, Hispanic investors are a driving force among the Mass Market, leading the way in exploring innovative new tools and product solutions.

MacroMonitor, the largest survey of US households’ financial behavior, allows us to explore their needs and challenges in depth versus other population segments. By understanding the distinct barriers they face and strategies they use to overcome these challenges, financial providers can uncover how to better guide the journeys of these would-be affluents.

Investment opportunity barriers: debt and dependents

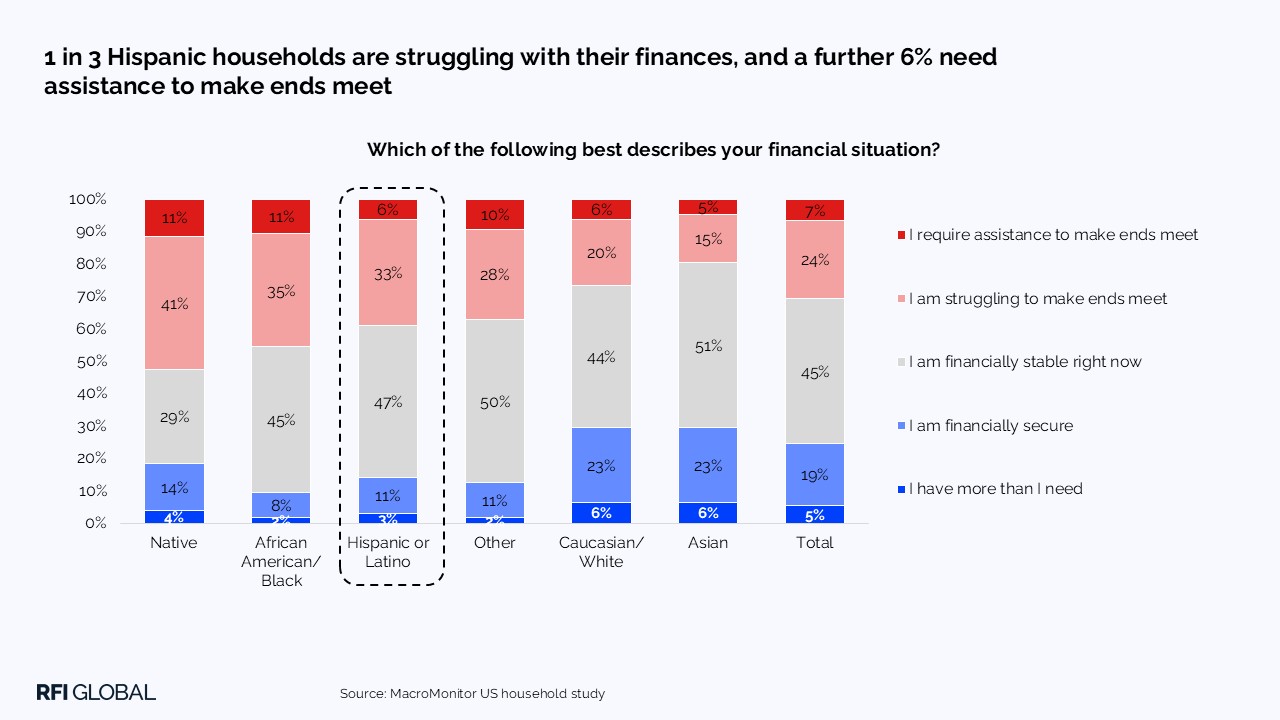

Life often gets in the way of Hispanic investment opportunities; a third of Hispanic households struggle to make ends meet, and a further 6% need additional assistance to get by. Debt is the crux of the issue, as many express difficulties managing larger ticket items alongside regular credit and household financing – 63% of Hispanic households would use an unexpected windfall to pay off debts.

Maintaining the welfare of their dependents adds further complication for Hispanic households, which tend to be composed of young families. On top of heightened concerns toward housing costs and job stability, 1 in 10 Hispanic households expresses that family responsibilities are a significant source of stress. Further, a third of Hispanic households include at least one member born outside the US and therefore are less likely to have well-established financial relationships. As a result, Hispanic heads of household find themselves navigating more complex financial problems with less available support from their personal networks.

Found between a rock and a hard place, Hispanic decision-makers typically de-emphasize longer-term financial goals, such as preparing for retirement and saving emergency funds, in favor of more immediate priorities like buying a home and paying off the mortgage. Hispanic households are aware that this could leave them underprepared, as 68% worry that they are not saving enough for future needs. Addressing these pain points requires tackling the source of their low consumer confidence:

- 44% of Hispanic households lack a dedicated financial strategy, compared to 34% of the rest of the market.

- Hispanic households harbor a deep-seated aversion to risk, taking guaranteed income over the potential for high returns or even government insurance on their savings.

Hispanic appetite for innovative wealth solutions

Hispanic ownership of traditional investment vehicles has routinely lagged the wider market. While 23% of all US households bought or sold stocks in the last 2 years, only 15% of Hispanics did. Limited trust in and understanding of stockbrokers, mutual fund companies and other dedicated firms has heavily restricted Hispanic engagement through traditional investor channels.

Fortunately, Hispanic attitudes indicate an intent to catch up; 22% are keen to learn how to choose investments and 47% are interested in exploring a savings plan for their children’s education (vs 38% of the market). Likewise, Hispanic interest in micro and youth investment accounts surpasses that of other would-be investors. In other words, Hispanic consumers are open to trying entry-level investments that are clearly attached to tangible objectives.

There is one product area, however, where Hispanic adoption has consistently exceeded the market: cryptocurrency. As of 2024, 7.1% of Hispanic households held active cryptocurrency wallets, vs 6.7% of all households. Seemingly at odds with their lower overall risk tolerance, this behavior represents the broader disconnect between aspiration and opportunity. Hispanic investors are able and willing to explore alternative investment options, but, as their higher rate of crypto holding attrition shows, they need additional support identifying what products are best for their situation.

Expand advisory uptake with AI

Improving access to advice would help bridge this gap. Currently, 57% of Hispanic households consult advisory sources before making significant financial decisions, compared to 65% of all households. Regarding the sources used, these households are significantly less likely to use professional certified financial planners and public accountants, relying instead on bank officers. Affordability and familiarity drive choice, which banks are well-positioned to leverage.

AI-powered services should be integral to onboarding Hispanic customers onto advisory channels. Tools such as predictive analytics and robo-advisors are much more appealing to the Hispanic segment, principally due to the perception that AI is less subject to personal bias. Providing management tools that highlight and encourage regular savings habits on mobile banking apps, which Hispanic individuals are more likely to use, would be an effective foundation to then promote more comprehensive financial planning.

Key strategies to win over loyal Hispanic consumers

Hispanic households face many financial challenges, but their recent behavior reveals an active willingness to adopt new solutions if a clear use case is shown. For financial institutions, the next step is to craft a proposition that speaks to their interests, which could be achieved through the following:

- Help Hispanic customers to formalize their financial plans, especially those with active mortgages or other liabilities, with goal-oriented tools. Messaging should emphasize long-term goals such as home-ownership, child education and retirement saving.

- Promote aggregator investment and savings tools that streamline and simplify micro-investment habits. Clear communication, such as graphical estimates of compound growth, can highlight how the institution can maximize the value of customer deposits, laying the foundation for potential cross-sell.

- Integrate AI educational assistants for more complex topics, such as tax planning, to build trust. Services that can benchmark the users’ experience against those in similar circumstances, and direct customers to a trusted representative with a clear outline, would be greatly valuable – doubly so when packaged with transparent safeguards.

For more information on the key financial trends in the US market and the key consumer segments driving innovation, get in touch.

Edward Smith

Lead Analyst, North America & EMEA

Edward Smith is a Lead Analyst at RFI Global, covering financial services trends across North America and EMEA.

View full profileFAQs: Hispanic investing trends and barriers in the US

Q: Why are Hispanic households an important growth opportunity for financial institutions in the US?

Hispanic households are one of the fastest-growing segments of the US population, reaching approximately 25 million households in 2024, up from 5.6 million in 2004. Many are part of the aspirational Mass Market and show strong interest in building wealth through savings plans, investment education, and new financial tools, creating significant opportunities for financial institutions.

Q: Why do many Hispanic households invest less than the overall US market?

Investment participation among Hispanic households is lower than the overall market due to financial pressures and structural barriers. Debt levels and family responsibilities often take priority over long-term investing, and many households lack a formal financial strategy. As a result, fewer Hispanic households participate in traditional investments such as stocks compared with the broader US population.

Q: How does Hispanic investment behavior differ from other US households?

Hispanic households tend to be more cautious about financial risk and often prioritize guaranteed income and financial security. Participation in traditional investments is lower, but interest in learning about investments and saving for children’s education is higher than the overall market. Hispanic households are also more open to entry-level investment solutions that support clear financial goals.

Q: How can banks and financial institutions better support Hispanic investors?

Financial institutions can support Hispanic investors by improving access to financial advice and providing goal-based savings and investment tools. Digital advisory services, including AI-powered tools and robo-advisors, can help make financial planning more accessible and easier to integrate into everyday banking channels such as mobile apps.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.