At RFI Global, we conduct tens of thousands of interviews every year with Australian consumers regarding their payment preferences and habits. We also conduct an annual study, where consumers record all their transactions for a week. Now in its 15th year, the RFI Australian Payments Diary provides a fantastic trend analysis of consumer behaviour in what is a rapidly changing market.

On a personal note, it’s fair to say that I spend more of my time thinking about how consumers pay for things than the average person. I read the payments articles in the media, and I consume – sometimes wincing – the things I see on payments on LinkedIn.

At times, there are conflicting views on the direction of evolution of payment behaviour in Australia. As we’ve just released our new Payments Diary, I thought it would be a good time to lay out two fundamental trends that I see shaping the landscape and, importantly, back them up with data.

These are:

1. Cash is dying as a payment mechanism, but it’ll live on for a while

2. Debit card-powered mobile wallet transactions will dominate everyday payments

1. Cash is dying as a payment mechanism, but it’ll live on for a while

The outlook for cash is a surprisingly contentious area. There are those who want to protect cash usage and acceptance and who see growth in its usage where no growth exists.

The fact is that in 2015, more than 80% of consumers were using cash at least once per month (our measure of habitual usage) and in 2025, that figure has fallen to 45%.

Further, as I’ve written about before, there is a demographic shift that adds to the decline of cash usage. 59% of over-55-year-olds use cash in a month, vs 29% of under-25-year-olds. Those younger consumers will make up a larger and larger share of purchasing power in the next decade as the over-55s decline as a force.

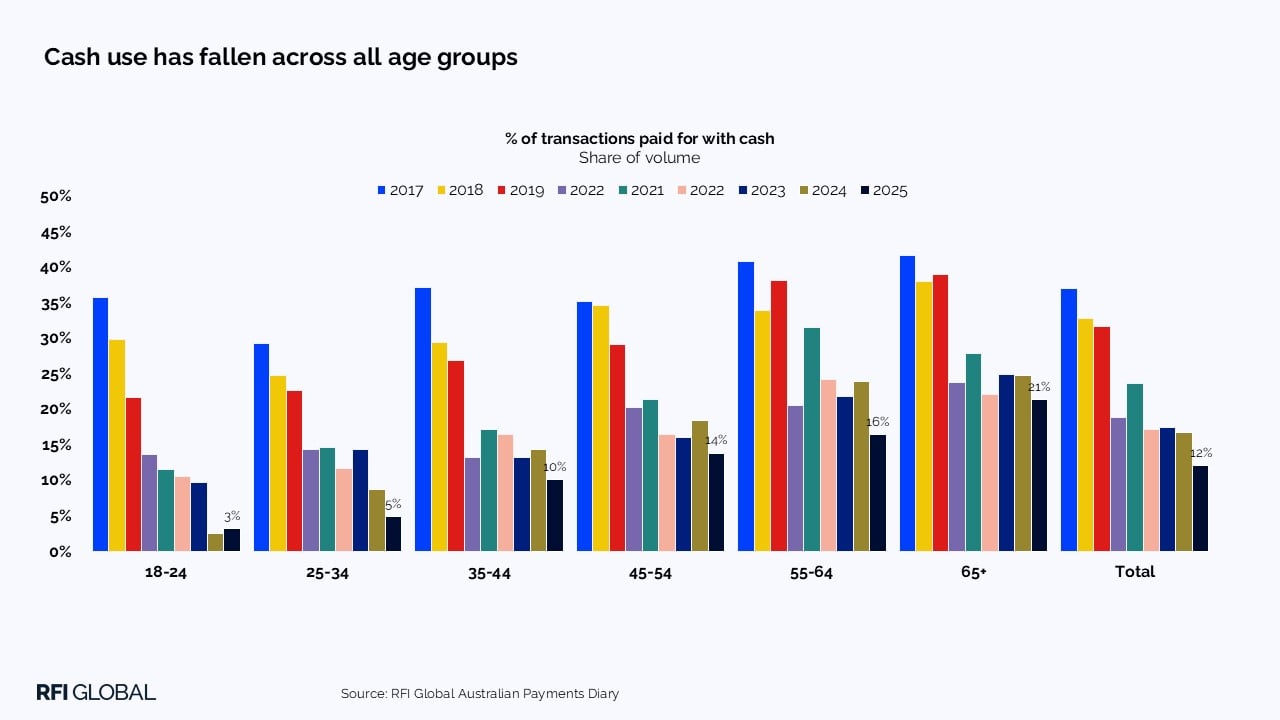

This shift is impacting transaction volumes. When we look at the volume of cash payments made by consumers using our diary, we can see that it accounts for 12% of all transactions; down from 17% a year ago and 37% in 2017. So, what is the share of transactions that under-25s make with cash?

Just 3%.

But wait…. Hasn’t the Reserve Bank of Australia just released data that says the total value of notes on issue has reached an all-time high? It has. In fact, the total value of banknotes in circulation is $104 billion.

This might sound contradictory, but much of this cash is not being used for everyday payments. It is being hoarded by – predominantly older – consumers as savings and used by others in the grey and black economy. If that sounds unbelievable, then consider this, there are more $100 notes in circulation (504 million) than there are $20 notes (187 million). Now ask yourself… when was the last time you had or saw a $100 note? I rest my case.

2. Debt card-powered mobile wallet transactions will dominate everyday payments

It’s not just cash usage that will be influenced by demographics; the whole shape of mobile payments evolution will turn on the usage of younger consumers.

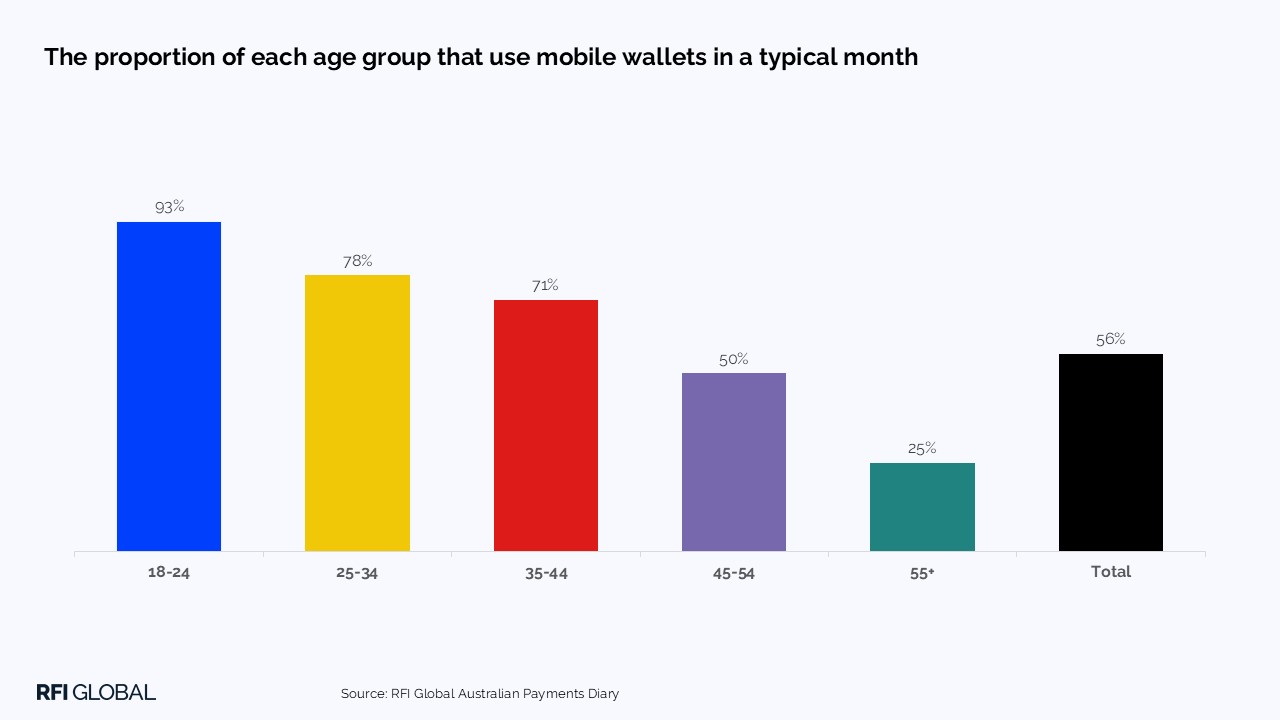

There is, of course, no doubt that mobile wallet usage is growing in Australia as well as other markets. To put this into perspective, in 2025, 56% of all consumers use mobile wallets in a typical month, a figure which has increased from just 8% in 2015!

Furthermore, if we dive into the demographics, we can see that while usage has increased for all age groups, in 2025, 93% of under-25-year-olds use mobile wallets each month, compared to just 25% of over 55’s.

Alongside this growth in mobile wallet usage, we know that younger consumers are also more reliant on debit cards than credit cards. Less than 30% of under-35s use credit cards in a typical month, vs more than 50% of over-45s.

The future of payments in Australia

If we put these data points together, then it follows that younger consumers will be making their mobile wallet payments, underpinned by debit cards. And that is exactly what the data shows.

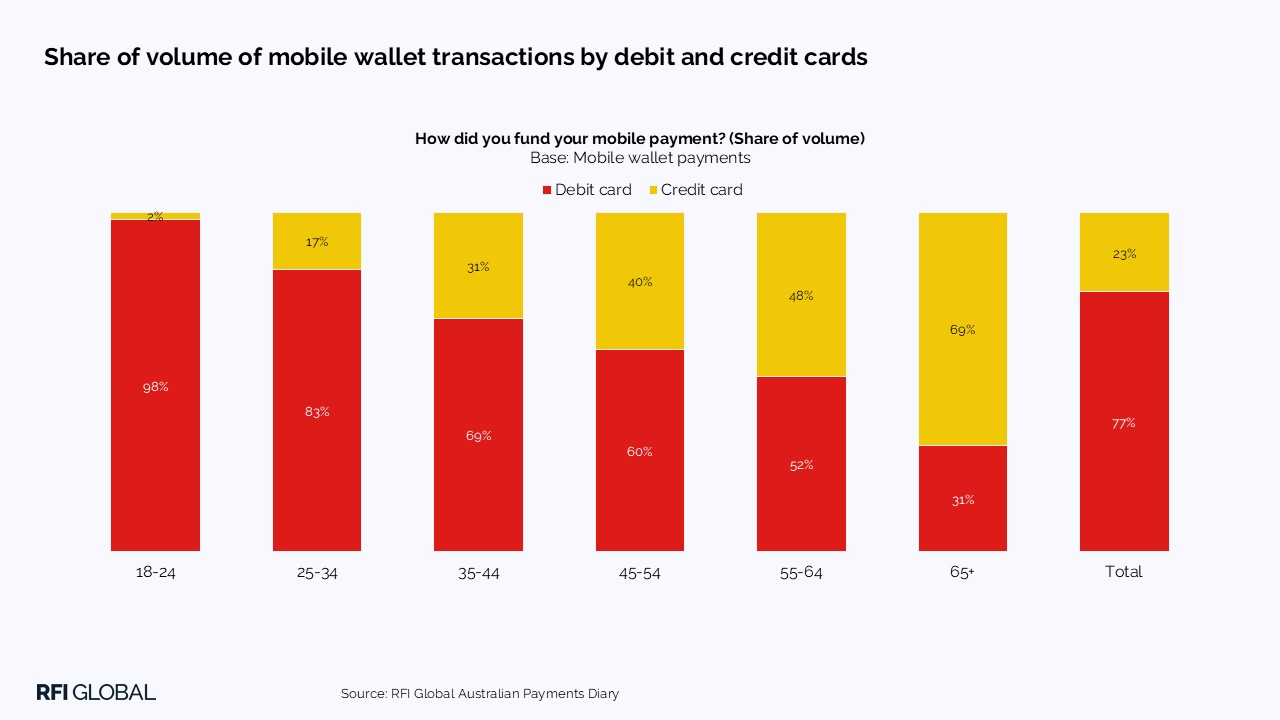

Our Payments Diary shows that in 2025, just 2% of mobile wallet transactions made by under-25s were underpinned by a credit card. A whopping 98% were debit-backed.

By contrast, almost half of the mobile wallet payments made by 55-64 year-olds were credit card-backed. The difference here is stark.

Similar to our cash analysis, if we project this trend forward over the next 10 years, then we can see that these younger consumers will grow as a force in payments, in both value and volume.

It’s not hard then to see that mobile wallet transactions will continue to grow and slowly begin to dominate in the everyday payments space. It’s also not a stretch to see that debit-backed mobile wallet transactions will become even more dominant than they already are.

Will younger consumers begin to pick up cash and stop using mobile wallets? The answer to that is, not likely.

Get in touch for more insights from our Global Payments Diary.

Frequently Asked Questions

Q: Is cash disappearing in Australia?

A: Yes, cash usage in Australia is declining sharply. In 2015, over 80% of Australians used cash monthly, but by mid-2025 that figure had fallen to 45%, with younger consumers driving the shift away from cash.

Q: What is replacing cash for everyday payments in Australia?

A: Mobile wallet payments, primarily backed by debit cards, are becoming the dominant method for everyday transactions, especially among younger Australians.

Q: How popular are mobile wallets in Australia?

A: Habitual mobile wallet usage has grown from just 8% of Australians in 2015 to 56% in 2025. Among under-25s, adoption is near-universal at 93%.

Q: Are Australians using credit or debit cards with mobile wallets?

A: In 2025, 98% of mobile wallet payments by under-25s are debit-backed, whereas older generations are much more likely to use credit cards, showing a clear generational divide in payment preferences.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.