Neo – Definition, ‘New’. A new or revived form of. So, neobanks are new banks challenging the established form of banking and the status quo. So far, so expected. Except that what we call neobanks are often not that new anymore.

In fact, if you search ‘neobank examples’ in Google, the top brands it picks up are shown in the table below, and the newest of them is now 10 years old.

So, what has happened in that decade? Have the Neobanks achieved what they set out to achieve? To challenge the banking orthodoxy; to deliver a superior digital customer experience; to make inroads into the ‘main bank’ market share.

To mark this maturity, it’s worth delving into the numbers.

Challenging orthodoxy

Arguably, the opportunity to challenge the orthodoxy has never been greater than it has been over the last decade. We’ve seen digital banking rise to primacy in terms of banking channel dynamics, and we’ve had a huge upheaval in the way people live their lives due to the pandemic.

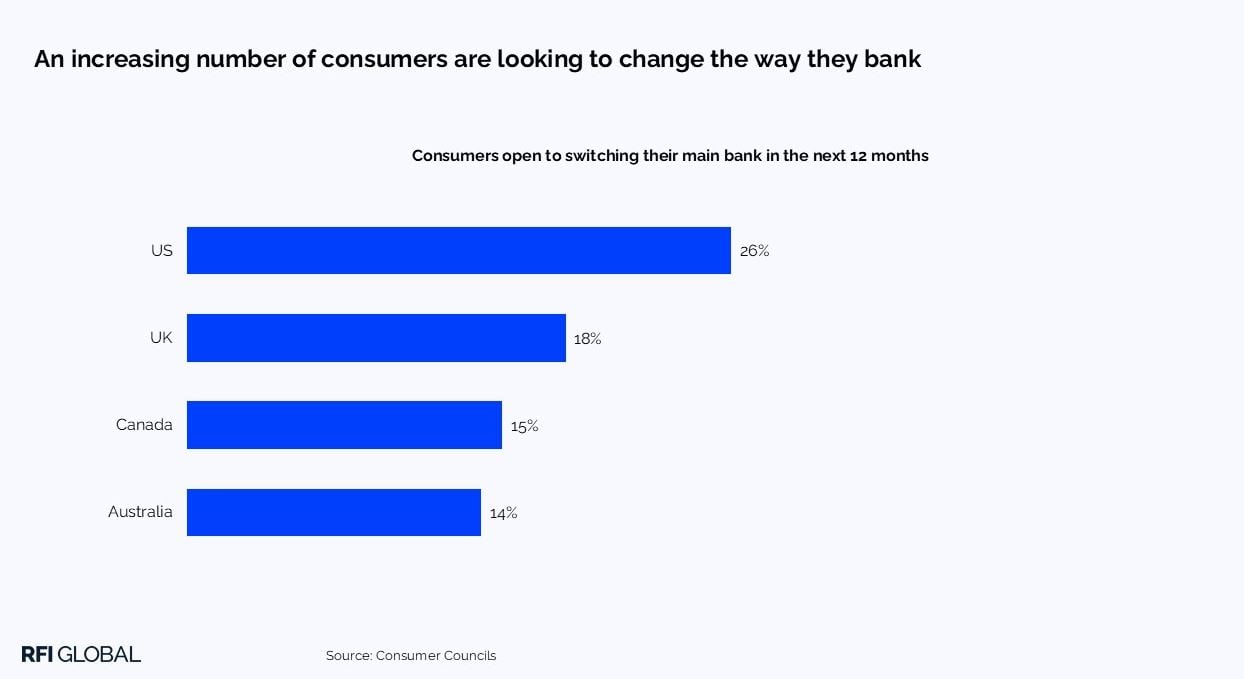

When we look at the data on the proportion of consumers looking to switch their main bank, the opportunity is huge. More than one in four consumers is open to switching their main bank in the next 12 months. Likewise, more than one in four US consumers is open to switching, one in five UK consumers and one in six Canadian and Australian consumers are open.

Have the neos taken advantage? There is no doubt that these digital-first banking brands have made inroads into the markets in which they operate.

In the UK, digital-only players have at some point counted a whopping 56% of the population as customers, up from 16% in 2018. And, in the US, 30% of households have accounts with a digital-only bank.

While these figures sound impressive, the criticism levelled at the digital-only banks has always been that these relationships have not translated into main bank share – a measure of how closely engaged customers are and of the opportunity to provide further products and services to these customers.

Making inroads into main bank share

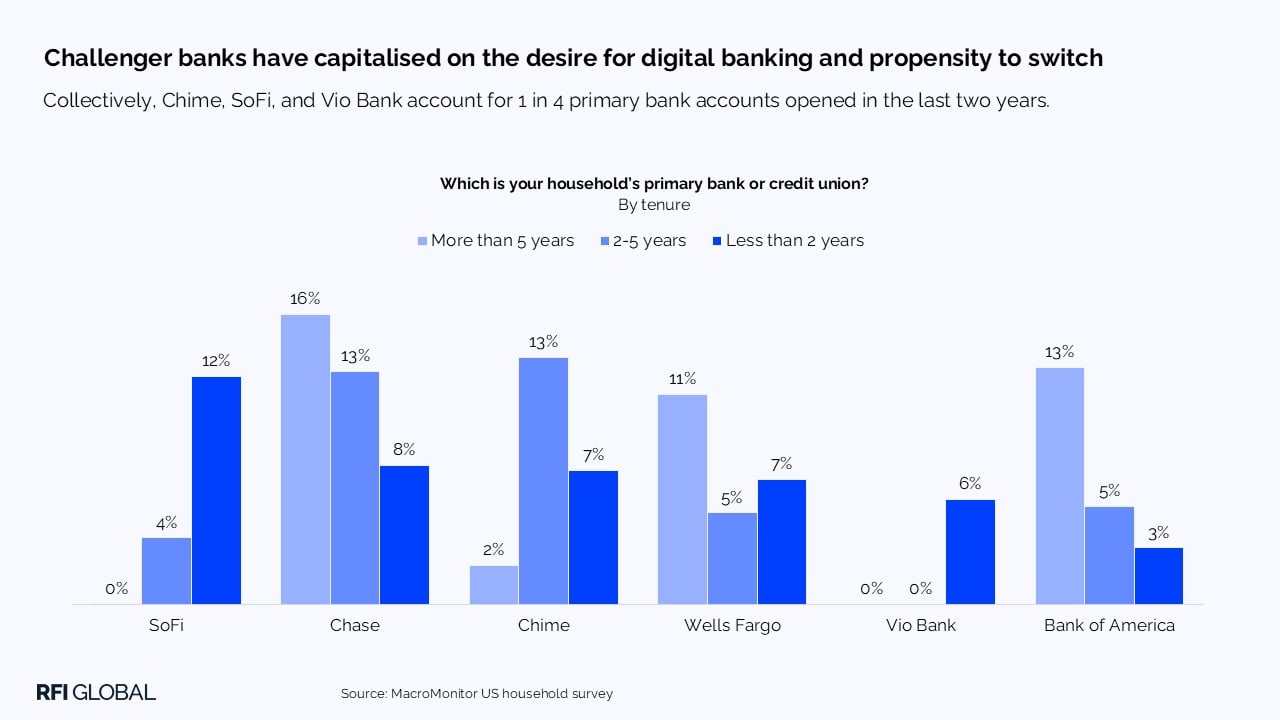

Is this criticism still fair? RFI Global’s US MacroMonitor Study shows clearly that if you break down primary bank or credit union share by customer tenure, the new banks are the big winners.

Established banks like Chase, Bank of America and Wells Fargo see their combined share of these relationships fall from 40% of those with more than five-year tenure to 17% among relationships of less than two years.

At the same time, Chime, SoFi and Vio Bank have seen their combined share of relationships climb from 2% of those with more than five-year tenure to 25% among relationships of less than two years.

If you’re interested in preserving the status quo, then that is a worrying trend, whichever way you cut it.

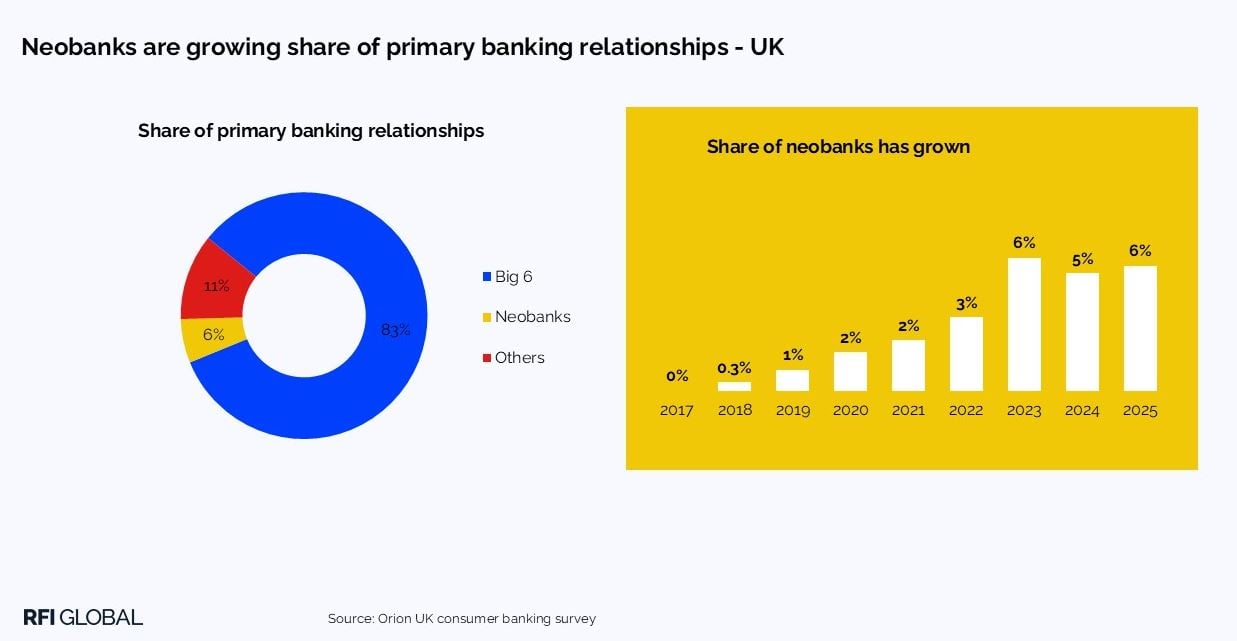

And it’s a similar story in the UK as shown by RFI’s Orion Consumer Banking Survey. Between 2017 and 2022, neobank share of main bank relationships grew steadily to 3%. However, at that point, whether through critical mass or acceptance at a wider scale, in 2023 the share doubled to 6% and has remained at that level ever since.

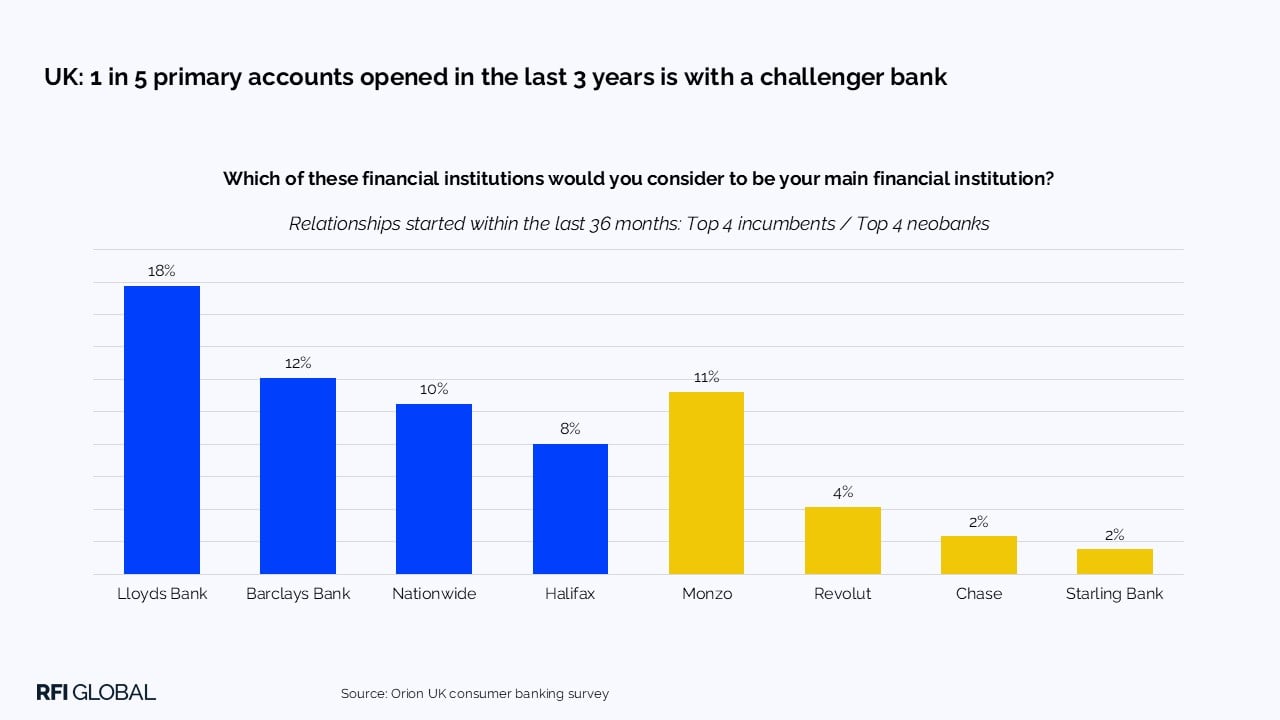

If we look at new accounts opened in the last 36 months, the progress is even more startling. In fact, almost 20% of main bank accounts opened in that period were with the neobanks, and Monzo on its own is the 3rd largest recipient of these new accounts behind Lloyds and Barclays. The momentum is well and truly with the challengers.

So, what next?

Demographics are on the side of the challengers. Younger adults who are just starting out in the world of banking will have grown up with these brands and regard them as legitimate parts of the landscape – not new; just there.

As these consumers age and account for a larger proportion of the banking customer base, there is an inevitability about the growth of the main bank share of the challengers. Demographics are a slow and powerful force in any trend.

On the flip side, these digital players will need to expand their offerings to cover a greater array of products and services. One cannot hope to be relevant to consumers without offering credit products alongside savings and transactions products.

This evolution will see neos become part of the furniture and open to challenges from the next wave of banking and fintech services. At some point, we might need a new name. No longer ‘neobanks’ will they become paleo banks?

As we navigate the evolving landscape of fintech and neobanks, our syndicated surveys provide a comprehensive understanding of the trends and dynamics shaping financial services. Please get in touch if you’d like more insights from our syndicated surveys.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.