50% of UK consumers now use digital-only providers, yet the Big 6 still hold 84% of primary banking relationships.

What does this mean for the future of banking?

Our recent study of over 4,000 consumers explores the dynamic financial services landscape in the UK. It deep-dives into consumer behaviour around financial services, and importantly their needs and expectations. Our analysis reveals 5 key strategies for banks and fintechs to focus on for success in 2025.

Changing consumer behaviour

Consumers are no longer tied to a single financial services provider and are prepared to shop around for solutions, particularly lending, investments and savings. On average, they now engage with 5.3 financial institutions – up from 4.3 a decade ago. 17% of UK consumers are actively looking for a new bank or would consider switching their main bank account. This trend is even stronger among younger generations, with 20% of Millennials open to switching banks.

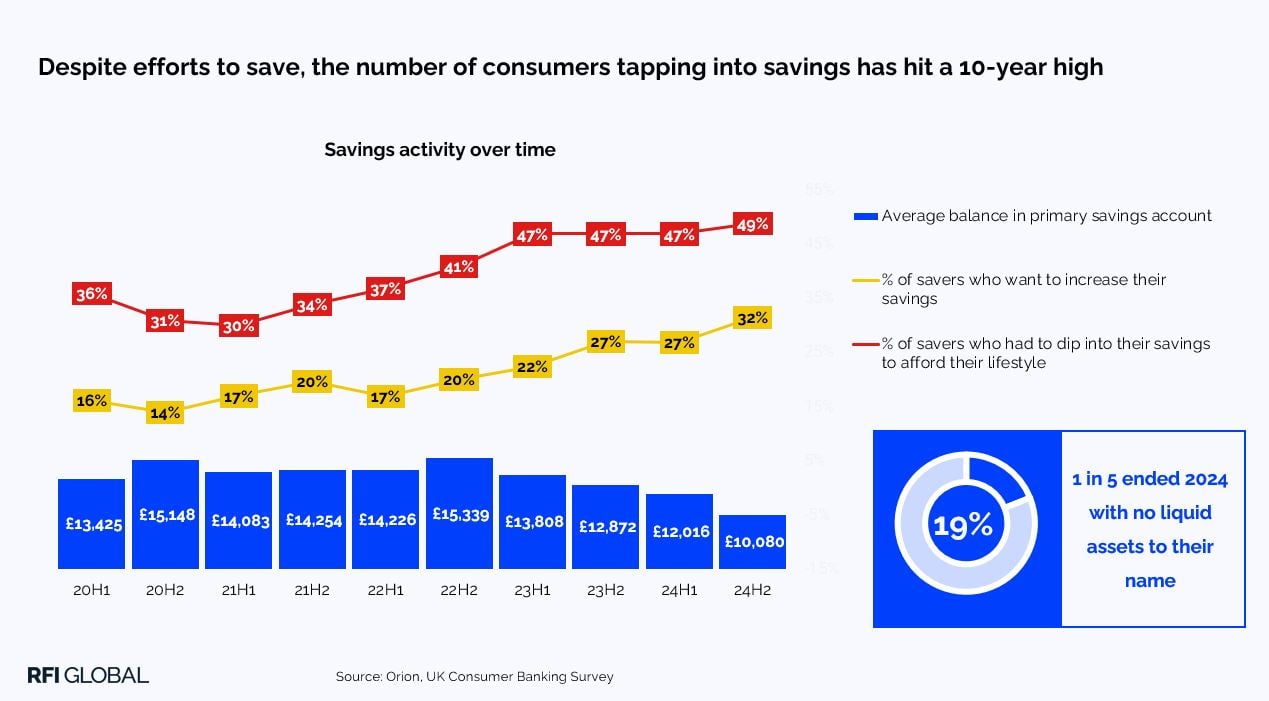

The impact of cost-of-living challenges is impossible to ignore. Four in five consumers say the cost-of-living crisis has changed how they manage and spend their money, and 36% report their financial situation has worsened in the past year.

With regard to savings, 1 in 5 ended 2024 with no liquid assets to their name, and over a third of savers had less than £1,000 to their name.

The battle of banks and fintechs

While the overall penetration of digital-only providers has grown from 16% in 2018 to 50% in 2024, neobanks still only capture 5% of primary banking relationships. Interestingly, 84% of primary banking relationships are still held by one of the Big 6 banks. Neobanks have mostly taken primary customers from tier two and tier three banks.

More affluent consumers and older generations have a wider portfolio and are more likely to hold a smaller share of their liquid assets with the Big 6.

However, the threat of neobanks should not be underestimated. Neobanks have expanded their propositions and deepened engagement with their customers. While traditional banks still dominate, consumers with their main debit card with a neobank spend 20% more than consumers using a Big 6 bank.

Driving innovation and customer experience

Today’s consumers don’t just want digital banking – they expect seamless, fast and intuitive experiences. Half of all banking transactions now take place via mobile apps, and with the rise of digital-only providers, consumers now expect quicker services, including account setup and query handling.

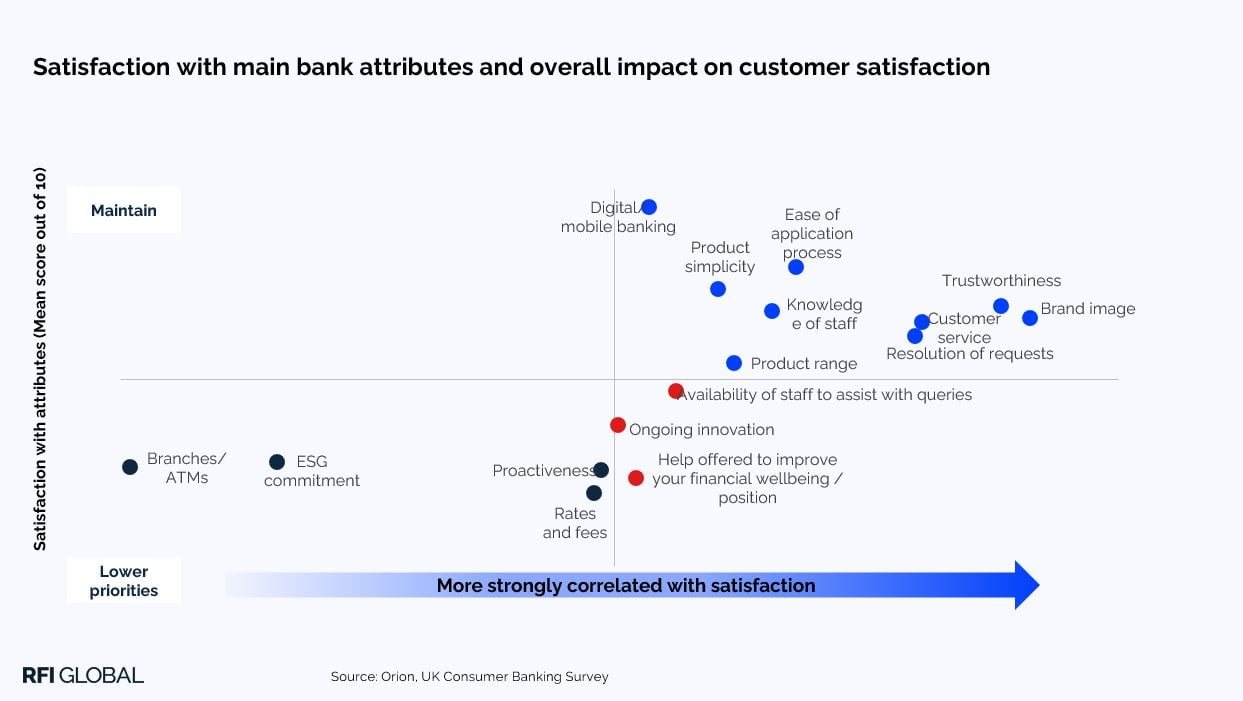

Consumers want banks to maintain a strong focus on ongoing innovation and desire easier access to support for their queries. It is also crucial to highlight the importance of overall assistance from providers in helping consumers improve their financial well-being and position. This support can come from digital-only tools, personal finance management tools, and guidance that enables consumers to better manage their finances.

The importance of rewards

In a world of highly fragmented financial relationships, our Financial Services Trends and Predictions 2025 report emphasises the significance of rewards in winning loyalty as a global trend. Rewards are no longer a ‘nice-to-have’ – they are a decisive factor in customer retention. Today UK consumers are more likely to switch banks for attractive deals and to access rewards such as cash bonuses, interest and other perks. Of those considering switching their main current account in the next 12 months, half (48%) are motivated by incentives or better rewards offered by other providers.

Our data also shows that consumers with rewards linked to their debit or credit cards spend significantly more than those without.

Banks have intensified their efforts to attract consumers with appealing rewards. However, the majority of consumers are dissatisfied with their current rewards proposition. Well-structured rewards programmes deepen existing customer relationships as well as attracting new customers.

Five strategies for banks and fintechs

The banking industry is undergoing a significant transformation, driven by changing consumer behaviours, digital adoption and the increasing appeal of alternative financial providers. From digital-only banks gaining traction to shifting loyalty patterns and the growing role of incentives in decision-making, financial institutions must adapt to these trends to remain competitive.

By focusing on customer experience, innovative offerings and strategic incentives, financial institutions can position themselves for long-term success in an increasingly digital world. The five key areas our consumer data point to are:

1. Adapt to fragmentation

Consumers are diversifying their banking relationships more than ever. On average, they now engage with multiple financial institutions, selecting providers based on the most attractive offerings rather than staying loyal to a single bank. To stay competitive, banks should offer personalised, value-driven experiences across multiple products and touchpoints.

2. Look beyond current accounts

While the Big 6 banks still dominate primary banking relationships, consumers are actively shopping around for other financial products like lending, investments and savings. To capture a greater share of wallets, banks and fintechs must ensure they offer a broad, competitive suite of products tailored to evolving customer needs.

3. Prioritise seamless, mobile-first experiences

The demand for quick, intuitive and frictionless banking continues to rise. With half of all banking transactions now via mobile apps, traditional banks must accelerate digital innovation to compete with digital-only providers. A seamless mobile experience is key to customer retention and engagement.

4. Enable smarter money management

Consumers want more than just transactions – they are looking for intelligent tools that help them manage their finances better. AI-driven budgeting, automation and personal finance management tools can strengthen customer engagement and position banks as trusted financial partners.

5. Boost engagement through rewards

Rewards and incentives are powerful drivers of consumer behaviour. With higher switching rates, customers are more likely to move banks for better incentives, cashback offers, or enhanced rewards programs. Financial institutions must refine their rewards strategies to attract, retain and deepen customer relationships.

The future of banking

The banking landscape is evolving rapidly, and traditional financial institutions should rethink their strategies to compete effectively with digital-only providers. By focusing on customer experience, innovative offerings and strategic incentives, banks can position themselves for long-term success in an increasingly digital world.

Watch our on-demand webinar to learn more about these trends, consumer expectations and actionable strategies for financial institutions in 2025.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.