Luke Allchin, Director, North America

Black History Month is a time to reflect on the power of perseverance, ambition, and community and to examine the financial experiences and aspirations shaping Black households today.

Optimism for the next generation, trade-offs for today

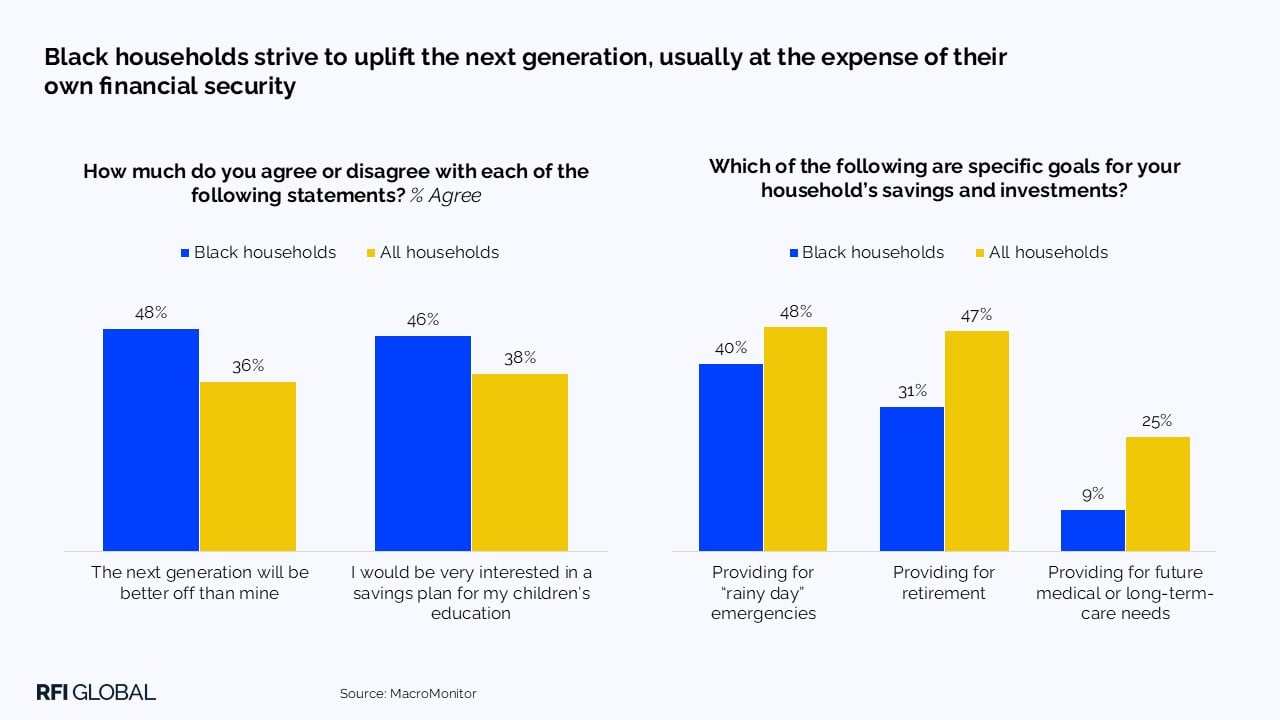

Insights from RFI Global’s MacroMonitor reveal a compelling narrative. In the US, Black households are deeply optimistic about their children’s future yet face persistent challenges that make long-term financial planning more difficult. According to MacroMonitor data, 48% of Black households believe that the next generation will be better off than their generation, compared to an average of 36% among all US households. This optimism reflects how Black families prioritize their financial goals. A greater proportion of Black households express a strong interest in savings plans dedicated to their children’s education, with 46% agreeing that they are very interested in such plans, compared to an average of 38%. Meanwhile, only 31% identify retirement as a key financial goal, significantly below the average of 47%. This focus on the next generation highlights a longstanding cultural emphasis on lifting children to greater heights, even at the expense of securing one’s own retirement readiness.

This commitment to the next generation isn’t new, and our data suggests that while financial circumstances may have changed, the commitment to ensuring children have better opportunities remains a central pillar of financial decision making within Black households. However, when personal financial security is deprioritized, households expose themselves to the risk of vulnerability in later life. This is why access to trusted financial planning resources is critically important to this group.

Balancing frugality with appetite for investment risk

Our MacroMonitor survey also reveals duality in day-to-day financial behavior among Black households. While they are generally more frugal compared to the average household, they are also more willing to embrace financial risk. A significant 88% of Black households indicate plans to spend less over the next year and seek out lower cost financial services, compared to 74% of all households. This heightened focus on cost consciousness reflects broader economic pressures, including income volatility and persistent racial wealth gaps. Yet surprisingly, Black households simultaneously demonstrate a greater appetite for investment risk, with 11% preferring very high risk, very high return investments, nearly three times the rate of the average household.

Despite this appetite, investment participation remains low. Only 9% of Black households own stocks, and 80% hold no securities at all, compared to 18% and 71% on average. This gap suggests not a lack of interest, but a lack of access, support, and trust. The idea of investing is attractive, but the path may feel uncertain or unwelcoming.

This trend demonstrates a powerful insight. Black households are not risk-averse – they are access- and trust-averse. When risk taking feels unsupported, overly complex, or inaccessible, even the most motivated households struggle to translate ambition into action.

The trust gap and the absence of a financial strategy

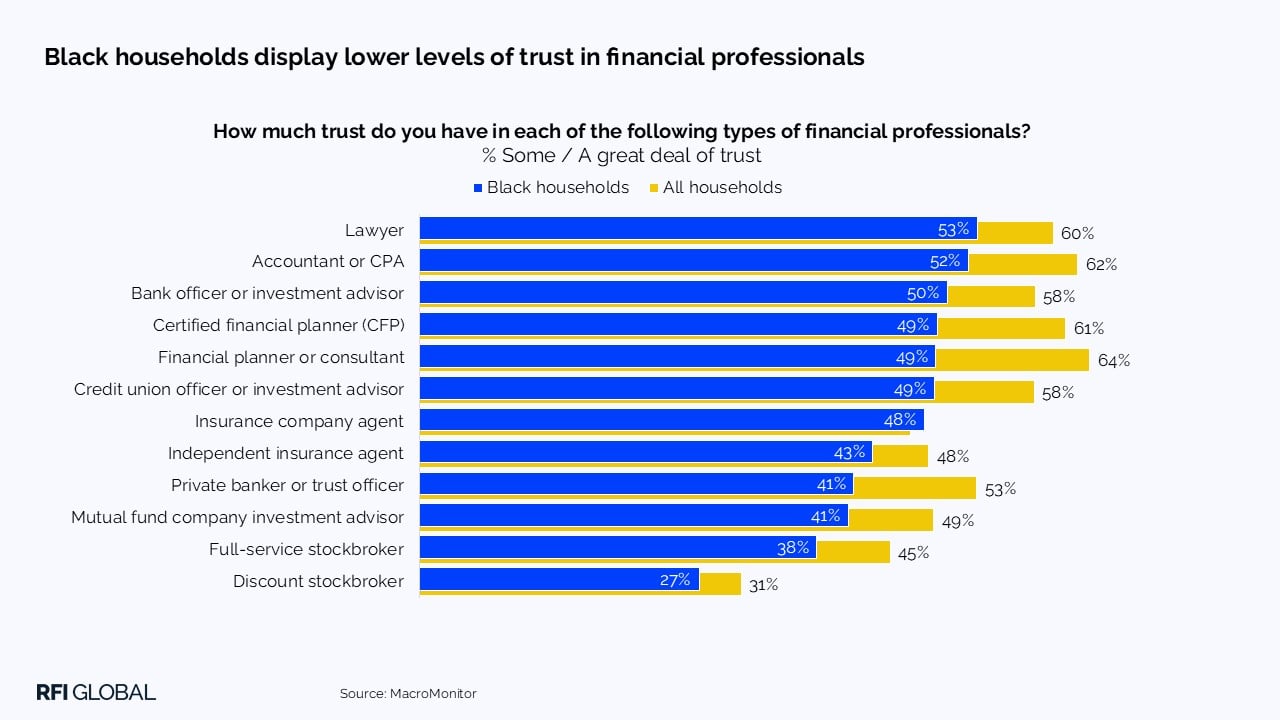

Perhaps the most profound finding from MacroMonitor is the trust gap that shapes the financial behaviors of Black households. More than half (51%) report having no financial strategy, compared to 36% of all households. One third say they never seek financial advice, and only 49% trust certified financial planners, compared to 61% on average. This lack of trust is not surprising. Historically, Black households have encountered discriminatory and systemic exclusion from wealth building opportunities. These experiences have left a lasting imprint on their perceptions of the financial services industry.

The Federal Reserve amplifies this reality, pointing to limited access to banking services, higher rates of financial fraud exposure, and higher fees among Black households, conditions that further strain trust. Without trust, even the best financial products fail to resonate. As a result, households turn inward, relying on family, self-directed research, or basic checking and savings accounts, rather than professional guidance that could accelerate wealth building.

The consequences are significant. Without a financial strategy, households often miss out on long-term tax advantages, compound growth opportunities, and structured planning that ties goals to actionable steps. This lack of planning also increases vulnerability during major life events, including job loss, illness, and retirement.

The digital-in-person paradox

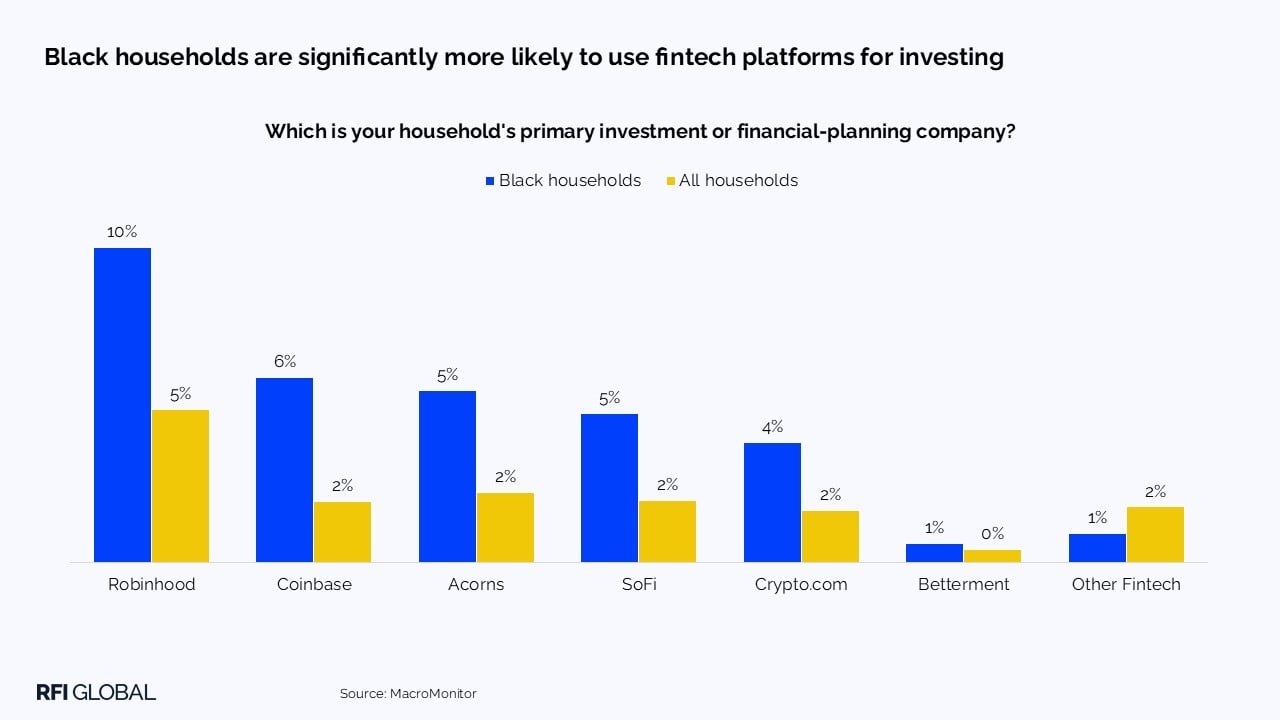

MacroMonitor data highlights a second contradiction: Black households express a strong preference for in person financial interactions, yet many engage more frequently with digital providers than the wider population. 68% of Black households say they prefer to handle financial matters in person, and only 56% feel comfortable completing financial business online, compared to 57% and 68% on average. Despite this preference for face-to-face engagement, Black households are more than twice as likely as the average household to use a fintech platform as their primary investment provider. 31% of Black households consider a fintech (such as Robinhood, Coinbase, or SoFi) as their main investment relationship, far above the 15% of US households overall.

This again reflects an unmet need. Traditional financial institutions have not provided the accessible and trustworthy in-person experiences Black households want. As a result, many turn to fintechs, which offer low barrier digital entry points, simplified user experiences, and fewer perceived judgmental interactions.

A community with aspirations but insufficient support

The overall picture painted by MacroMonitor data is that Black households have clear aspirations but face systemic barriers that limit them in forming long term financial strategies. They want to secure their children’s future, but lack the trusted advisors needed to guide holistic family planning. They are open to risk but lack access to trustworthy investment pathways. They prefer in person support but end up relying on digital solutions because in person experiences have not historically been built with them in mind. This is not a matter of indecision; it is a reflection of long standing structural inequities and unmet needs.

In recent years, several financial institutions have begun to meaningfully address these long-standing gaps by designing products and services that speak directly to the needs of Black households. OneUnited Bank, the nation’s largest Black-owned bank, has taken a leading role by offering financial literacy programs, credit–building tools, and initiatives such as its free online Financial Education Center and the One Transaction program, all aimed at building financial confidence and helping families build generational wealth. OneUnited Bank demonstrates what intentional, equity–focused banking can look like.

The opportunity for financial services providers

The path forward requires intention and investment. Financial institutions have a meaningful opportunity to bridge these gaps if they act with cultural awareness, transparency, and a focus on representation. External research shows this potential is growing. According to a report published by LIMRA last February, Black Americans display a higher level of optimism regarding their financial situation than average and are more likely to believe their situation will improve. This forward-looking sentiment, combined with rising fintech adoption and the ongoing focus on generational uplift, signals a readiness for deeper engagement. Financial services providers that prioritize trust building through representation, clear communication, personalized guidance, and accessible products will be best positioned to support Black households in building wealth.

Ultimately, supporting Black households requires more than products; it requires partnership. Financial institutions must create environments where Black consumers feel seen, heard, and understood. This includes increasing representation within advisory roles, investing in community based financial education, simplifying access to investing and wealth building tools, and designing hybrid service models that blend digital ease with human empathy.

RFI Global’s MacroMonitor data makes one message unmistakably clear: Black households are striving toward a brighter financial future – one centered on generational progress, resilience, and possibility. With the right support and meaningful trust building, they are fully prepared not only to look forward but also to establish the financial legacy they desire. Get in touch to access further analysis from MacroMonitor, the largest survey of US household financial behavior, including detailed insights on Black households and other key consumer segments.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileFrequently Asked Questions on Black American Household Finances

Q: What are the key financial priorities of Black households in the US today?

Black households place a strong emphasis on generational progress, particularly supporting their children’s education and future opportunities. RFI Global’s MacroMonitor shows they are more optimistic about the next generation than US households on average, often prioritising savings for children over retirement planning.

Q: Why do many Black US households lack a formal financial strategy?

More than half of Black US households report having no financial strategy, largely driven by low trust in traditional financial institutions and advisers. Historical exclusion, higher fees, and limited access to trusted guidance continue to shape financial decision-making.

Q: Are Black US households risk-averse when it comes to investing?

No. MacroMonitor data shows Black households are more willing than average to consider high-risk, high-return investments. However, actual investment participation remains low due to barriers around access, trust, and support, rather than a lack of interest.

Q: What can banks and financial providers do to better support Black households in the US?

Financial institutions can close these gaps by building trust through representation, transparent advice, accessible investment pathways, and hybrid service models that combine digital ease with meaningful human engagement.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.