Tiffany Ng, Client Executive, North America

According to MacroMonitor, the largest ongoing study of US household financial behavior, 88% of households now use at least one fintech service. But reach is not the same as relationship. Based on the data, we estimate total US household financial assets at around $72.6 trillion. Investment fintechs hold about $1.5 trillion of that — just 2%. Fintech has the footprint, but reach does not yet equal relationship depth.

For incumbent investment firms, the real question is not whether households are using fintech, but how much of the investment portfolio is at risk over time. Looking across generations, affluence, and customer segments, four drivers stand out.

1. Competition is intensifying first, where digital-first platforms are gaining ground

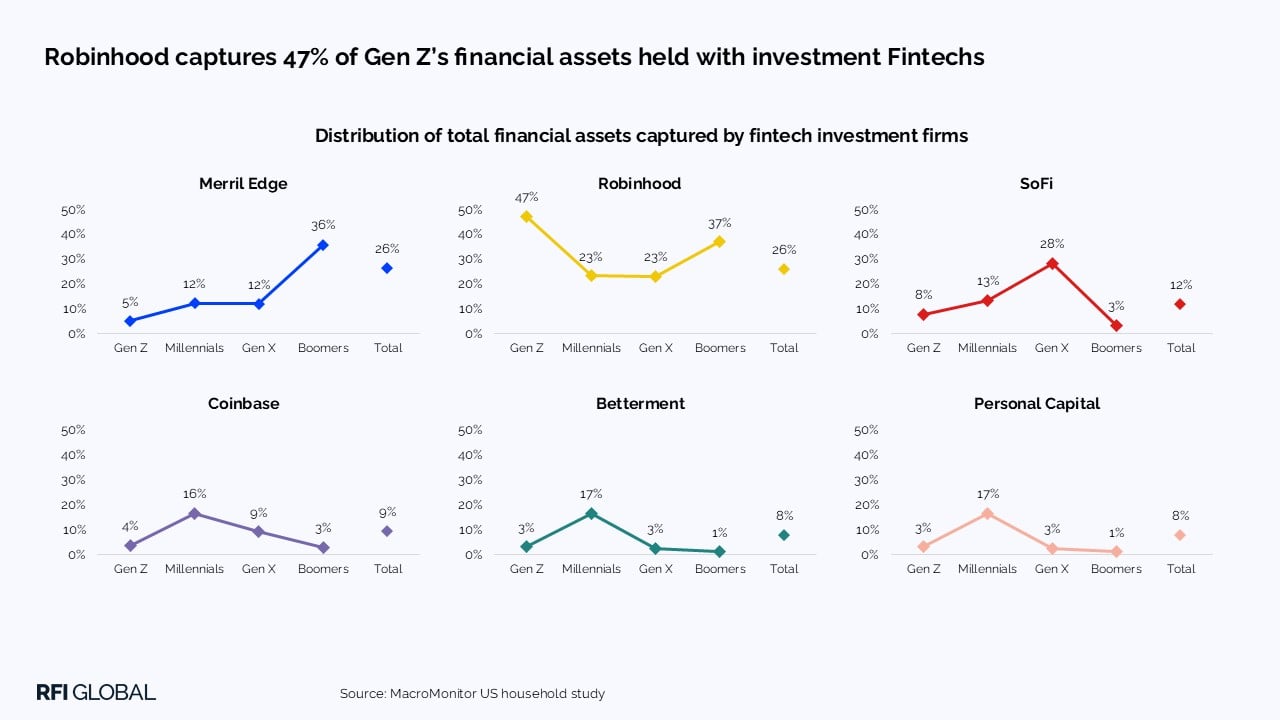

Fintech investing in the US has grown from 2% of households in 2020 to 16% today, but that growth is far from even. A handful of platforms capture a disproportionate share of assets, and the leaders differ sharply by generation. Robinhood dominates with Gen Z (1996-2006), holding 47% of their fintech-invested assets versus 26% across all users. Merrill Edge skews older, capturing 36% among Baby Boomers (1946-1964).

The split reveals wallet share moving at different speeds across segments. Digital-first platforms are pulling ahead with younger, self-directed investors, while established providers hold their ground with older investors, where trust and long-standing relationships still carry weight.

Investment fintech is not reshaping the market uniformly — it is taking hold first in specific segments, particularly among younger investors, who tend to start investing earlier and gravitate towards for digital-first providers that are capturing a larger share of assets.

2. Asset drift is a bigger risk than immediate switching

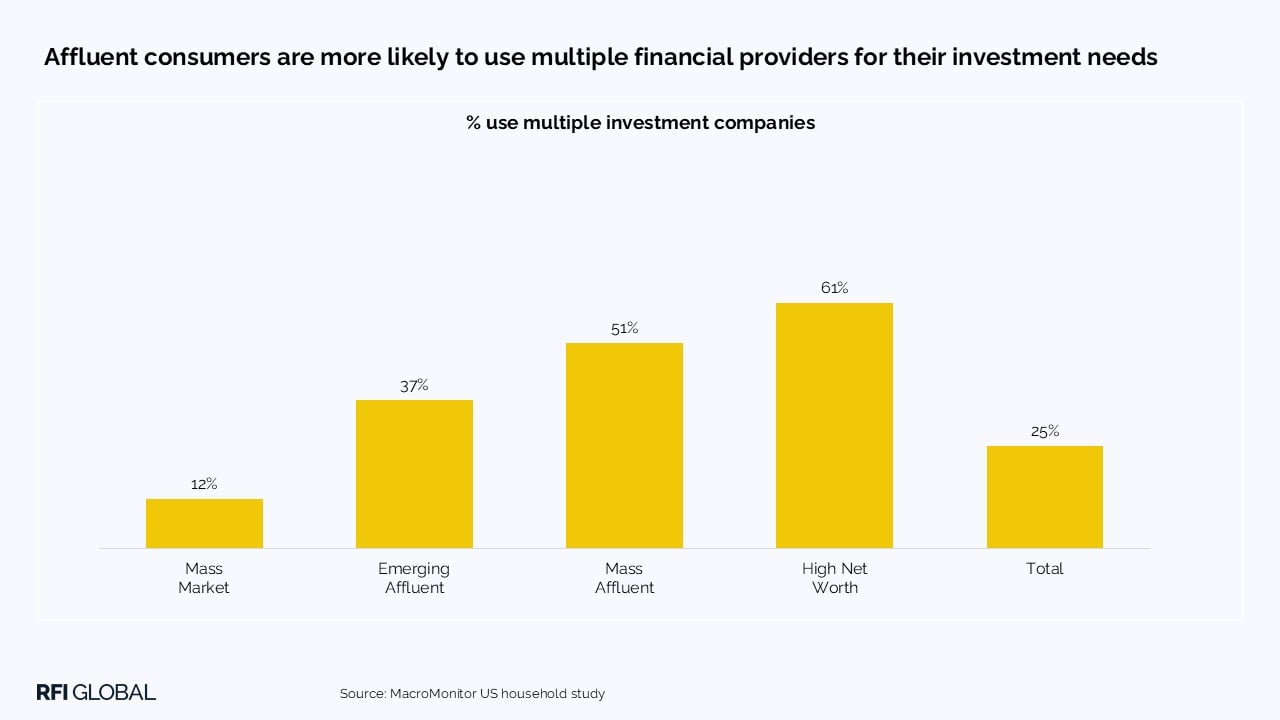

Many investors already spread their assets across multiple providers, and the pattern grows stronger with wealth. While 25% of all households hold accounts at two or more investment companies, that figure rises to 51% among Mass Affluent households ($500k-$3 million in investible assets) and 61% among the High-Net-Worth households (over $3 million).

Yet affluent investors are less likely to switch their primary provider outright. Only 20% of Mass Affluent and 12% of High-Net-Worth households say they are likely to switch, compared to 27% of households overall. Even so, around 45% of both segments say they would still consider alternatives. Performance is the main trigger. 26% of Mass Affluent and 28% of High-Net-Worth households cite poor returns as a reason to switch, compared to 21% households overall.

In practice, affluent investors don’t move quickly, but they are more selective and quicker to act when expectations aren’t met. The real risk isn’t sudden switching, but rather a gradual drift as portions of portfolios are reallocated to other providers over time.

3. Segments are turning to fintech for different reasons

For some segments, fintech is already the primary investment relationship. In related article, Black History Month: A community with big aspirations, but insufficient support from banks, 31% of Black households name a fintech platform as their primary provider, compared to 15% overall. That suggests that fintech isn’t just preferred in these cases; it’s filling gaps where traditional providers have fallen short on access, relevance, or support. Asian households show a different pattern. Adoption here appears driven less by unmet needs and more by alignment with digital behavior: 32% use fintech investment services and 16% use robo-advisors, both well above the overall market. Digital engagement runs deep: 70% of Asian households have made deposits online, and nearly half have bought or sold investments digitally. Higher trust in robo-advisors (34% versus 20% overall) reinforces that these tools aren’t just used, they’re trusted.

The outcome is similar across both segments: fintech becomes central to the investment relationship. But the reasons differ, which means firms need to respond differently across segments rather than relying on a single approach.

4. Digital experience is a baseline, not a differentiator

Customer expectations are shifting in ways that favor digital-first providers.

Trust in neobanks has risen from 25% in 2022 to 34% in the US in 2024, reflecting growing comfort with digital-first financial services. Neobanks aren’t investment platforms, but the shift points to a broader openness to managing money digitally.

The same trend shows up in investing. Trust in robo-advisors has climbed from 18% to 26% over the same period, signaling greater willingness to lean on digital tools for investment decisions.

For investment firms, this changes the basis of competition. Digital experience is no longer a differentiator — it’s the minimum entry requirement. Firms that fall short risk losing engagement simply by failing to keep up.

What does this mean for retail investment firms?

Fintech isn’t redefining retail investing overnight. But wallet share is shifting, competition is becoming more segmented, and customer expectations are evolving toward digital-first experiences. The challenge is no longer just acquiring accounts. It’s capturing a larger share of assets and activity in a market where customers are increasingly comfortable spreading their business across multiple providers.

That means competing on more than brand or product breadth. It means strengthening positioning in the segments where wallet share is already shifting, especially among younger investors. It means staying relevant with affluent households that already diversify across providers. And it means recognizing that for some segments, digital platforms aren’t an alternative to them — they’re already the primary relationship.

The opportunity remains significant: the vast majority of household assets are still not held with fintech investment companies. The firms that sharpen their digital capabilities, align with shifting customer behavior, and compete effectively across segments will be best positioned to retain, and more importantly, grow their share of the relationship.

These insights come from MacroMonitor, the largest ongoing survey of US households. To explore how households are navigating housing, investing, and financial stress in more depth, get in touch to access insights from the full dataset and subscribe to our newsletter for regular, evidence-based insights.

Tiffany Ng

Client Executive, North America

Tiffany Ng is a Client Executive at RFI Global, supporting financial institutions across North America.

View full profileFrequently Asked Questions

Q: What percentage of US households use fintech services?

According to MacroMonitor, 88% of US households now use at least one fintech service. This shows fintech has reached mainstream adoption across the US market. However, broad usage does not necessarily mean fintech firms hold the majority of household financial assets.

Q: How much of US household financial assets are held by fintech investment companies?

MacroMonitor data estimates total US household financial assets at approximately $72.6 trillion. Of that, fintech investment companies hold around $1.5 trillion, or 2% of total assets. This suggests fintech has strong customer reach, but still relatively limited investment wallet share.

Q: Are affluent investors at risk of moving assets to other providers?

The article shows affluent households are less likely to switch their primary investment provider outright, but more likely to use multiple providers and consider alternatives. Among High-Net-Worth households, 61% already hold accounts with two or more investment companies. This means the greater risk is gradual asset drift, where portions of portfolios move over time.

Q: Why is digital experience important for retail investment firms?

Digital experience has become a baseline expectation rather than a competitive differentiator. Rising trust in neobanks and robo-advisors suggests US households are increasingly comfortable managing finances digitally. For retail investment firms, features such as streamlined onboarding, self-directed investing, and always-on access are now expected as standard.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.