Luke Allchin, Director, North America

For years, changes in payments have been described as evolutionary rather than revolutionary. Cards replaced cash, contactless replaced chip and PIN, and mobile wallets quietly layered themselves on top of existing card rails. But our latest data suggests something more fundamental is taking place. Payment preferences in the US are becoming decisively digital, and households are reassessing the value they get from traditional credit cards as cost pressures rise.

Findings from MacroMonitor, RFI Global’s long running study of US household financial behavior, point to a clear shift in how US consumers choose to pay, what they expect from providers, and where traditional card products are starting to lose ground.

This is not the death of the credit card. Far from it. But it is a signal that card providers can no longer assume default status in everyday spending. Value, convenience and perceived fairness increasingly matter more than branding or habit.

Digital payments are no longer niche or optional

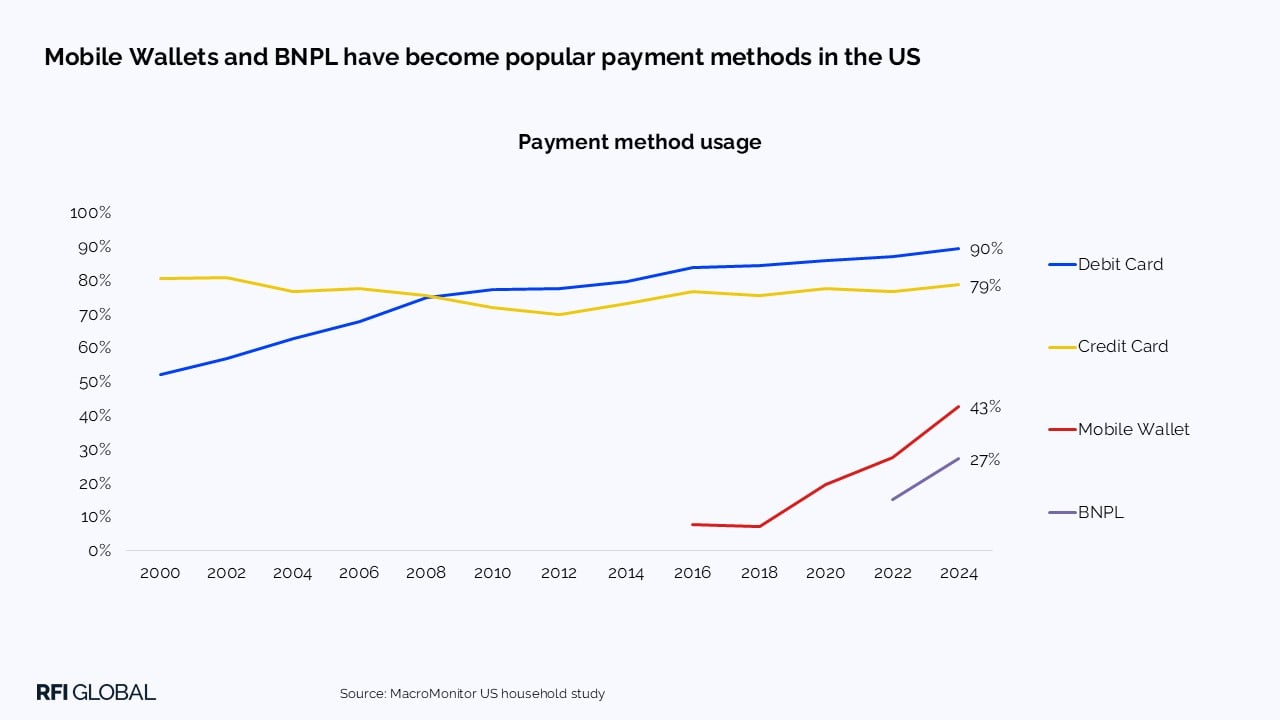

Cash has been declining for years, but the pace of change is now accelerating. Across most everyday payment scenarios, consumers are slowly but steadily turning away from cash, replacing it with digital alternatives. Cards still dominate, but they are no longer the whole story.

Mobile wallets and Buy Now, Pay Later are now firmly established in the mainstream. These tools are not just used for bigger or discretionary purchases. Increasingly, they are part of everyday, low value spending. Households reach for phones rather than wallets, particularly when speed and convenience matter most.

This shift is not uniform across all segments. Mass market households still rely more heavily on cash than affluent consumers, using it across a wider range of scenarios. But even here, cash usage is trending downward year-on-year. The behavioral direction is clear, even if the endpoint looks different across income groups.

What is striking is that this is happening at the same time households report becoming more disciplined about spending and saving. Consumers may be more budget conscious, but they are not retreating into cash. Instead, they are choosing digital payment methods that feel more controllable, more transparent, or simply easier to use.

Credit cards remain central, but pressure is building

Credit cards continue to sit at the heart of household finances. Usage exceeds debit, especially among Millennials and Mass Affluent consumers, and monthly spend through credit cards remains vast. In a typical month, around $240 billion flows through personal credit cards in the US, underscoring just how critical they remain to the payment ecosystem.

But beneath the headline numbers, cracks are starting to appear.

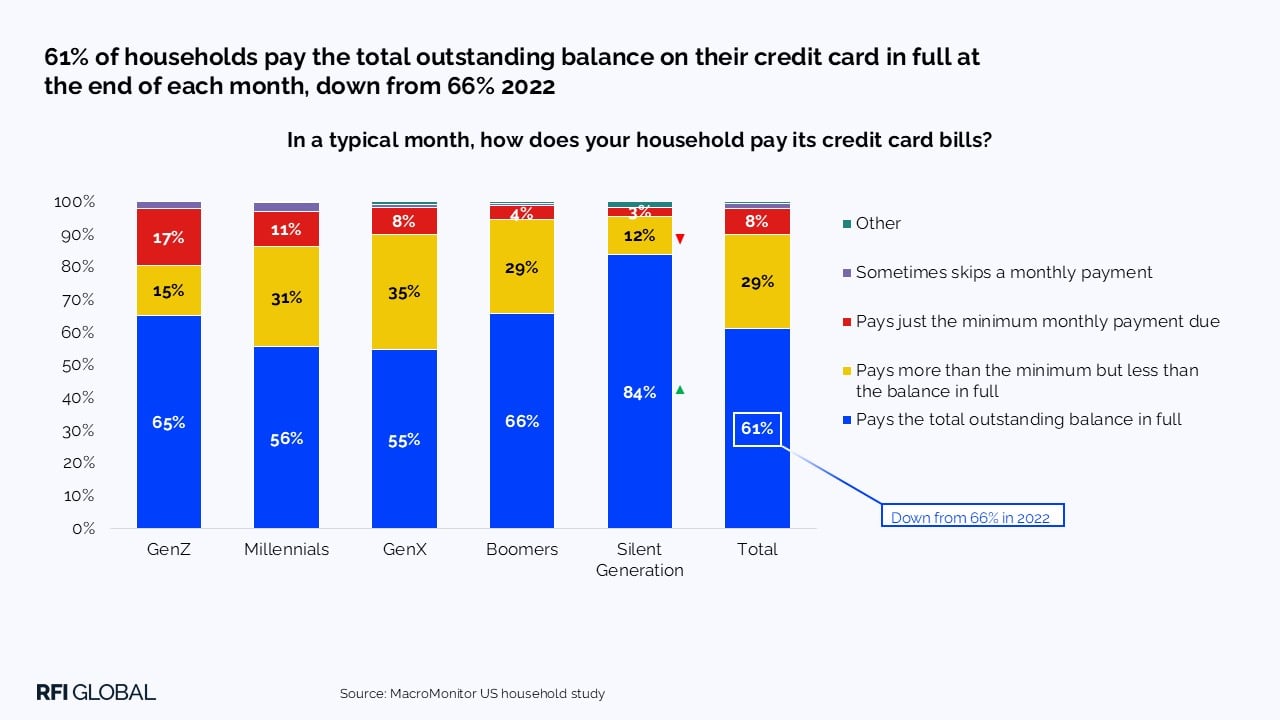

The proportion of households paying their credit card balance in full has declined since 2022. Today, just over six in ten households do so. At the same time, around one in four say they carry more credit card debt than they did a year ago, and one in five have revolved a balance at least once in the past 12 months. Financial pressure is not evenly distributed, with households with children seeing the sharpest increase.

This matters because it changes how consumers think about credit cards. A tool that once felt flexible and rewarding can quickly feel punishing when balances rise and interest costs become more visible. As pressure builds, sensitivity to credit card pricing becomes more prevalent in the market.

MacroMonitor shows this clearly. Annual fees, interest rates and rewards remain the most important drivers of card choice. Gen X consumers, in particular, place a high premium on 0% balance transfer offers. And when households are asked what would push them to close a card account, a rise in the annual fee tops the list by a wide margin.

This is a warning sign for issuers relying on inertia or brand loyalty. Consumers are paying attention, and they are increasingly willing to walk away when perceived value deteriorates.

Why BNPL is resonating with households today

Buy Now, Pay Later sits at an interesting intersection of this shift. Awareness has grown rapidly, with close to six in ten households now familiar with the concept, up significantly compared with just a few years ago. Usage is not only growing among younger consumers, but also among older households, particularly those approaching retirement.

BNPL is often framed as a Millennial product, but our data suggests something broader is happening. While Millennials still hold the most favorable views, older segments are adopting BNPL at pace, often for pragmatic reasons tied to budgeting and cash flow management.

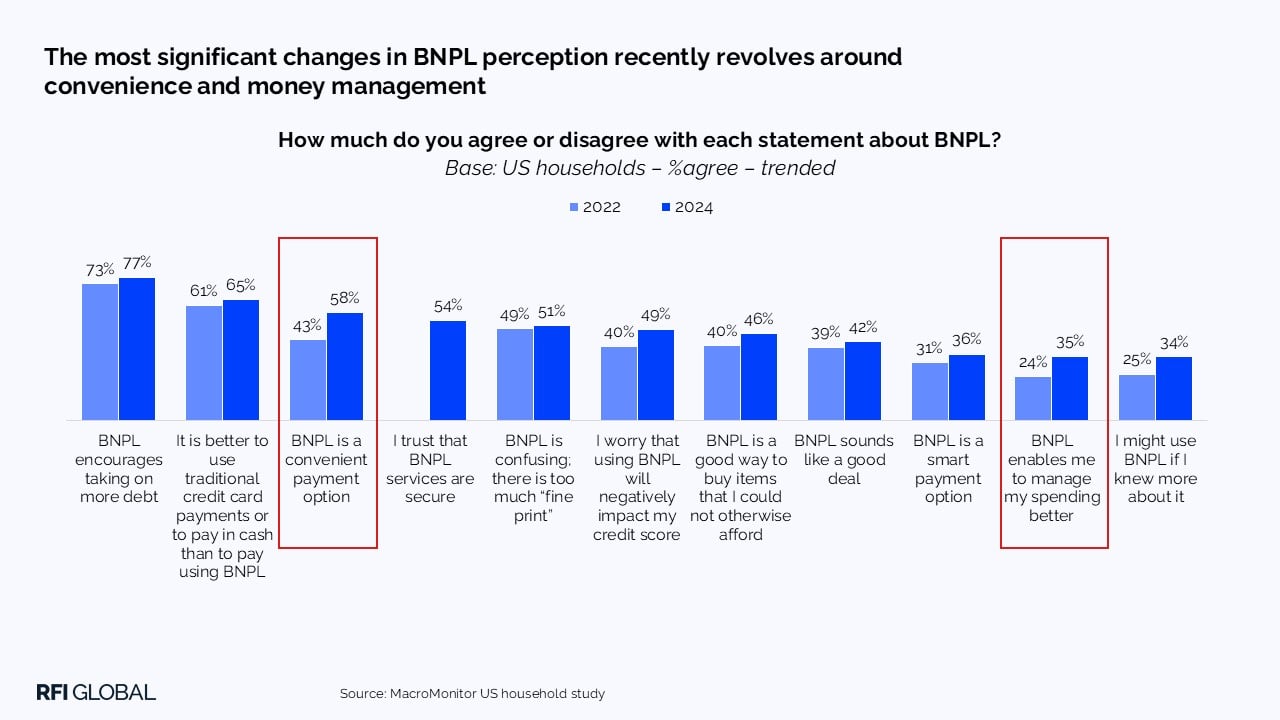

Providers like Affirm, Klarna and PayPal are the most widely recognized, but Afterpay punches above its weight in usage, second only to Affirm. That said, BNPL still has work to do. Non users tend to find it confusing and worry about the potential impact on credit scores. These concerns remain one of the biggest barriers to broader adoption.

Yet perspectives are evolving. The biggest recent shifts in BNPL perception center on convenience and money management rather than novelty. For some households, BNPL feels less like debt and more like a structured way to stay in control of spending. Compared to revolving credit, it can feel predictable, bounded, and easy to understand. In an environment where households are fee sensitive and wary of hidden costs, that positioning matters.

Peer-to-peer payments reinforce the move away from traditional solutions

Peer to peer (P2P) payments add another layer to the digital story. Usage has risen greatly over the past few years, reaching around 80% of US households in 2024, up from just over half in 2020.

Venmo remains the most widely used platform overall, driven by strong adoption among Gen Z and Millennials. Zelle, meanwhile, is growing at the fastest rate, particularly among Gen X and Boomer households. The generational split is clear, but so is the direction of travel.

As P2P becomes habitual, expectations around ease and zero fee transfers harden. These experiences shape how consumers judge other payment products, including cards. When money can move instantly, at no visible cost, tolerance for friction decreases elsewhere.

What this means for card providers

Together, these trends place card providers at a strategic crossroads. Credit cards are not disappearing, but they are increasingly competing with digital alternatives that consumers feel are simpler, cheaper and more transparent. Mobile wallets and BNPL benefit directly from rising fee sensitivity and concern around revolving balances. They are not replacing cards entirely, but they are capturing incremental usage that once defaulted to credit.

To compete effectively, card providers must reinforce their value proposition in meaningful ways. Rewards alone are no longer enough if fees feel unjustified or unclear. Consumers are demanding clarity, flexibility and tangible benefits that align with how they spend.

Segmentation matters more than ever. Millennials and Mass Affluent households remain heavy credit users, but they are also among the most enthusiastic adopters of mobile wallets, BNPL and digital P2P services. Mass market households still use cash more widely, but they are not immune to digital adoption. A single, one size fits all payment strategy will miss these nuances.

Providers that align card products with digital behaviors will be better placed to defend relevance. That means seamless wallet integration, clearer messaging around cost and value, and a clearer focus on how credit supports everyday financial management rather than simply encouraging spending.

The payments landscape has become more competitive, more transparent and less forgiving. The direction of travel is digital, and households are voting with their behavior. There is still time for card providers to adapt, but those that rely on habit may find loyalty eroding faster than expected.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileFrequently Asked Questions

Q: How are payment preferences changing in the US?

US payment preferences are becoming increasingly digital. While cards remain the dominant payment method, households are using mobile wallets, Buy Now, Pay Later (BNPL) and peer-to-peer (P2P) payment platforms more frequently for everyday spending. The shift suggests digital payments are moving from optional alternatives to mainstream consumer behavior.

Q: Are credit cards losing relevance in the US?

Credit cards remain central to household finances and continue to account for significant monthly spend. However, RFI Global data shows their default status is under pressure. Rising sensitivity to annual fees, interest rates and perceived value means consumers are becoming more willing to switch or close accounts when benefits no longer justify costs.

Q: Why is Buy Now, Pay Later growing in the US?

BNPL is growing because many consumers see it as a simpler and more predictable way to manage spending. The article highlights that adoption is expanding beyond younger consumers, with older households also using BNPL for budgeting and cash flow management. Convenience and payment control are key drivers of growth.

Q: What do US payment trends mean for banks and card issuers?

US payment trends indicate banks and card issuers need to compete on value, transparency and digital experience. Rewards are important but alone may no longer be enough. Providers should focus on clear pricing, seamless mobile wallet integration, flexible payment solutions and products that support everyday financial management.

Q: What is driving demand for peer-to-peer payments in the US?

P2P payment adoption has risen strongly because consumers value instant transfers, ease of use and low or no visible fees. As services such as Venmo and Zelle become habitual, they are also defining expectations for speed and convenience across the wider payments market.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.