Jackie Greig, VP Marketing, Global

Customer loyalty in retail banking is being tested like never before. Fragmented relationships, intensifying competition from digital-only providers, and rising expectations for more personalised, technology-led engagement are redefining what it means to be a customer’s ‘main bank’.

At the same time, consumers are navigating a prolonged period of economic pressure. While they can’t control inflation, interest rate policy or the rising cost of essentials, they can act in the areas they can control. This is driving a more active reassessment of financial relationships, with customers increasingly willing to manage multiple providers and reconsider long-standing banking choices.

In this environment, switching is no longer exceptional behaviour – it is becoming a rational response to choice, price pressure and perceived value. Consumers are actively seeking better returns, lower costs and clearer evidence that their loyalty is recognised.

Against this backdrop, rewards and loyalty programmes are becoming one of the most effective levers available to banks. Once largely associated with credit cards, rewards are now embedded within the core current account relationship, shaping both acquisition and retention strategies across global markets.

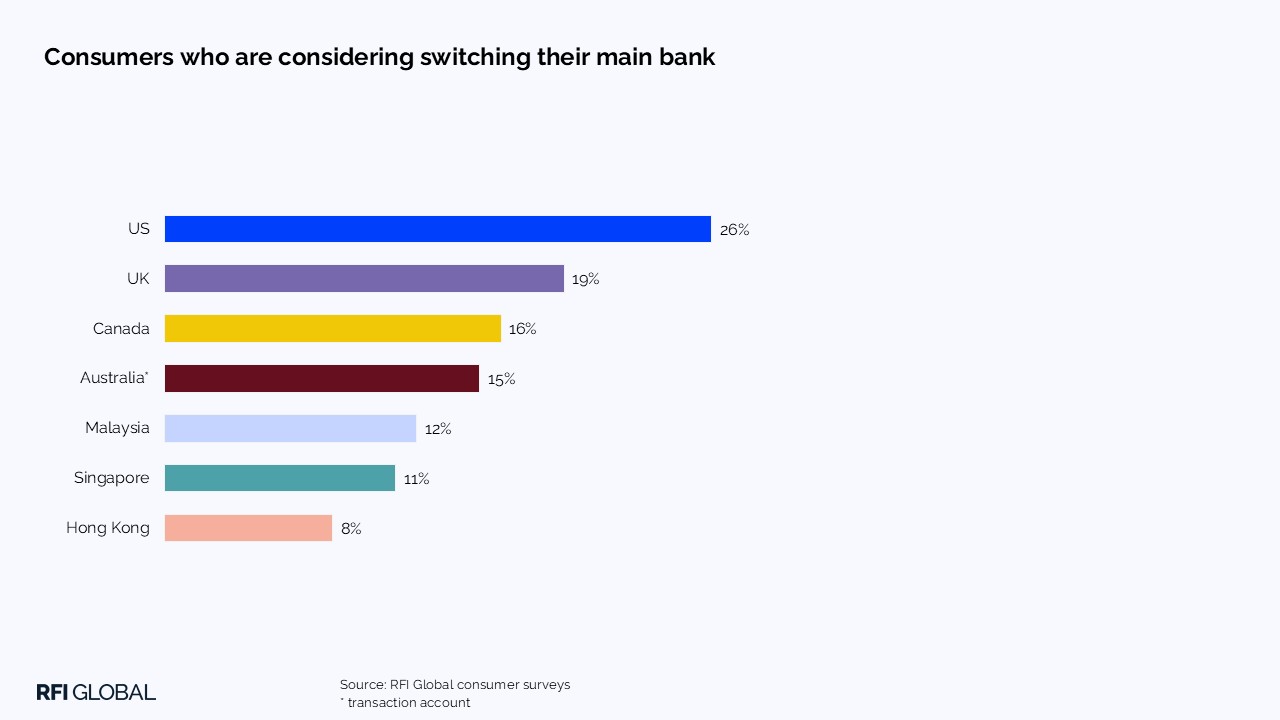

Switching rates are significant – and different by market and generation

RFI Global data shows that switching intentions for main bank relationships are significant across markets, though the scale varies by geography. In the US, more than a quarter of households (26%) report they intend to switch their primary bank within the next 12 months. This falls to just under one in five in the UK (19%), and 16% in Canada. APAC consumers are the least likely to switch.

Younger generations, particularly Gen Z and Millennials, are more likely than older cohorts to switch. They are more digitally engaged, more comfortable managing multiple financial relationships and less anchored to legacy institutions. In contrast, Boomers and the Silent Generation are less likely to switch, showing a stronger attachment to existing providers.

As younger cohorts enter their peak earning and borrowing years, banks will need to compete more actively for relevance and engagement for these digitally native, value-sensitive customers.

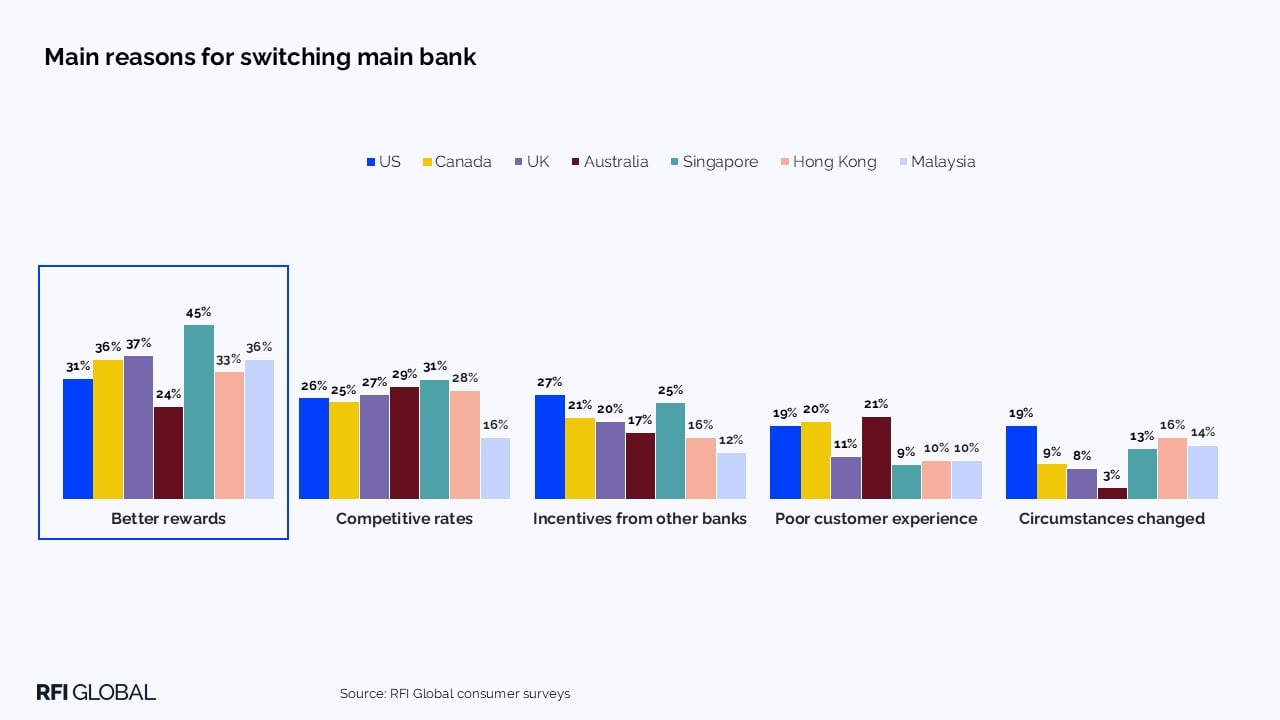

Rewards: a primary trigger for switching behaviour

While competitive interest rates remain a critical factor in banking decisions globally, rewards programmes have emerged as a powerful motivator among those actively considering switching.

Across markets, between a quarter and nearly half of intending switchers cite rewards as a main reason for changing their main bank account. This positions rewards ahead of many traditional drivers like rates and customer experience.

This dynamic reflects a broader behavioural shift. Rather than absorbing higher costs, consumers seek rates, better value and more personalised rewards.

There are, however, important market nuances. In Australia, consumers are less likely than in other regions to select a bank product primarily based on rewards, but not feeling rewarded for loyalty is typically one of the key reasons to switch for specific products.

In the UK, rewards are a strong motivator for affluent customers: 43% of affluent consumers considering switching cite rewards as a key factor. In Singapore, by contrast, the figure is lower at 27%, reflecting different expectations of service, benefits and financial value across markets.

Older consumers, particularly Boomers and the Silent Generation, are the least likely to switch on the basis of rewards. Their relationships are often built on trust, inertia and historical engagement. For younger cohorts, however, rewards act as both a rational incentive and a signal of how much a bank values their custom.

From acquisition to retention: rewards as a loyalty lever

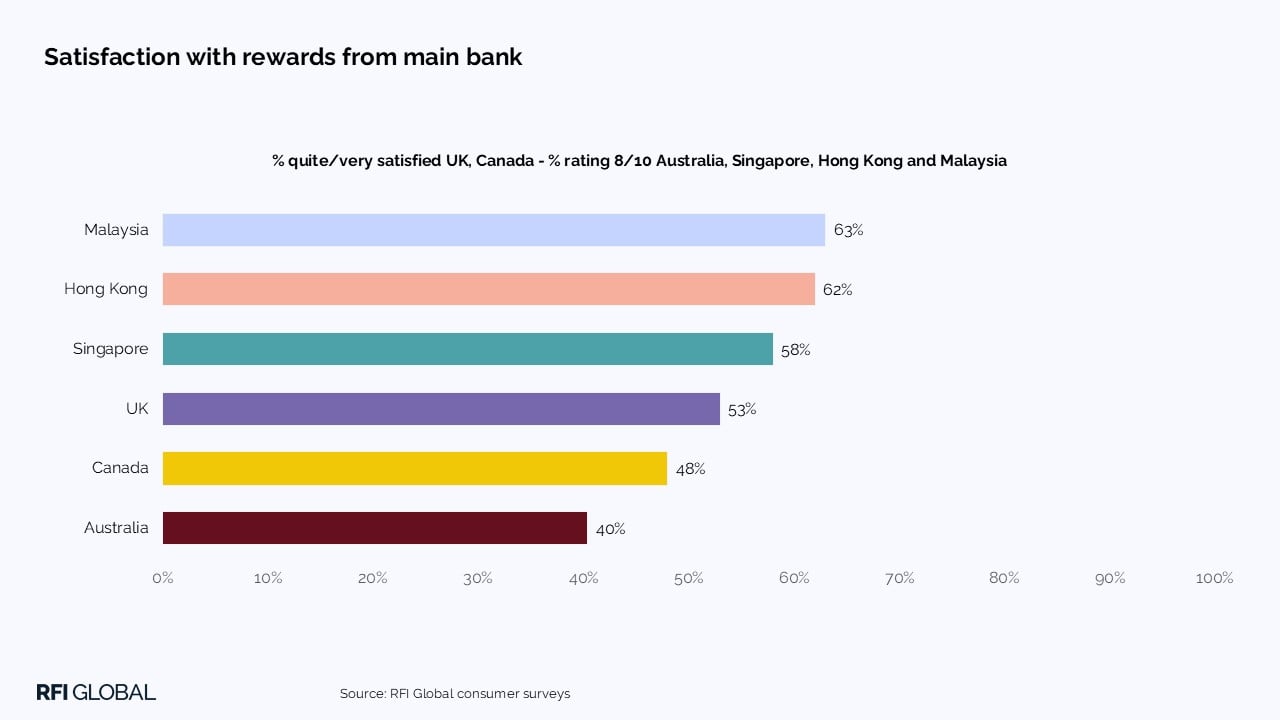

While rewards are highly effective at attracting intending switchers, their impact doesn’t stop at acquisition; they are also shaping perceptions of value, satisfaction and advocacy.

Satisfaction with rewards varies significantly by market. Levels are high across APAC markets, while lower satisfaction in the UK, Canada and Australia points to untapped potential. In markets where rewards have historically been peripheral to current accounts, banks face a growing opportunity – and risk – as customer expectations evolve.

In APAC, rewards and loyalty programmes consistently emerge as a key driver of recommendation among retail banking customers. At the same time, they are also identified as a major pain point when they fall short – alongside competitiveness of rates and fees, clarity of product offerings, and transparency around pricing and terms. This dual role underscores the strategic importance of execution: rewards programmes that are well-designed can materially enhance loyalty, while poorly implemented schemes can actively undermine it.

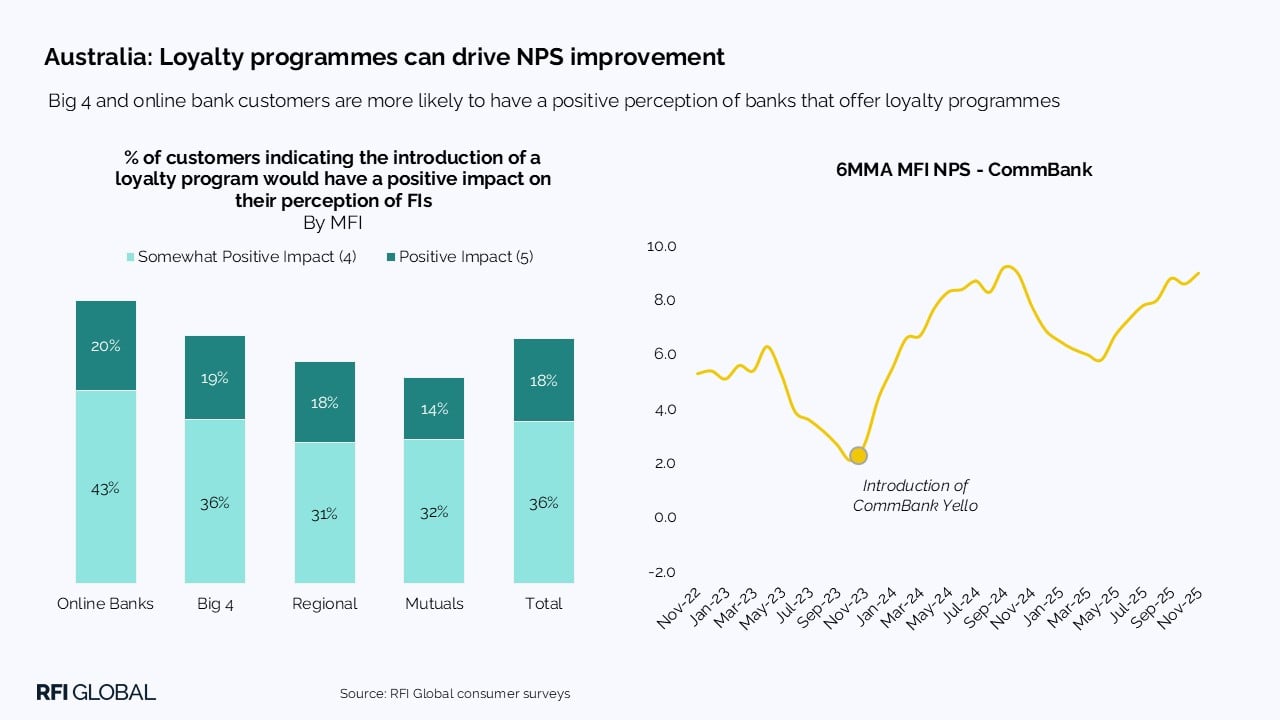

Australia provides a clear illustration of this effect. More than half of retail banking customers (56%) agree that loyalty programmes would have a positive impact on their perception of their bank. And rewards programmes have a more positive impact amongst online and digital-first banks users. Rewards are being used not only as a marketing tool but as a key customer retention strategy.

What ‘good’ looks like: best practice in rewards

The most effective rewards programmes share several characteristics: they are easy to access, offer clear value, personal relevance and are integrated into everyday banking behaviour. Increasingly, leading institutions are moving beyond simple transactional incentives such as points and cashback, towards experience-led and usage-based engagement.

Australia: CommBank Yello

Launched in October 2023, CommBank Yello embeds rewards into everyday banking through cashback, personalised discounts and prize draws for active customers. Benefits scale with engagement, encouraging deeper product usage via a tiered structure. RFI Global data shows customers feel greater recognition of loyalty since launch, and Yello has supported higher Net Promoter Scores for Commonwealth Bank, demonstrating the impact of frictionless, value-led rewards on advocacy – see chart above.

UK: Nationwide

Nationwide’s rewards proposition integrates rewards into the core banking relationship, offering cashback, interest enhancements, bundled services and ‘thank you’ payments for eligible members. Rather than acting as short-term incentives, these benefits reinforce long-term engagement. RFI Global data shows that Nationwide outperforms the market on satisfaction, with 63% of customers reporting strong satisfaction with rewards versus 53% across the total market. This highlights the effectiveness of loyalty-led relationship strategies.

US: Chase

Chase’s Ultimate Rewards programme offers flexible points redeemable across travel, dining, technology and statement credits, with the ability to transfer to select airline and hotel partners for enhanced value. A built-in shopping portal further differentiates the experience by surfacing retailer offers directly within the Chase platform. Forbes Advisor highlights the programme’s versatility and strong redemption value, particularly for travel. RFI Global survey data also shows that Chase is the most highly regarded US bank for having the best perks, reinforcing the role of rewards in driving satisfaction and loyalty.

Singapore: Citi

Citi delivers one of the most highly rated rewards propositions in Singapore, combining accelerated earn rates with flexible redemption across cashback, travel and lifestyle categories. Products such as the Citi Rewards Card and Citi PremierMiles appeal strongly to affluent, travel-oriented customers. RFI Global data shows 77% of Citibank customers are extremely satisfied with their rewards programme, compared with a market average of 54%, demonstrating clear differentiation through loyalty.

The implications for banks: loyalty as a strategic capability

In this context, rewards and loyalty strategies have become central to consumer decision-making. They now shape not only how customers select a main bank, but how they judge the quality, fairness and value of their ongoing relationship.

However, not all rewards are equal. Well-designed loyalty ecosystems can drive acquisition, deepen engagement and materially improve customer advocacy.

Key principles for best practice:

- Relevance over scale: Personalised, context-aware rewards outperform generic offers.

- Frictionless integration: Rewards must be embedded into everyday banking behaviour, not layered on as an afterthought.

- Recognition of loyalty: Customers increasingly expect tangible acknowledgement of tenure and engagement.

- Commercial sustainability: Merchant partnerships and tiered benefits help balance customer value with cost control.

As competition intensifies and switching remains high, the strategic question for banks is no longer whether to invest in rewards, but how to design them to drive sustainable value. Programmes that are relevant, frictionless and clearly aligned to customer needs will differentiate in an increasingly commoditised market.

Customer loyalty can no longer be assumed; it must be actively earned – through consistent value, meaningful recognition and experiences that reinforce why a bank deserves to remain at the centre of a customer’s financial life.

To stay up to date with data-driven insights from RFI Global’s consumer and business surveys, subscribe to our newsletter or get in touch to explore how we can support your customer strategy.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileFrequently Asked Questions on banking rewards

Q: Why are people switching their main bank account?

People are switching banks more often as they look for better value in a high-cost environment. With more choice and easier switching, consumers are reassessing long-standing relationships and moving providers to access better rates, lower costs and rewards that recognise their loyalty.

Q: Do rewards really influence which bank people choose?

Yes. Rewards are one of the strongest incentives for consumers to switch their main bank. RFI Global data shows that between a quarter and nearly half of consumers considering a switch cite rewards as a key motivator, often ahead of traditional factors such as customer experience.

Q: Are rewards only useful for attracting new customers?

No. While rewards help attract switchers, they also improve retention. Well-designed loyalty programmes increase satisfaction, strengthen advocacy and improve how customers perceive their bank over time.

Q: What makes a banking rewards programme effective?

The most effective programmes are easy to use, clearly valuable and built into everyday banking. Personalised rewards, low friction and meaningful recognition of loyalty matter more than complex points systems.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.