Kieran Hines, Director, EMEA & North America

Talk to anyone across the industry, and it’s clear there’s no shortage of ways for banks to apply AI technologies to better deliver for customers.

Understanding the needs and preferences of the end-user is critical to these discussions, but, when it comes to AI, one area is often overlooked. Unlike other cycles of technology-driven change, such as the impact of the cloud or the adoption of mobile banking, customers don’t need to wait for banks to deliver service enhancements.

This has significant implications for the decisions banks need to make about integrating AI technologies into their product and channel strategies.

AI tools are already part of everyday life

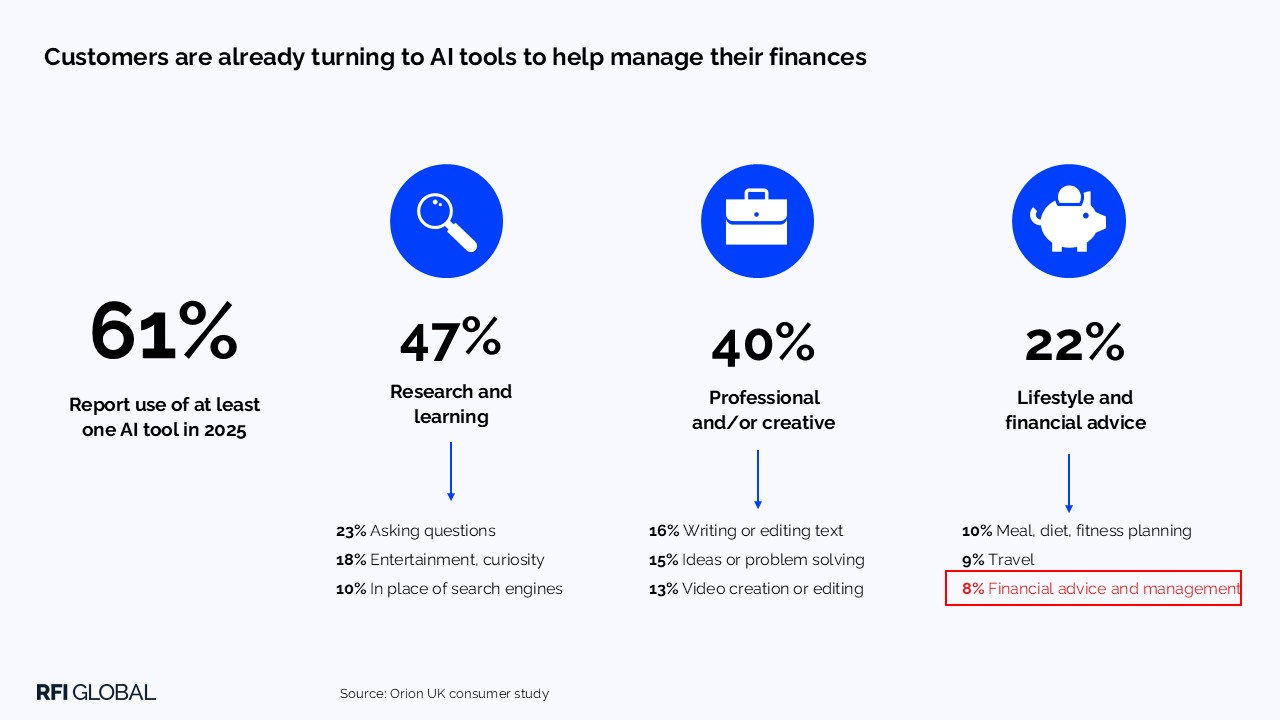

Consumer engagement with AI tools in the UK is widespread. Our latest Orion study, which captures insights from 16,000 UK consumers per year, shows that 61% of adults report having used at least one AI tool, such as ChatGPT, Copilot or Gemini in 2025.

Usage is becoming increasingly sophisticated. While 23% use AI tools for asking simple questions, they are the default search tool for 10%. This in itself has very important implications for the way banks should think about how their products are discovered.

We can also see clear adoption in the workplace. Around one in six adults use AI tools for writing or editing text, and a similar proportion uses them for other work related tasks. This matters because it accelerates familiarity and trust. As AI becomes normalised in professional life, it accelerates adoption in other domains.

A meaningful shift for financial institutions

One of the most striking findings from our recent consumer data is the number of consumers using AI tools for financial purposes, with 8% of UK adults using AI tools for financial advice or support in 2025.

This tells us two things. First, there is a clear appetite among consumers for conversational, AI driven interfaces when it comes to financial questions. Second, this behaviour exists largely outside of traditional banking propositions today, highlighting clear unmet demand.

Understanding demand opportunities

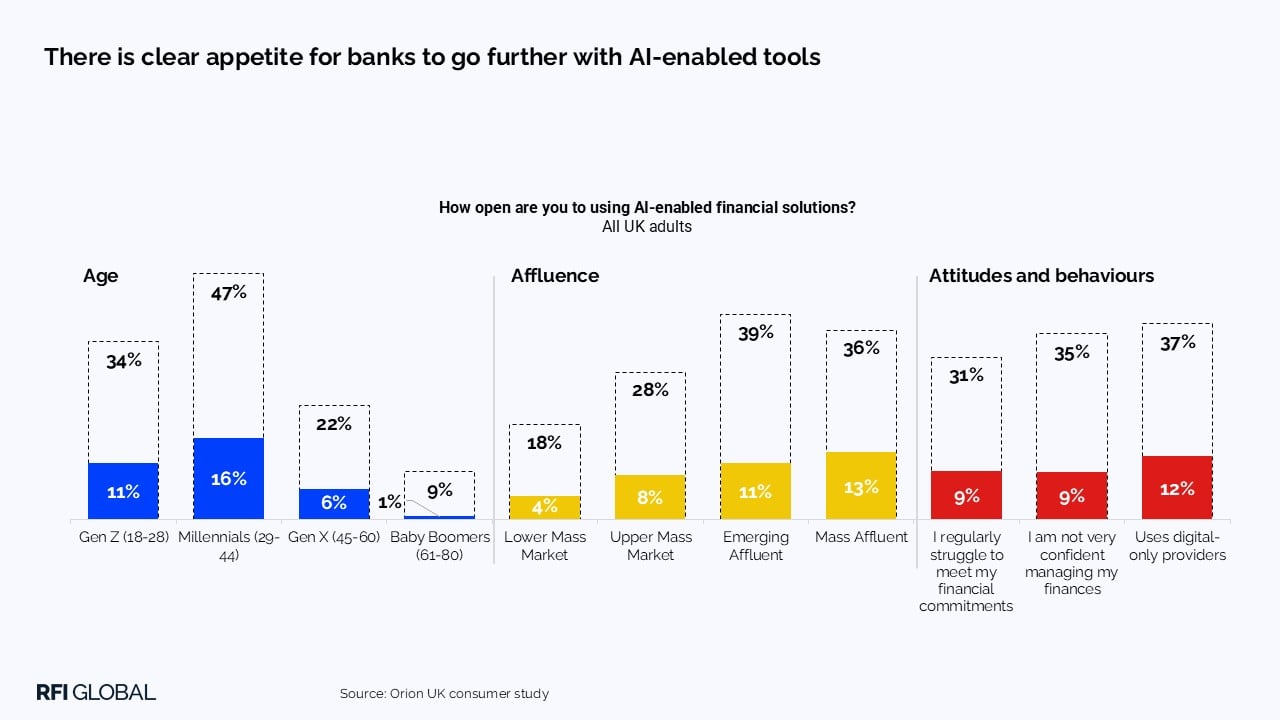

Digging deeper into who is using AI tools for financial management reveals some important nuances. Usage skews younger, with higher engagement among 18–44-year-olds. That is not surprising, but it reinforces the need to be bold in designing and launching new product features to fully meet the expectations of these users.

More interesting still is the relationship with affluence. Use of AI tools for personal financial management increases as consumers become wealthier. This is partly about professional exposure, but it also highlights a long standing gap in the market: scalable, high quality, personalised financial advice that sits between mass market banking and full service wealth management.

At the same time, consumers who struggle with managing their finances are also turning to AI tools. In other words, the same technology is being used by very different customer segments, with very different needs. That creates opportunity, but also complexity. One size fits all propositions will not work.

The latent demand for AI-driven interfaces

Perhaps the clearest signal for banks comes from comparing current usage of AI tools with stated interest in AI enabled financial services. Across every demographic segment, consumer appetite is significantly higher than actual usage.

Our data shows that around 29% of UK banking customers say they are interested in AI enabled financial solutions, compared to the 8% currently using it. When applied to the UK population, that equates to almost 16 million people. In each segment, the proportion open to using AI powered banking tools is roughly three times larger than the proportion already using generic AI tools for finance.

The implication is straightforward. Consumers are not waiting for banks to ‘invent’ the demand; they are waiting for credible, trusted financial providers to bring AI capabilities into products and services in a visible and useful way. If banks do not do this, some customers will inevitably look elsewhere.

That said, it is equally important to recognise that the majority of consumers are not there yet. This is an area that will move quickly, and banks should target early adopters while building scalable foundations for the future.

People want AI to be used to solve problems, not gimmicks

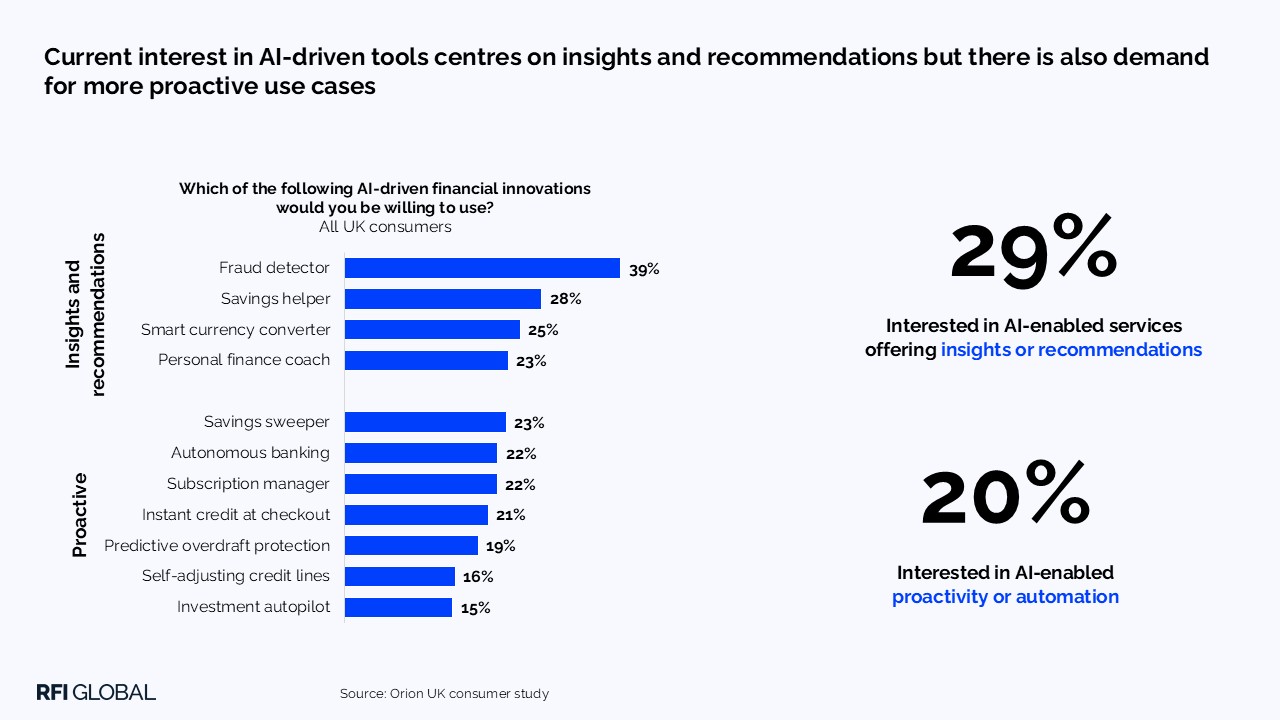

The big takeaway for the industry is that there’s no silver bullet; customers are looking for improvements across a wide range of areas. Concern around fraud and scam risks has surfaced in a demand for stronger customer-facing support around fraud detection, while better support around building deposits and broader finance coaching are also high on the list. These are familiar concepts, but AI has the potential to make them more timely, contextual, and personalised.

What is changing faster than many expect is customer openness to more proactive and action oriented use cases. More than one in five customers is already comfortable with some level of automation, particularly in areas such as savings, payments and subscription management. This appetite is even stronger among those who lack confidence in managing their finances.

There is a reinforcing dynamic at work here. The more comfortable customers become with AI tools in general, the more receptive they are to automation within banking. Over time, this points towards a pivot from recommendation led services to more agent-led proactive service models.

How financial institutions can capture the AI opportunity

The pace of change we’ve seen to date suggests we may reach this point more quickly than many in the industry expect.

For banks, the message is clear.

Customers are more ready for AI-led services and experiences than you realise. Moving quickly to embed the functionality and experiences customers want into your digital channels should be a priority. The growing use of GenAI tools for financial advice shows that this is not just a question of digital engagement, but about the risk to deposits and investment balances, both now and in the future.

Institutions that move early to deliver trusted, practical and visible AI-led experiences will be best placed to capture the opportunity.

Get in touch for further insights from our study and how to bridge the AI opportunity gap.

Kieran Hines

Director, EMEA & North America

Kieran Hines is Director at RFI Global, leading research and advisory work across EMEA and North America. He is a senior financial services analyst with deep expertise in retail and business banking, payments and digital transformation.

View full profileFrequently Asked Questions about AI in banking

Q: Are UK consumers open to AI in banking?

RFI Global data shows that 29% of UK banking customers are interested in AI-enabled financial solutions. That equates to around 16 million people in the UK, indicating significant unmet demand for trusted AI-powered banking services.

Q: Are people using AI for financial advice and money management?

Yes. RFI Global research shows that 8% of UK adults already use AI tools for financial advice or support. Usage is higher among younger consumers and increases with affluence, highlighting strong demand among digitally engaged and wealthier segments. At the same time, consumers who lack confidence in managing their finances are also turning to AI tools, showing that demand spans multiple customer groups with different needs.

Q: What AI features do banking customers want most?

Customers are looking for practical AI use cases that improve everyday financial management. Key areas of interest include fraud and scam detection, savings support, financial coaching, payments assistance and subscription management. Demand is strongest where AI can reduce friction and improve confidence.

Q: What are the AI opportunities for banks and financial institutions?

This article highlights that customer demand for AI in banking is significantly ahead of current usage. This creates an opportunity for institutions to build trusted AI-enabled products and services, targeting early adopters while creating scalable foundations for wider future adoption.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.