Tiffany Ng, Client Executive, North America

The caregiving shift

The American population is aging faster than at any point in its history. By 2030, 73 million Americans—21% of the population—will be 65 or older, driving unprecedented demand for care, according to USAFacts. This demographic shift is not just a social story; it is a financial one, and women sit at its center.

Women make up 61% of caregivers, according to a US 2025 AARP Research Report, and they shoulder more unpaid care than men. In 2023, women spent an average of 6.7 hours per day on unpaid caregiving for children or older adults, compared with 5.6 hours for men. These hours represent lost wages, diminished retirement contributions, slower career progression, and altered financial priorities that compound over time.

My previous article on the Sandwich Generation explored the strain of multigenerational care. Here, the focus goes deeper, examining how caregiving reshapes financial behavior across gender and race, and why banks need a strategy that treats caregiving as a defining force in many women’s financial lives.

The financial ripple effects of caregiving

Caregiving’s financial impact is long-term, measurable, and often underestimated. Data from our MacroMonitor study, the largest survey of US household behavior, reveals clear disparities between male- and female-led households aged 40 to 60—the life stage banks typically model as peak earning years. Half of women-led households in this age group report being one paycheck, illness, or accident away from financial collapse, compared with 44% of men-led households. Anxiety about the future is also pronounced: 66% of women worry about having adequate retirement income, and only 31% feel their savings could cover an illness or disability, versus 41% of men.

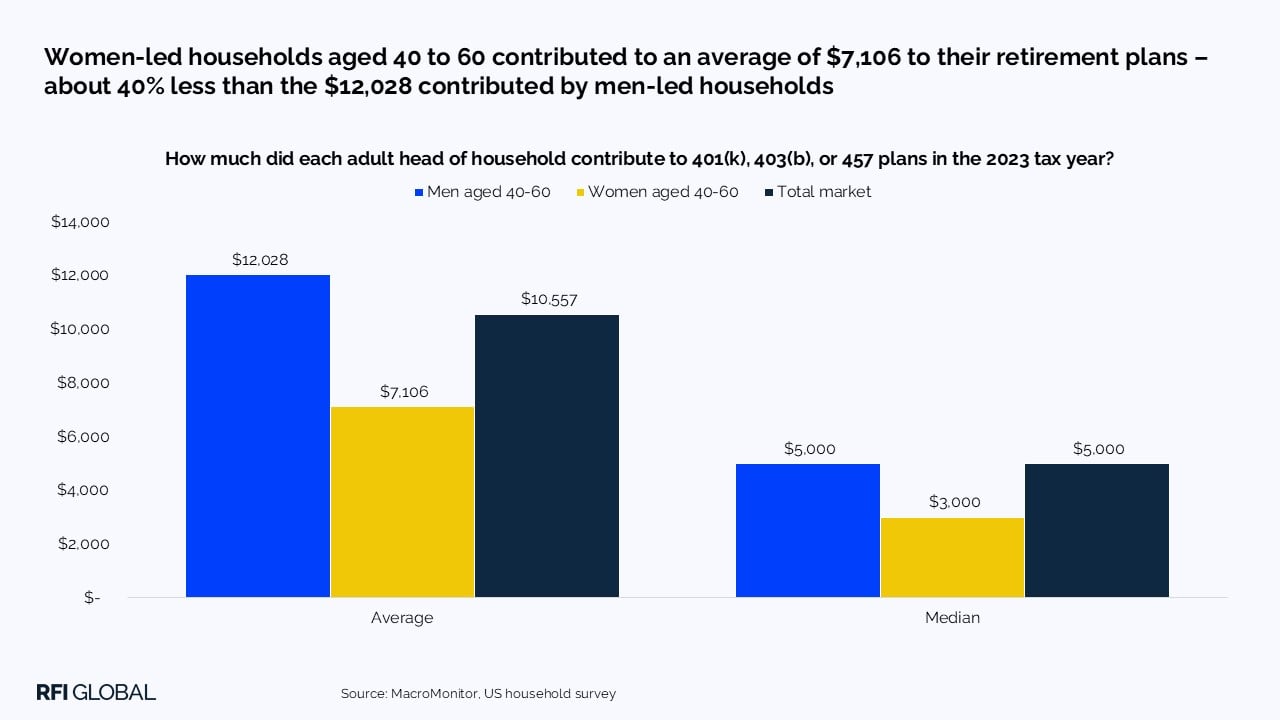

Income interruptions compound these pressures over time. Women contribute an average of $7,106 annually to retirement plans, far below men’s $12,028, resulting in lower total retirement balances of $152,781 compared with $200,500 for men. Median annual contributions tell the same story, at $3,000 for women versus $5,000 for men. These gaps reflect years of reduced earning power, paused contributions, and delayed recovery tied closely to caregiving responsibilities.

At the macro level, the scale is staggering. Americans provide 30 billion hours of informal care for the elderly each year, representing $522 billion in forgone earnings, according to RAND. Each hour spent caregiving is an hour not spent earning, saving, or compounding, and when those hours cluster in midlife, the financial effects reverberate across decades.

Banking implications: why caregiving must be a strategic priority

Caregiving reshapes financial behavior in ways banks often fail to detect. The result is misaligned products, credit decisions that penalize caregivers, and underestimated long-term value. Caregiving increases liquidity pressure through unpredictable expenses such as medical co-pays, mobility aids, home modifications, and travel for appointments. It also adds layers of financial complexity as caregivers frequently manage both their own finances and those of aging parents.

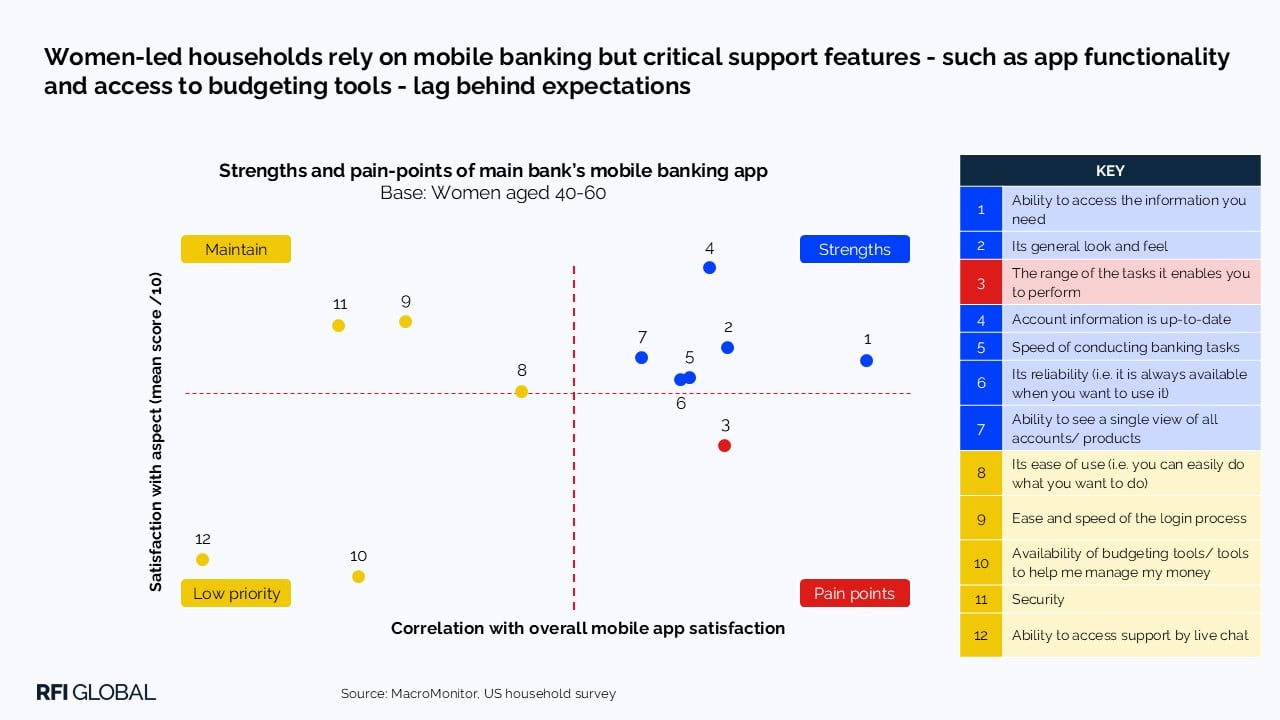

MacroMonitor data shows that women-led households rely heavily on mobile banking to navigate these demands. Nearly three-quarters (74%) of women-led households aged 40 to 60, report using a mobile app to access their financial accounts. Yet critical support features lag behind expectations, with gaps in app functionality, budgeting tools and live chat support making it harder to manage multi-household finances and irregular expenses. At the same time, women have a growing influence over high-value decisions, including long-term care, insurance, and home adaptations. When banks recognize care-driven digital reliance and design tools that truly support it, trust and retention rise. When they do not, they miss a critical loyalty trigger.

Caregiving through an ethnic lens

Caregiving intensity and financial strain vary sharply across racial and ethnic groups, a nuance often missing from standard segmentation. AARP data shows that 61% of caregivers are non-Hispanic white, broadly reflecting the population share. However, caregiving intensity and financial exposure are disproportionately concentrated among caregivers of color. Hispanic caregivers, who represent 16% of caregivers according to the Center for Economic and Policy Research, are more likely to provide high-intensity and co-residential care. Black caregivers, representing 13%, experience heightened income volatility due to lower wealth buffers and greater reliance on earned income. AANHPI caregivers account for 6%, but cultural expectations often drive earlier and longer caregiving commitments, reducing their lifetime savings capacity.

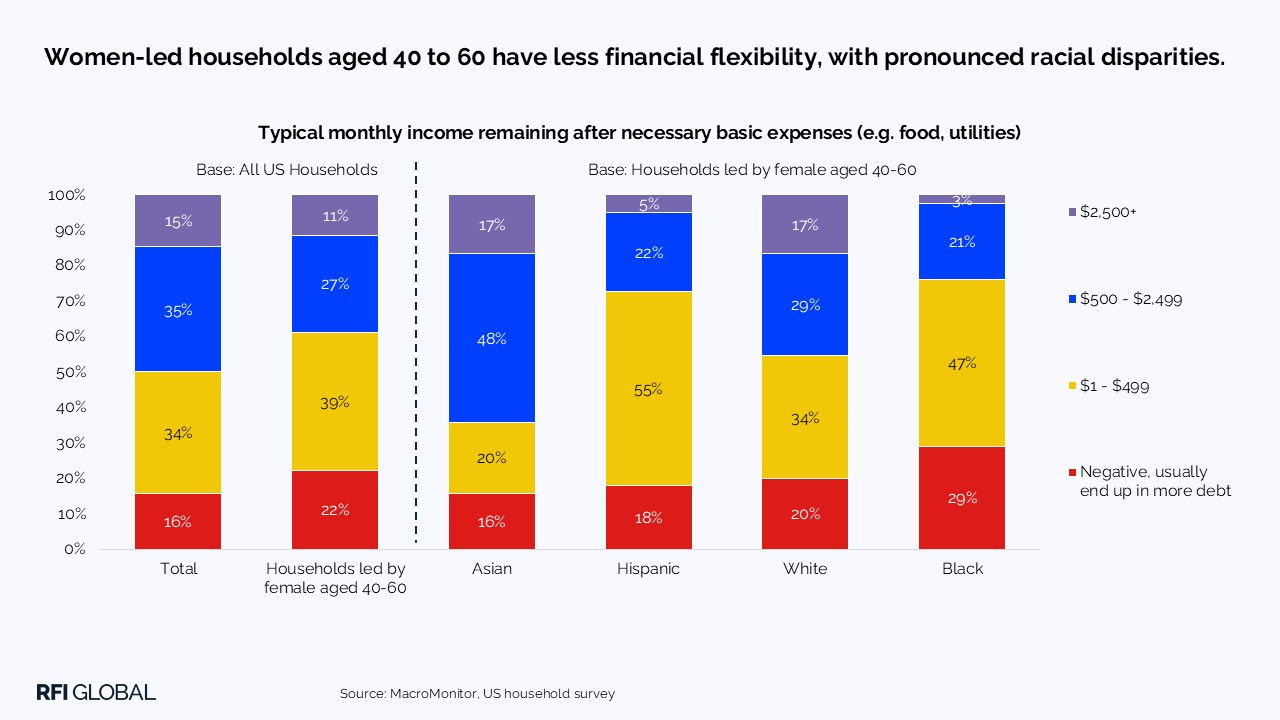

MacroMonitor data underscores the resulting financial strain. After covering basic expenses, 29% of Black women-led households, 18% of Hispanic households, and 16% of Asian households report going into debt. Liquidity buffers are thin: 55% of Hispanic and 47% of Black women-led households have less than $500 left after essentials, compared with 34% of the average household.

These disparities reflect the intersection of wage gaps, wealth gaps, and caregiving gaps. For banks, failing to adapt products and outreach means overlooking millions of customers who face disproportionate financial burden while representing significant long-term value.

The overlooked segments and the missed value

Banks frequently overlook caregiving-related segments not because they lack value, but because their financial lives do not follow linear earning and saving models. Middle-income women with caregiving-driven income volatility often maintain long relationships and stable core balances but are misread by rigid credit frameworks. Women of color with higher caregiving intensity show elevated day-to-day financial activity and recurring liquidity needs that remain underserved. Daughters managing parents’ finances remotely influence two households’ banking decisions at once. Women re-entering the workforce after caregiving breaks represent critical inflection points where early engagement can anchor long-term loyalty.

The strategic imperatives for banks

As caregiving stretches longer and begins earlier, banks face a growing risk of misreading some of their most valuable customers at precisely the moment when trust and relevance matter most.

1. Improve risk assessment: caregiving-driven income volatility and liquidity strain are often adaptive, not chronic. Banks that distinguish caregiving-related disruptions from long-term instability can reduce unnecessary credit declines and avoid mispricing loyal, midlife customers.

2. Design for caregiving complexity: caregivers manage multiple households and unpredictable expenses. Products that support flexible liquidity, delegated account access, and dual-household financial management reduce friction while increasing engagement.

3. Invest in loyalty over life stages: caregiving is a phase, not a permanent condition. Women supported through caregiving transitions show higher retention and broader product use once financial stability returns. With women projected to control $45 trillion in US assets within the next decade through intra-household wealth transfer, caregiving-aware design is not a concession. It is a long-term growth strategy.

Women’s financial lives rarely follow the clean, linear trajectory assumed by legacy banking models. Caregiving reshapes earnings, savings, credit behavior, and long-term wealth. Banks that design for real life rather than idealized life paths will earn trust, deepen relationships, and capture long-term household value in an aging America.

Find out more

These insights are from MacroMonitor, the largest and most comprehensive survey of US financial behavior. For more information on how RFI Global’s data and expertise can support your strategic initiatives and strengthen your wealth offering, please get in touch.

Tiffany Ng

Client Executive, North America

Tiffany Ng is a Client Executive at RFI Global, supporting financial institutions across North America.

View full profileCaregiving, women’s finances, and what banks need to know: key questions answered

Q: Why does caregiving have such a large financial impact on women?

A: Caregiving disproportionately affects women because they provide the majority of unpaid care, often during mid-career years. This reduces earnings, interrupts retirement contributions, increases reliance on short-term liquidity, and compounds long-term wealth gaps. Data from RFI Global’s MacroMonitor shows that US women-led households are more likely to face financial precarity and lower retirement readiness as a result.

Q: How does caregiving change financial behavior and banking needs?

A: Caregiving increases financial complexity and unpredictability. Women caregivers are more likely to manage multiple households, face irregular expenses, and rely heavily on mobile banking tools for real-time account access, payments, and monitoring. Traditional banking products and risk models often fail to account for these care-driven patterns.

Q: Why are US banks misreading caregivers as higher risk?

A: Income fluctuations caused by caregiving are usually temporary adjustments, not indicators of long-term financial risk. However, many credit and risk frameworks interpret these fluctuations as chronic instability. This can result in unnecessary credit declines or conservative pricing, as caregiving-related income volatility is assessed using models that do not account for long-tenured, highly engaged customer behavior.

Q: What should banks do differently to support women caregivers?

A: Banks should design products and risk assessments that reflect caregiving realities, including flexible liquidity solutions, delegated account access, dual-household financial management tools, and credit pathways for workforce re-entry. Supporting women through caregiving transitions builds trust, improves retention, and unlocks long-term customer value.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.