The UK financial services sector enters 2026 with a market that is highly digital, increasingly competitive and shaped by technology. Neobanks are moving from rapid growth to sustainable profitability, mobile banking dominates customer interactions, and artificial intelligence is increasingly becoming part of consumers’ everyday financial management.

In our Financial Services Trends and Predictions 2026 global report, we identified five trends we believe will shape the industry next year. Drawing on insights from over 4,000 UK consumers, this article examines how these shifts will affect financial institutions in the UK and where the biggest opportunities lie.

1. Trust in AI: Adoption of AI accelerates as use cases increase

AI in the UK financial industry is moving beyond its experimental phase. According to a 2024 Bank of England survey, 75% of firms in the sector were already using AI, mainly for data analytics, anti-money laundering, fraud prevention and cybersecurity. While 55% of AI use cases involved some automated decision-making, only 2% are fully autonomous, showing that human oversight remains critical.

On the consumer side, adoption is accelerating. Lloyds Banking Group’s latest Consumer Digital Index shows that more than 28 million UK adults now use AI to help manage their money, with 1 in 3 using it weekly. This signals a clear opportunity for banks to integrate AI into everyday journeys, but trust remains the deciding factor. Customers want transparency about how AI works, reassurance on accuracy and the option to speak to a human when needed.

2. Digital UX: The market is now firmly into the mobile-first era

Mobile banking is the dominant channel in the UK. According to RFI Global’s Orion UK data, 68% of consumers use mobile banking at least once every other week and 45% of all banking interactions are now on mobile. Our data shows that satisfaction is strong, with three-quarters of consumers very satisfied with their main bank’s digital and mobile capabilities.

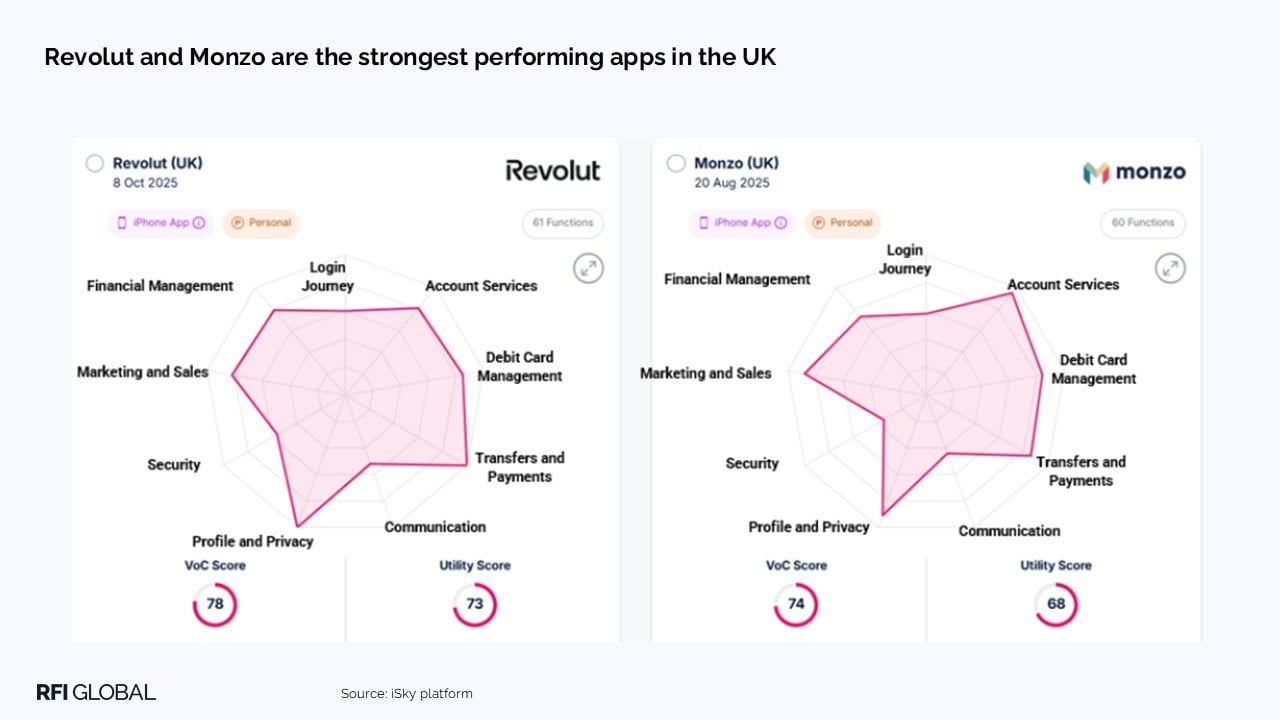

UK neobanks are leading innovation. Data from our iSky Platform that monitors thousands of real consumer interactions with banking apps worldwide shows that Revolut and Monzo achieve the highest Utility Scores (a measure of functionality) among all retail banks assessed in the UK, and offer the broadest range of personal finance management tools. The data also shows providers are investing heavily in improving mobile app capabilities, with the average Utility Score in the UK increasing by 38% since January 2022.

The shift to mobile-first banking means digital experience is now a key battleground for customer engagement and loyalty. With satisfaction levels already high in the UK, differentiation will come from personalisation and integrated tools that make financial management effortless. Providers that fail to keep pace risk competing only on price, while those that deliver intuitive, secure and feature-rich mobile experiences will strengthen engagement and retention.

3. The next chapter for Neobanks: A pivot in focus from customer acquisition to value

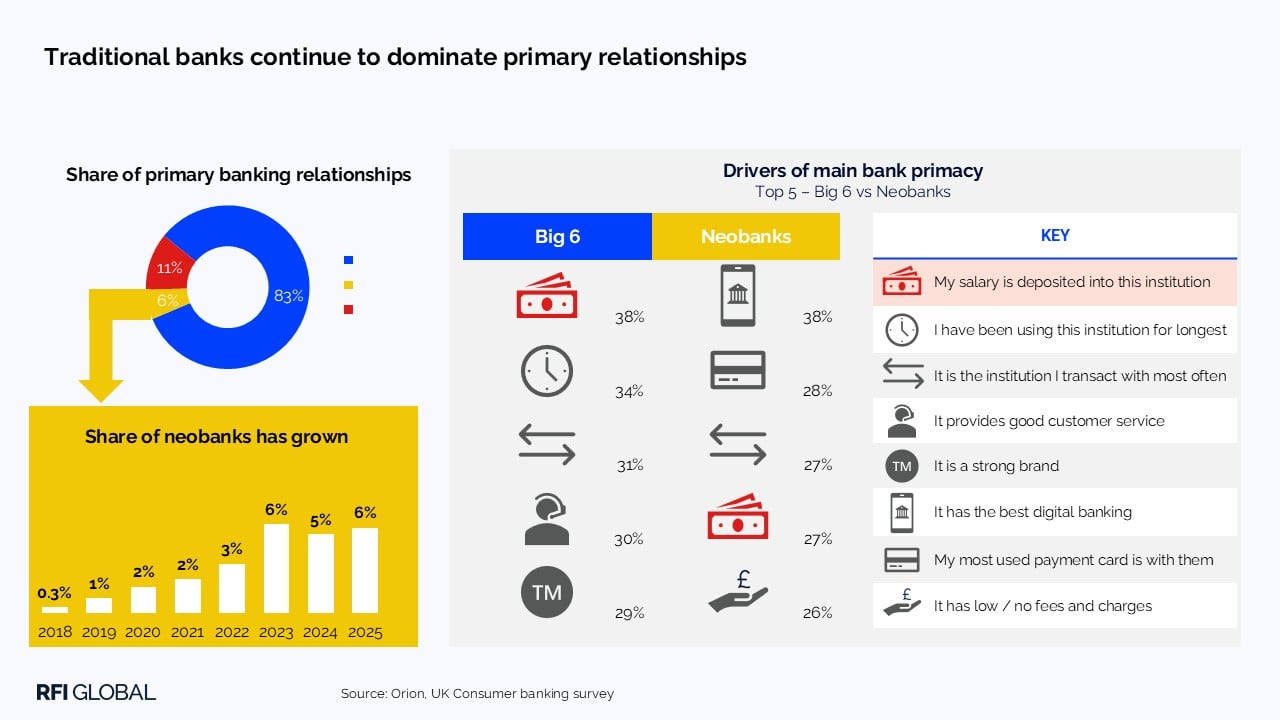

Neobanks in the UK are moving beyond customer acquisition to focus on profitability and deeper engagement. A quarter (26%) of UK consumers now have an active relationship with a neobank, and their share of primary banking relationships has grown from 3.5% to 5.9% between 2022 and mid-2025. Among consumers who started their main banking relationship in the past three years, neobanks now hold over 20% of market share.

Monzo reported its first annual profit in 2024, with deposits up 88% to £11.2 billion and revenue more than doubling to £880 million. Revolut continues to scale globally while driving engagement through product diversification.

As we look towards 2026, the trend is clear: neobanks are no longer just disruptors used for secondary relationships or transactional perks and they are increasingly evolving into full-service financial institutions. Providers need to broaden their offerings, introduce premium tiers and embed tools that make daily financial management easier.

4. Cybersecurity: the evolving fraud landscape

Fraud remains a major issue in the UK. According to UK Finance Annual Fraud report 2025.pdf 2025, £1.17 billion was stolen through unauthorised and authorised payment fraud in 2024, similar to 2023. There were 3.31 million fraud cases recorded, showing the scale of attacks. On a positive note, £1.45 billion of unauthorised fraud was prevented by the industry, up 16% from 2023.

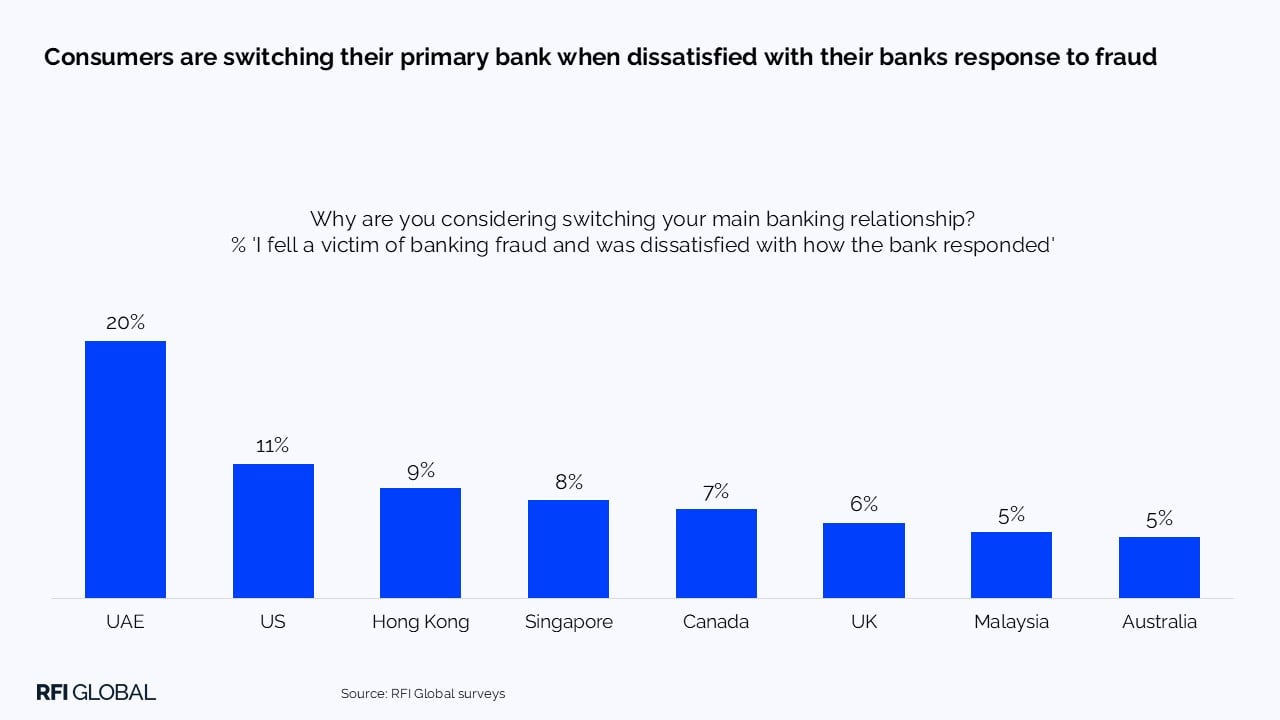

Consumers prioritise security when choosing payment methods, and businesses are increasingly concerned. Six percent of UK consumers who are considering switching say they are doing so because they are dissatisfied with how their bank handled fraud. Further, two-fifths of UK consumers (39%) say the security features for authenticating payment are the #1 consideration when choosing a payment method for online purchases.

With the UK’s Economic Crime and Corporate Transparency Act introducing tougher penalties for firms without adequate safeguards, the pressure to act is rising.

5. Wealth in 2026: Turning intent into action

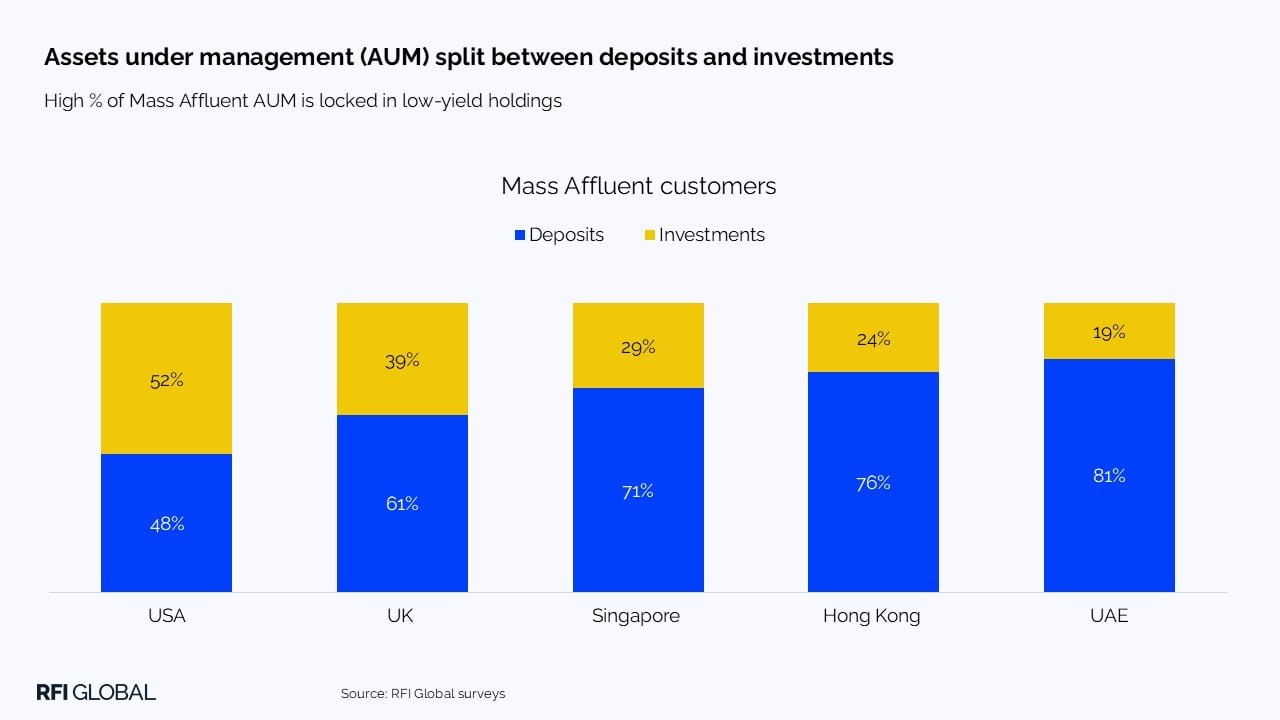

Lower interest rates are pushing affluent consumers toward investments. In the UK, 31% of mass affluent consumers plan to make their money work harder for them over the next 12 months, but around 60% of liquid assets remain in low-yield deposits. This intent outpaces other segments, signalling strong demand for higher returns and reinforcing the need for banks to deliver tailored investment propositions.

This creates a clear opportunity for financial providers to convert deposits into investment portfolios through education, personalised advice and simple digital journeys.

Competition is intensifying from fintechs and neobanks offering sleek interfaces and lower fees. Incumbents need to modernise their wealth propositions and embed investment tools into digital platforms to stay relevant.

What next for UK Financial Services?

In 2026, UK banking will be shaped by smarter technology and stronger competition. AI will continue to move from behind the scenes into everyday banking, powering personalisation and practical tools that help people manage their money more efficiently.

With most interactions now taking place on mobile and satisfaction already high, the challenge will be to deepen what banking apps can offer. Banks will need to encourage uptake of new features and strengthen personalisation to keep customers engaged.

At the same time, neobanks are entering a more mature phase and competing more directly with established players. Their focus is shifting from fast expansion to sustainable growth, supported by premium accounts, new partnerships and broader product ranges that bring them closer to being full-service providers. As they advance, traditional banks will need to accelerate their digital improvements and make their value clearer to customers.

Download the full Financial Services Trends and Predictions 2026 report for more data-driven insights on UK consumer trends and how they compare to other markets.

Interested in how these trends are shaping the US? Read this article.

Frequently Asked Questions on UK financial services trends for 2026

Q: What are the main trends shaping UK financial services in 2026?

A: Five trends are influencing the UK market: growing consumer use of AI, a shift to mobile-first banking, the maturation of neobanks, rising fraud threats and increased investment intent among affluent consumers. Together, these trends are reshaping how UK institutions compete, engage customers and build value. Source: RFI Global.

Q: How is AI changing banking for UK consumers?

A: AI is becoming part of everyday money management, with more than 28 million UK adults already using AI tools. Consumers are open to more AI-driven services, but trust and transparency remain essential. Banks that provide clear explanations, accuracy and easy access to human support will see the strongest adoption.

Q: Why is mobile banking now critical for UK customer engagement?

A: RFI Global data shows mobile is the UK’s dominant banking channel, accounting for 45% of all interactions. With satisfaction already high, differentiation now depends on personalisation and integrated financial management tools that make day-to-day banking seamless.

Q: What does rising investment intent mean for UK financial institutions?

A: Although 31% of mass affluent consumers plan to seek higher returns, most of their liquid assets remain in low-yield deposits. This creates a clear opportunity for providers to convert intent into action through better education, tailored advice and simple digital investment journeys.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.