Jon Ruston, Insights Director, EMEA & North America

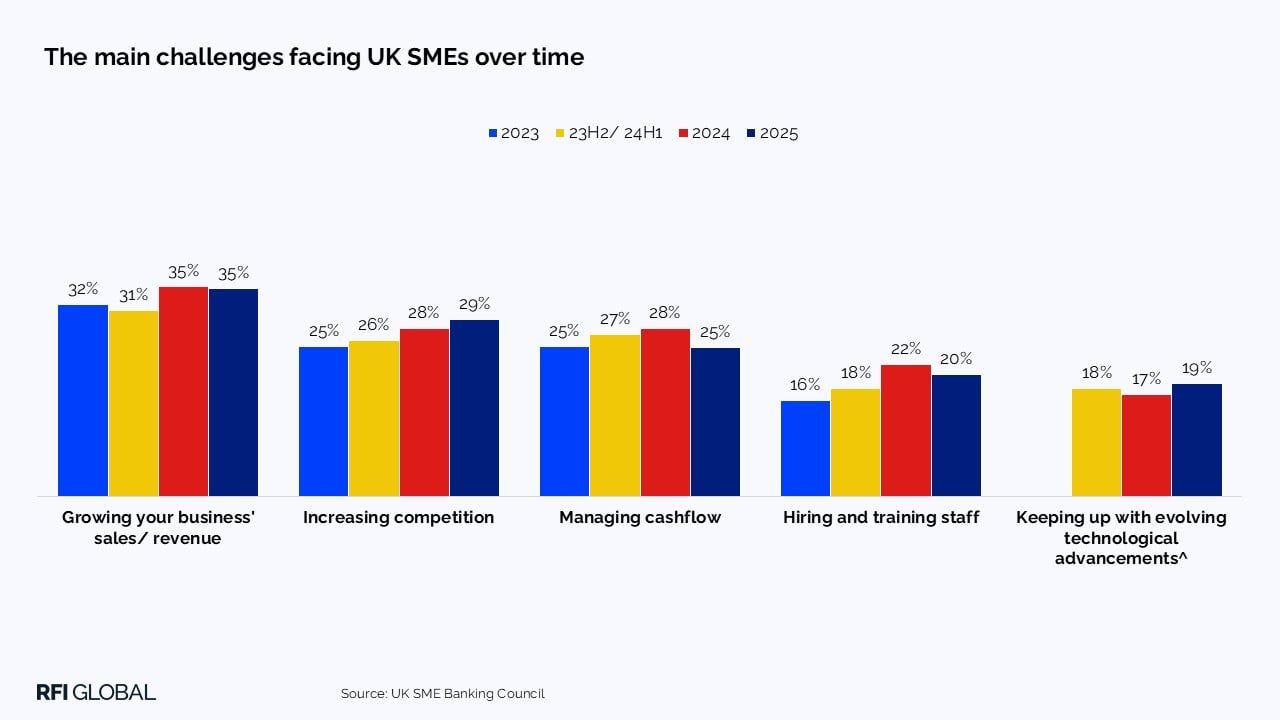

2025 has been a challenging year to run a small business in the UK. Over the past five years, SMEs have weathered unprecedented disruptions, from COVID-19 and supply chain issues to inflation, rising interest rates and global trade uncertainty. Data from our latest SME banking survey shows that since 2024, SMEs have reported a significantly higher number of challenges, a trend continuing into 2025. Competitive pressure is mounting, making it harder for SMEs to grow revenue, as they compete for customer spend amid rising costs.

So how can financial service providers help SMEs grow their businesses?

We explored our data to uncover the key challenges SMEs face, their expectations around AI and personalisation and how financial institutions can better meet their needs.

Rising challenges and growing pain points

For the first time in 2025, keeping pace with technological change has emerged as a top five challenge, as SMEs navigate the fast-moving landscape of artificial intelligence and digital innovation.

In 2025, the number of pain points SMEs experience with their main bank has increased year-on-year. As SME challenges grow, it’s crucial to understand how these pressures are reshaping their financial relationships. Our data highlights that top pain points for SMEs include proactive advice, digital innovation and access to sector expertise. However, one notable, long-standing issue remains unresolved – commitment to long-term growth. This continues to be a top priority for SMEs, yet expectations are consistently falling short.

Commitment means more than access to finance alone

Our SME banking research uncovers what ‘commitment to growth’ truly means. While access to finance remains vital, SMEs increasingly expect more. They seek solutions that scale alongside a business, delivered through proactive advice and digital innovation at every stage of their journey.

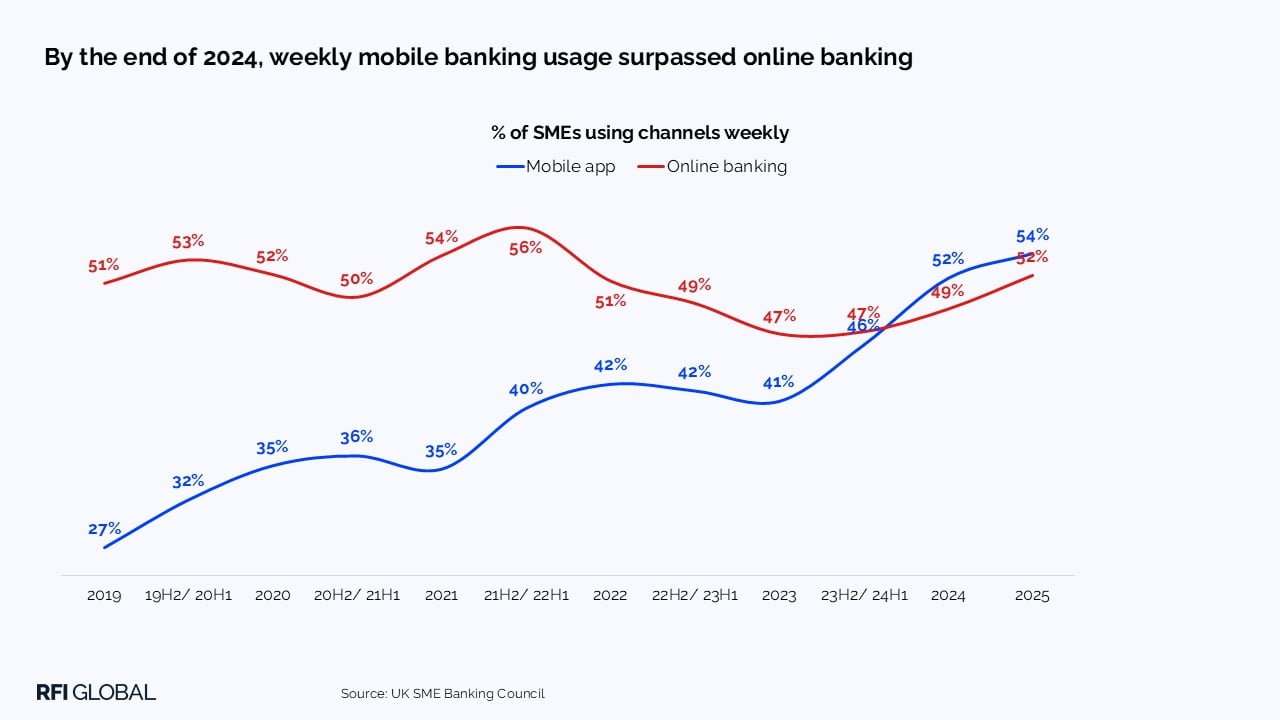

UK SME banking is now mobile-first

Our data has continued to highlight the acceleration towards digital channels among SMEs. By the end of 2024, weekly mobile banking usage surpassed online banking for the first time, a trend that has continued in 2025, with over half of UK SMEs using mobile apps weekly.

In this mobile-first landscape, understanding how to win through mobile banking is more critical than ever.

Personalisation is paramount as SMEs now see their mobile banking app as the gateway to their broader financial ecosystem. More than 1 in 2 SMEs seek greater personalisation from their mobile banking app. This opens opportunities to deliver tailored product recommendations, personalised interfaces and business insights. As reliance on mobile grows, SMEs are ready to do more through their apps and expect greater functionality. Two in three SMEs state they most value access to invoicing tools and accounting integrations in their mobile banking app. Therefore, these functionalities are no longer optional; they are essential.

Getting the channel mix right

With more SMEs using mobile banking apps, we could assume that it spells the end for traditional banking channels. However, 1 in 2 SMEs report being dissatisfied with the level of proactive advice received from their main bank, a key factor weighing down overall advocacy levels. In a mobile-first landscape, expectations are not only rising for digital channels, but also for what can be delivered beyond them, driven by the human touch. As a result, it has never been more crucial to understand what the optimal service model looks like.

SMEs prefer digital channels for tasks like opening a business account or searching for product information, offering autonomy and seamless applications. However, for more complex tasks, such as applying for a business loan or seeking tailored advice, SMEs desire a human touch. Therefore, SMEs are craving more than a one-size-fits-all approach. The winning financial institutions will be those that are agile enough to deliver the ‘opti-channel model’, providing the right product or service, at the right time, through the right channel.

Artificial intelligence – a threat or benefit to SMEs?

As discussed earlier, technological change is a top challenge facing SMEs, with artificial intelligence at its core. At RFI Global, we have been tracking sentiment towards artificial intelligence among UK SMEs for the past 3 years. In 2023, 1 in 10 SMEs (10%) reported having no concerns with using AI. That figure has now risen to over 1 in 4 in 2025 (27%), a trend we expect to continue into 2026. Furthermore, 2 in 5 SMEs report they are very comfortable with the introduction of AI in financial services.

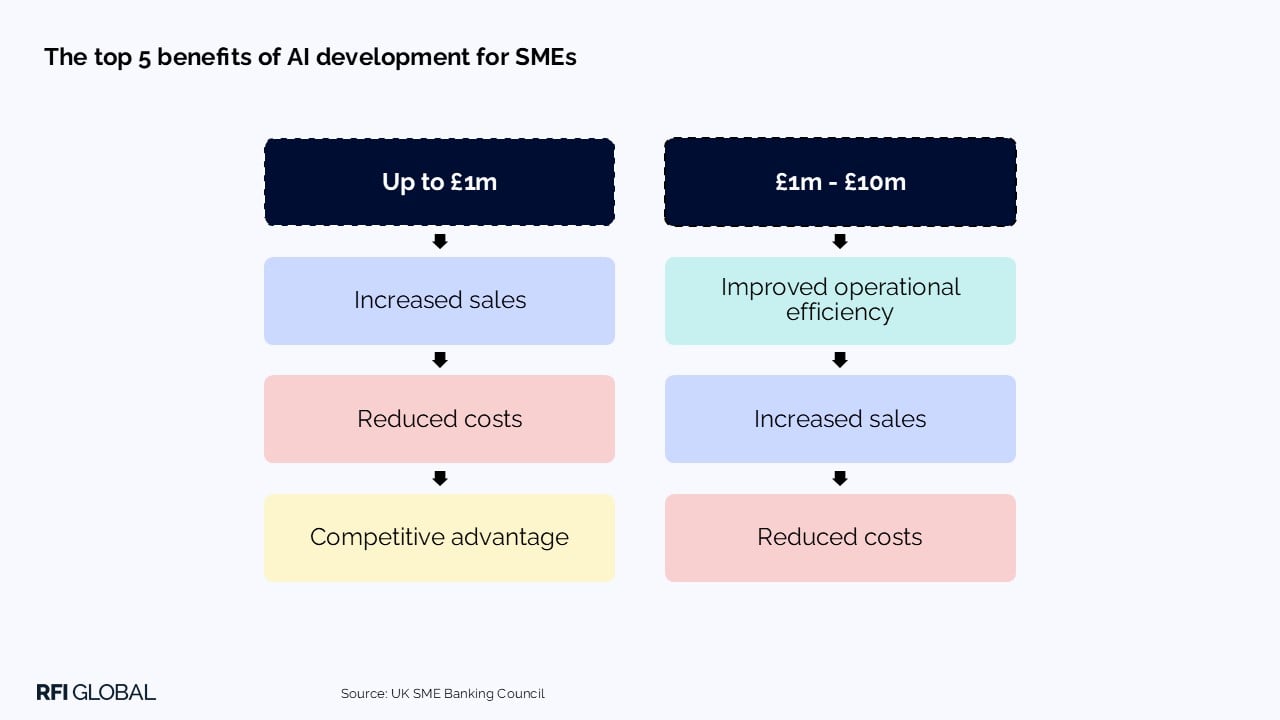

As comfort levels with AI rise, it is important to understand the perceived threats as well as the benefits to help alleviate concerns. One of the most recognised advantages is improved operational efficiency, particularly among SMEs with £1m+ in annual revenue. Meanwhile, SMEs with <£1m in annual revenue cite cost reduction and delivering a competitive advantage as top benefits. A perception of increased sales is also a top perceived benefit. However, over 1 in 4 SMEs say data security and privacy are their biggest concern, with 1 in 5 highlighting the replacement of human touch.

Delivering transparent communication about how and why AI is being used in financial services, alongside clearly outlining the benefits and expected outcomes, is therefore essential. Given the importance of proactivity in SME banking, being on the front foot is critical as we help SMEs navigate technological change. This is not only essential to meeting SMEs’ needs in 2025, but also to future-proof relationships.

Winning strategies for SME success

As SMEs navigate another year of uncertainty, financial institutions have a clear opportunity to stand out by combining digital innovation, proactive support, and trust. Our data highlights four key strategies to strengthen SME relationships and drive growth in 2026 and beyond.

1. Commit to SME growth

SMEs expect more than just access to finance alone. They value solutions that scale with their business, delivered through proactive advice and digital innovation. This is essential to meeting SMEs’ evolving expectations.

2. Lead in a mobile-first era

With over half of UK SMEs using mobile banking apps weekly, personalisation and functionality are paramount. Financial institutions should focus on delivering tailored product recommendations, personalised interfaces, and essential tools like invoicing and accounting.

3. Deliver an opti-channel experience

SMEs prefer digital channels for routine tasks but seek human touch for complex needs. The opti-channel model is the key to success, providing the right product or service at the right time, through the appropriate channel.

4. Embrace technological change

SMEs are increasingly challenged by the fast-paced technological landscape, underpinned by digital innovation and artificial intelligence. Financial institutions must prioritise proactive advice and solutions in navigating these changes.

Watch our on-demand webinar for further insights from our survey on SME needs and expectations.

Jon Ruston

Insights Director, EMEA & North America

Jon Ruston is an Insights Director at RFI Global, leading research programmes across EMEA and North America.

View full profileFrequently asked questions about branches

Q: What are the biggest challenges facing UK SMEs?

A: UK SMEs are navigating multiple pressures, from rising costs and inflation to increasing competition and rapid technological change. RFI Global research shows that keeping pace with digital innovation and artificial intelligence became a top five challenge for the first time in 2025.

Q: How can financial institutions better support SME growth?

A: UK SMEs want more than access to finance. They expect proactive advice, tailored digital solutions and scalable tools that help their business grow. Financial institutions that combine innovation with relationship-led support are best positioned to meet these expectations.

Q: Why is mobile banking so important for UK SMEs?

A: More than half of UK SMEs now use mobile banking apps weekly. This shift has made mobile the primary channel for managing finances, meaning personalisation, functionality, and integrations, like invoicing and accounting, are now essential for engagement and retention.

Q: What role does AI play in the future of SME banking?

A: AI is transforming SME banking by improving efficiency, reducing costs and enabling personalised experiences. However, data security and the need for human interaction remain key concerns. Transparent communication about how AI is used will be vital to building SME trust.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.