Tiffany Ng, Client Executive, North America

In today’s evolving family landscape, many Americans—especially Gen-Xers and older Millennials aged 40 to 60—are navigating the dual caregiving challenge, supporting both aging parents and dependent children. According to the Pew Research Center, approximately one in seven Americans in this age group is providing financial assistance to both a parent and a child.

Crucially, this caregiving burden often falls more heavily on women. A 2025 report by the Federal Reserve highlights that among households with children under age 13:

– 56% of mothers say they are usually the primary caretaker when children are home, compared to only 13% of fathers.

– Even when both parents work full-time, 37% of mothers say they are the primary caregiver, versus 11% of fathers.

This caregiving imbalance adds a layer of complexity to the financial responsibilities many women shoulders as part of the Sandwich Generation.

New data from RFI Global’s MacroMonitor highlights how this pressure plays out across gender: 16% of older millennial women cite family responsibilities as a significant source of stress—twice the percentage of older millennial men at 9%.

For financial service firms, this growing demographic presents an opportunity to build deeper, more meaningful client relationships. Understanding the unique financial realities of the Sandwich Generation can position firms as trusted partners during one of life’s most pivotal stages.

Understanding the financial challenges of the Sandwich Generation

1. Shifting financial priorities

The Sandwich Generation faces complex and competing financial responsibilities. Rather than focusing solely on retirement or wealth accumulation, many prioritize short-term financial resilience and debt repayment.

MacroMonitor reveals notable shifts in behavior. Only 46% of households aged 40 to 60 were saving for emergencies in 2024, down from 58% in 2008. At the same time, 43% of this age group report paying off debt or mortgages compared to 36% of the total market, signaling a focus on debt reduction than the broader population.

The Sandwich Generation is walking a financial tightrope, trying to balance today’s costs with tomorrow’s goals—and that balance is growing more difficult to maintain.

2. The cost of caring for aging parents

As life expectancy increases and healthcare needs rise, long-term care costs are becoming a critical concern. The US Department of Health & Human Services (HHS) projects that the number of Americans using paid long-term care services will more than double—from 15 million in 2000 to 27 million by 2050.

Meanwhile, long-term care costs remain steep: in 2024, the average annual cost for a shared room in a nursing home was approximately $111,325, and a private room cost around $127,750 American Council on Aging.

Despite these rising costs, MacroMonitor reveals that only 22% of 40–60-year-olds have savings or investments designated for future medical or long-term care expenses. Long-term care insurance, though available, remains underutilized, especially among those already shouldering the dual caregiving and financial pressures of the Sandwich Generation.

3. Navigating the rising cost of education

College costs remain high and continue to climb. According to the National Center for Education Statistics the average annual tuition at public four-year universities stood at $27,100 for the 2022–2023 academic year. However, our latest data shows that fewer Sandwich Generation households are prioritizing education savings.

Only 13% of households aged 40 to 60 prioritize education savings, less than half the 27% who did so in 2008. With so many financial obligations on their plate, education funding has become a lower priority.

The implications for Financial Services firms

Increased demand for financial advice

Growing uncertainty among the Sandwich Generation about achieving financial goals is fueling demand for expert guidance. Our data shows that 35% of this group feel less confident about meeting their goals, compared to 26% of the rest of the market, signaling a strong demand for professional support.

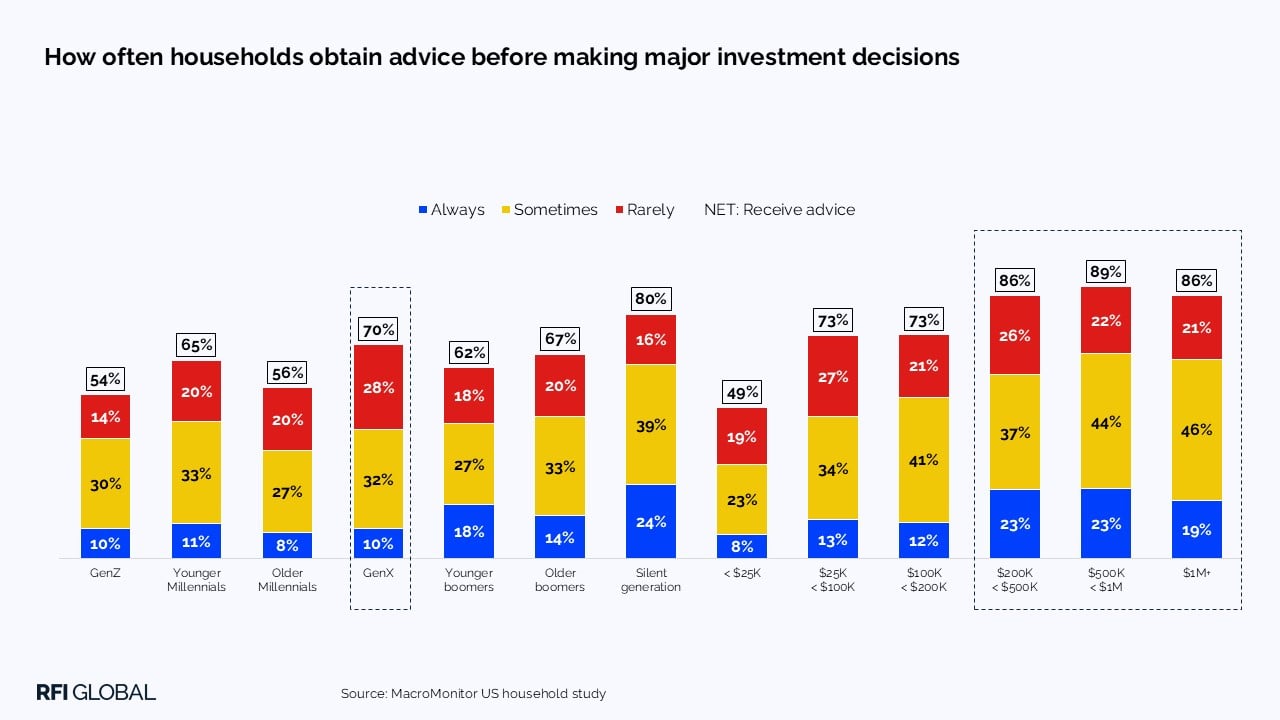

As a result, more households are seeking financial advice, creating a clear opportunity for firms to strengthen their role. Among 40 to 60-year-old households, we see that demand for advice rises with affluence, and with it the opportunity for firms to deepen relationships by guiding financial decisions. When further segmented by investable asset levels, Emerging Affluents, with $50,000 to $500,000 in investable assets, are more likely than the average household to consult an advisor, though typically only occasionally. In contrast, High-Net-Worth households, with $3 million or more in investable assets, are more likely to rely on advisors for nearly all financial decisions. This pattern underscores a critical opportunity for firms to deepen engagement as households accumulate greater wealth.

Winning over Gen X and the older Millennial wealth

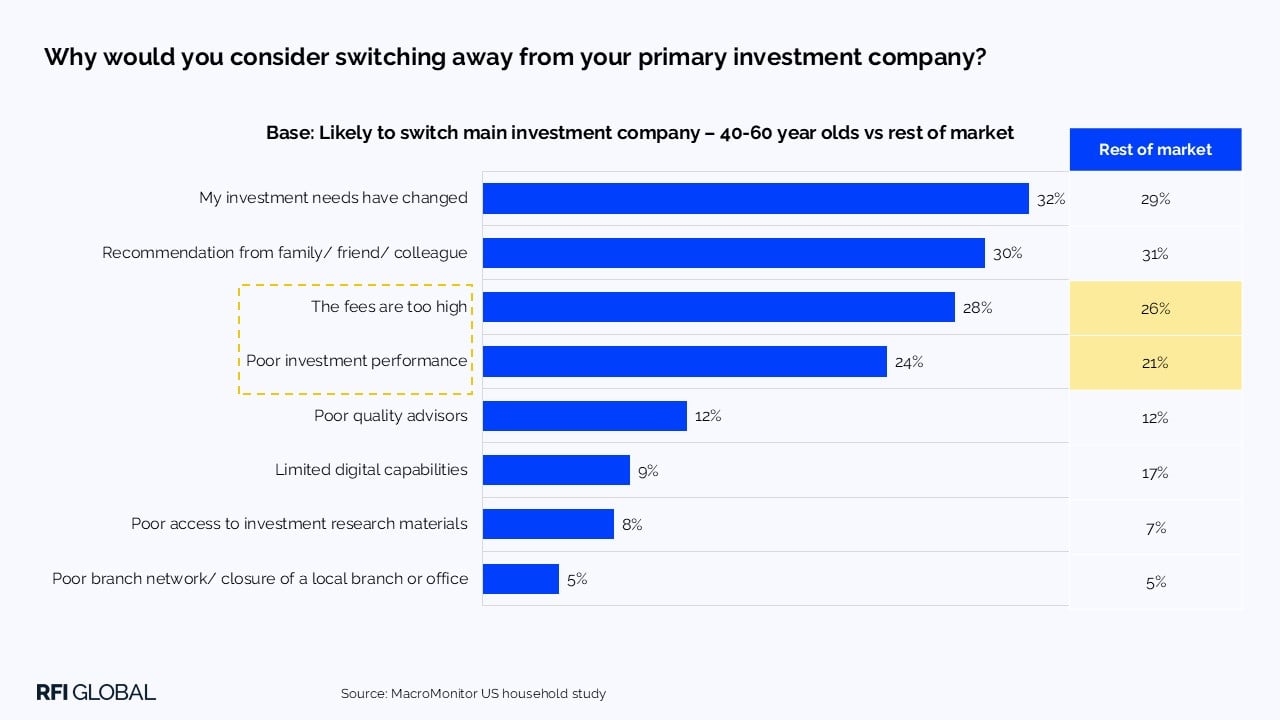

Rising switching behavior signals a major opportunity for financial service firms. MacroMonitor shows that 29% of Gen X and 35% of older Millennials are open to switching their primary investment providers.

– High Net Worth Gen X households show the strongest intent to switch, with 39% considering a change compared to just 12% of the average household.

– 28% of High-Net-Worth Millennials report intent to switch, more than double the average household.

– Mass Affluent older Millennials, with $500,000 to $3 million in assets, also stand out, with 39% indicating intent to change providers.

Our findings show much of this movement is driven by dissatisfaction with fees and unmet investment expectations, especially among Gen X and older Millennials. Firms that address these pain points with clear communication, transparent value, and realistic guidance have a strong opportunity to win and retain these high-potential clients.

Advising the Sandwich Generation through the great wealth transfer

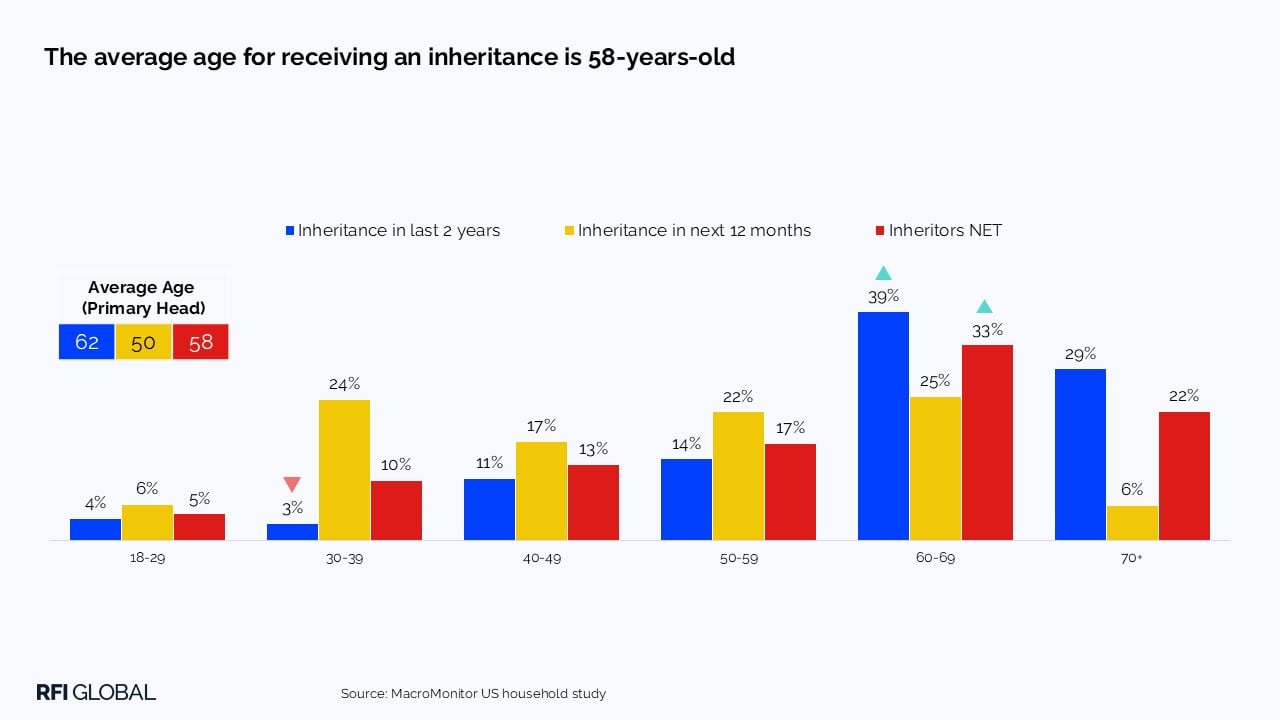

Inheritance represents a significant financial milestone for many Americans, and an unprecedented wealth transfer is coming. Our data shows that households aged 70 and older are expected to transfer $45 trillion to the next generation over the next decade. It reveals that this shift is already underway —3.39 million households have already received an inheritance, and another 1.93 million households expect to receive it in the next 12 months. Households aged 60 to 69 make up the largest group of inheritance recipients; 39% have received an inheritance recently, and another quarter expect to receive it in the next 12 months. With the average age of inheritance at just 58, many recipients are still working and juggling retirement planning and family obligations.

Capturing and advising on this wealth transfer is a critical opportunity for financial service firms, and an opportunity to deepen relationships, preserve assets under management, and guide clients through complex financial decisions.

Key takeaways for financial services firms

The Sandwich Generation represents a prime opportunity for financial service firms to capture new business and position themselves as indispensable partners in wealth preservation and transfer. To meet their needs and turn these pressures into partnership opportunities, financial services firms should consider the following strategies:

1. Deliver holistic, personalized advice

The financial challenges of the Sandwich Generation do not exist in silos. Effective advice must address retirement, healthcare, education, debt, and daily cash flow—in the context of diverse family dynamics.

Firms should tailor solutions to reflect variation in gender, ethnicity, and income level. A one-size-fits-all approach won’t work with a generation juggling so many priorities.

2. Build trust through transparency and value

Consumers want to understand what they’re paying for—and what they’re getting. For Gen X and older Millennials, clear communication, transparent value, and realistic guidance are key to winning and retaining these high-potential clients.

3. Leverage retirement planning as a key engagement tool

Even amid shifting financial priorities, retirement remains a resonant theme—especially for those in their 40s and 50s. Some firms are already setting the bar with accessible tools. For example, firms Charles Schwab offers a free retirement savings calculator that factors in age, retirement goals, income, savings, Social Security, and spending plans to project future retirement readiness. Vanguard provides a similar tool allowing users to input retirement age, savings, spending expectations, and investment allocation to estimate how long their money will last.

By offering clear, actionable planning tools like these, firms can demonstrate tangible value, build trust, and establish themselves as essential partners in preparing clients for retirement.

4. Turning long-term care into a growth opportunity

Financial firms can win trust by guiding the Sandwich Generation through the real costs of long-term care. Lincoln Financial shows how with its Hybrid Long-Term Care solution, which makes planning accessible and strategic for households juggling work, parenting, and elder care.

5. From wealth transfer to wealth partnership

Financial service firms that proactively guide 40 to 60-year-old heirs through inheritance decisions by offering clear strategies for wealth preservation, tax efficiency, and long-term planning can capture lasting relationships during the Great Wealth Transfer.

Get in touch to learn more about how the Sandwich Generation is reshaping financial priorities and expectations. Our latest survey dives deeper into the behaviors, pressures, and opportunities facing this group, especially as they navigate caregiving, debt, and long-term planning.

Tiffany Ng

Client Executive, North America

Tiffany Ng is a Client Executive at RFI Global, supporting financial institutions across North America.

View full profileFrequently Asked Questions

Q: What is the Sandwich Generation and why is it important for financial services?

A: The Sandwich Generation refers to adults (typically aged 40 to 60) who financially support both their children and ageing parents. This dual responsibility creates complex financial needs—making them a key segment for financial institutions to understand and serve.

Q: What financial challenges does the Sandwich Generation face?

A: They are balancing debt reduction, rising care costs, education expenses and lower emergency savings. Many are prioritising short-term financial survival over long-term goals like retirement and long-term care planning.

Q: Why is the Sandwich Generation under financial stress?

A: Women often take on more caregiving, which adds to financial strain. RFI Global data shows that 16% of older millennial women cite family responsibilities as a major source of stress — compared to 9% of men — highlighting a gender gap in financial pressure.

Q: How can financial advisors help the Sandwich Generation?

A: With declining confidence and rising demand for advice, financial firms that offer personalized, holistic guidance can win trust, deepen client relationships and retain assets—especially as this group prepares for the Great Wealth Transfer.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.