Luke Allchin, Director, North America

New data shows that liquid wealth has declined significantly since 2022 after a steady increase since the pandemic. Why is this? And, with overall wealth rising, where are US investors putting their money?

The pandemic drove liquid wealth to new levels

The COVID-19 pandemic was a watershed moment for the global economy, and its effects are still echoing throughout the financial landscape, especially in the US. One of the most significant shifts observed was the rise of liquid wealth among US households, a change that occurred largely due to government income support measures and a sudden shift in personal consumption habits. According to RFI Global’s MacroMonitor study, the average US household saw its liquid assets increase 27% between 2020 and 2022. As the pandemic’s immediate effects wore off, many households that had once accumulated unprecedented liquid wealth are now facing a difficult reality of rising debt and declining financial cushions. The story of liquid wealth, its rise, and its fall, offers valuable insight into the economic pressures facing households today, and how financial institutions can better meet their needs.

The post-pandemic decline

As COVID-19 restrictions began to lift in 2021, pent-up demand led to a surge in consumer spending. Meanwhile, the cost of living began to rise at an alarming rate. Inflation reached levels not seen in decades, and with it came rising prices on essentials like food, gas, and housing.

As a result, credit card delinquency rates, which had dropped during the pandemic, began to rise once again. Over the past two years, the strain of rising costs has begun to show, particularly among lower-income households. MacroMonitor data shows that the number of households struggling to repay credit card debt is notably higher for the lowest-income groups. These households have become more reliant on their credit cards and have seen their credit card balance steadily increase.

Not all households face the same challenges

While the rising cost of living and interest rates have taken a toll on many US households, the experience has not been universal. Our data shows that higher-income households, benefiting from more substantial pandemic savings and the ability to invest in higher-yielding assets, have weathered the storm better than others. These households have not only managed to preserve their liquid wealth but, in many cases, have continued to increase it by moving funds into high-interest-bearing accounts.

In contrast, households with lower incomes have been disproportionately impacted by inflation and rising borrowing costs. These households have been forced to dip into their savings or increase their debt just to maintain their standard of living. According to the Federal Reserve’s Household Debt and Credit Report (2024), household debt in the US has reached all-time highs, with much of this increase coming from credit card debt and other forms of revolving credit.

Where are US investors now putting their money?

Over the past two years, there has been a noticeable shift in where US households are investing their money. Our data shows that a growing number of households are placing their funds in certificates of deposit (CDs), money market accounts, cryptocurrencies, and US treasury securities. These areas have experienced an uptick in popularity as investors seek more secure, liquid, or alternative investment options amidst changing economic conditions.

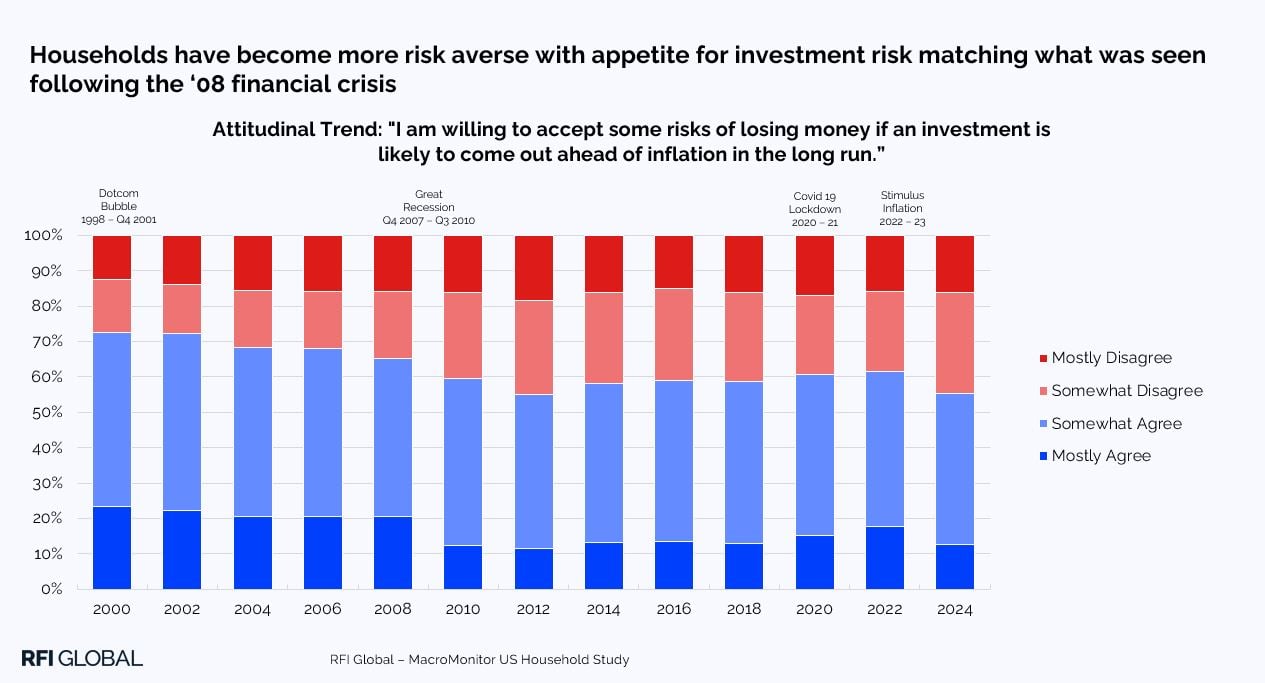

One of the most significant trends observed is the increased participation in CDs and money market accounts. These traditionally conservative options have seen growth as investors take a more cautious approach, with many opting for the guaranteed returns offered by CDs or the stability of money market accounts. MacroMonitor data shows that since 2022 households have become more risk averse, with appetite for investment risk matching what was seen following the ‘08 financial crisis.

In contrast, ownership of traditional savings accounts has declined slightly. Interest saw a steady decrease over the course of 2024, and it is likely many made the decision to move their savings into CDs to lock in better returns for a fixed period.

Mutual fund ownership has seen a mixed trend. While the average balance held in mutual funds has risen, signalling that those who continue to invest in them are committing larger amounts of money, the total number of households holding mutual funds has declined.

What now?

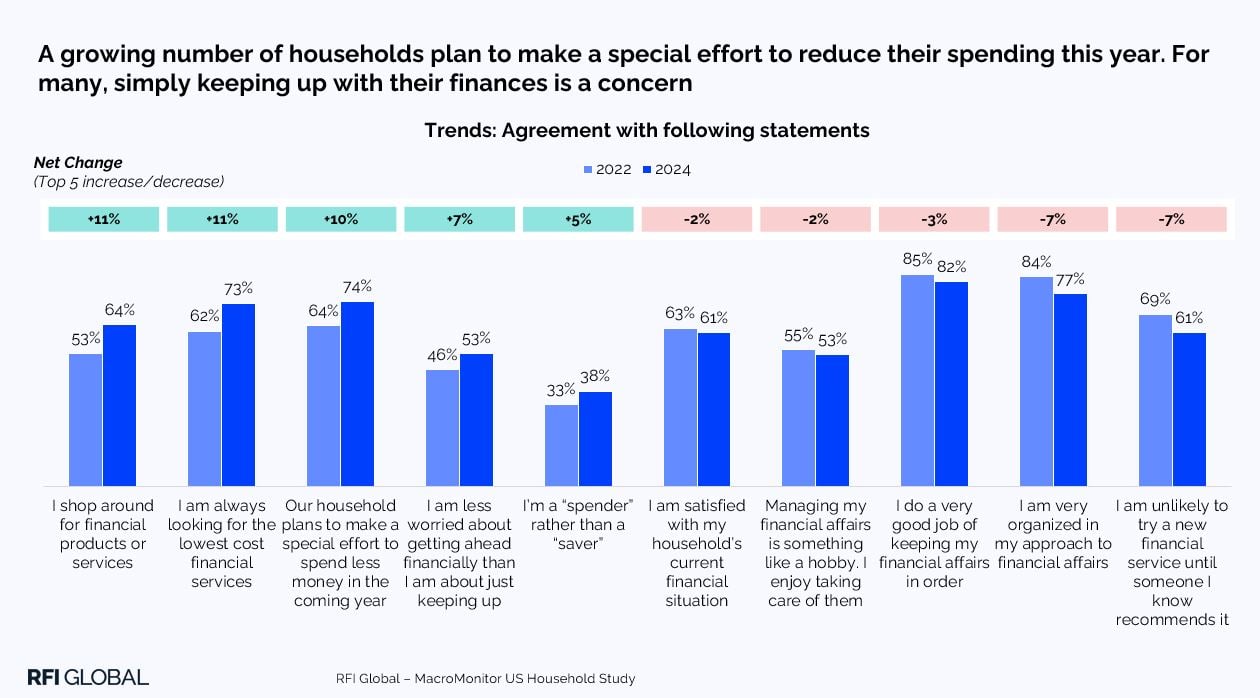

As we move further from the pandemic, the lingering effects of the drawdown in liquid wealth are more evident. Without the financial cushion that helped people sustain consumer spending during the height of the pandemic, many households are now struggling to keep up with higher prices and rising debt levels. MacroMonitor data shows that 53% of households agree they are ‘less worried about getting ahead financially than [they are] about just keeping up’, up from 46% at the end of 2022.

Economic resilience is not evenly distributed

The rise and fall of household liquid wealth in the US during and since the COVID-19 pandemic reflects broader economic trends that have shaped the financial lives of millions. While many households benefited from government support and the inability to spend during lockdowns, the inflationary pressures that followed have eroded much of that accumulated wealth.

The result is a consumer landscape that is increasingly divided, with lower-income and middle-income households facing rising debt burdens, while higher-income households preserve and even grow their assets.

It is evident in the data that economic resilience is not evenly distributed, and those with fewer resources are the first to feel the impact when the safety net of household savings disappears. The questions now are how policymakers and institutions will respond to these challenging economic realities, and how will they address the growing wealth gap and the financial fragility that many households in the US now face.

Get in touch for more insights from MacroMonitor.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.