Luke Allchin, Director, North America

In today’s turbulent economy, US households face tough financial decisions. During a recent Society of Insurance Research (SIR) webinar, I spoke about how these economic shifts have influenced consumer behavior, especially regarding insurance coverage.

The evolving financial landscape

Over the past five years, US households have faced increasing pressures in the aftermath of the global pandemic. Persistent inflation, political volatility, and stagnating incomes, to name a few. These pressures are more than just macroeconomic data points; they are deeply personal realities affecting the day-to-day lives of millions of households across the US. Our latest MacroMonitor study explores how these pressures are reshaping the financial priorities of US households, including critical insights into how they influence their insurance decisions.

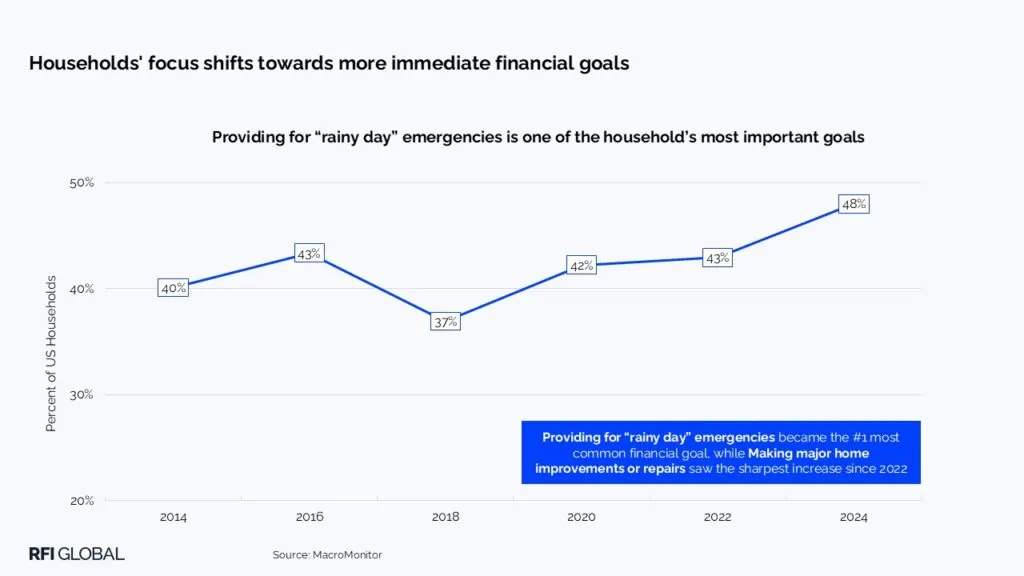

Today, many households are more financially stressed than ever before. Rising costs have driven people to work longer hours and take on additional jobs, yet household finances often feel more disorganized. According to MacroMonitor data, 48% of all households now cite building an emergency or ‘rainy day’ fund as their most important financial goal, surpassing long-term objectives like saving for retirement.

The cumulative effect? Shrinking discretionary income. Despite modest improvements in the job market, wage growth has not kept pace with inflation. Middle- and lower-income families are feeling this most acutely, as they struggle to stretch increasingly tight household budgets.

Rising insurance premiums

In addition to shrinking budgets, households have seen insurance premiums grow. Our data show that insurance costs grew by $718 for the average household in the US between 2022 and 2024 – an increase of 14%. The most significant increases are in home and vehicle insurance, with life insurance premiums also trending upward.

At the same time, employer-sponsored benefits are on the decline. The combination of higher premiums and lower workplace support is leaving many families either underinsured or entirely unprotected against unexpected events.

Reevaluating priorities and rationalizing protection

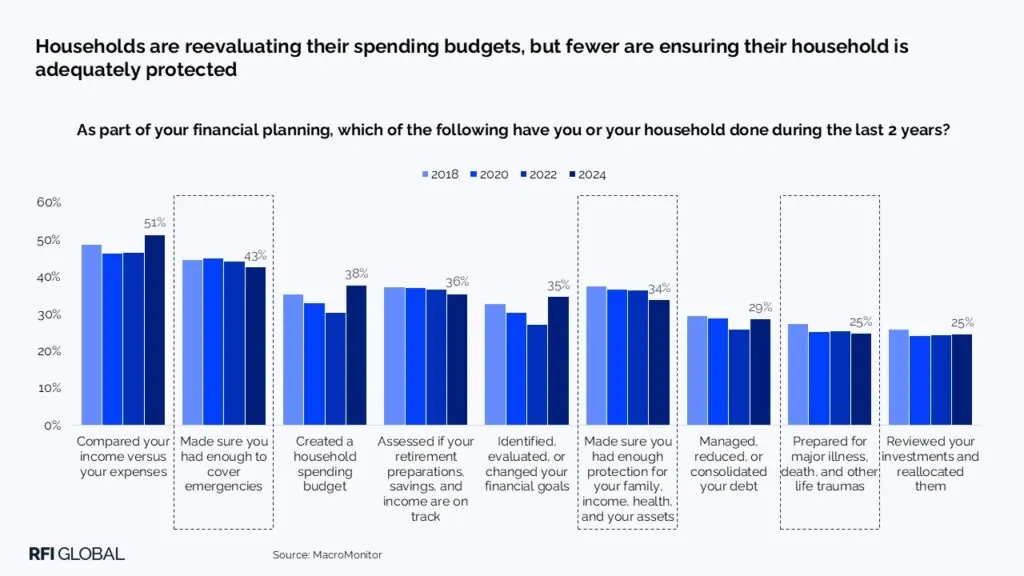

To cope with tighter budgets, households are reassessing their spending priorities. More households are setting budgets, repaying debt, and adjusting financial goals. Unfortunately, insurance coverage is often the first casualty in these revisions.

Life insurance continues a steady decline in ownership, especially for individual policies. Other areas seeing reduced coverage include:

- Home insurance: While structural coverage remains essential due to mortgage requirements, fewer households maintain content and personal liability policies (53% and 48% respectively, down from 62% and 54% in 2022).

- Vehicle insurance: Comprehensive coverage remains steady, and optional protections such as personal injury and liability are being rationalized.

- Health insurance: Though medical plan ownership has rebounded post-pandemic, many households skipped coverage during COVID-19 due to job loss or cost-cutting. Meanwhile, dental and vision insurance have seen slight increases, possibly replacing more comprehensive plans.

Some coverage lines, such as travel, accidental death, and liability insurance, have experienced long-term declines, likely due to shifting perceptions about their value rather than recent financial strain.

That said, there are exceptions. Pet insurance ownership is rising, suggesting that while households are cutting back, they are also reallocating their budgets based on evolving needs and priorities.

Affordability and simplicity

Increased premiums are only part of the problem. A growing number of households cite a lack of need for insurance and the complexity of the buying process as reasons to forgo insurance. Many feel overwhelmed by their financial responsibilities and are looking to simplify where possible.

This desire for simplicity has changed how consumers engage with financial products. There is less interest in face-to-face interactions and a growing preference for streamlined digital experiences. More households now favor buying policies through banks, credit unions, or as part of employee benefits – channels perceived as offering a more streamlined purchasing journey.

We also see a strong preference for consolidating financial relationships and switching providers. MacroMonitor data highlights that 42% of households are considering switching their primary insurance provider, the highest rate in over a decade.

The importance of digital

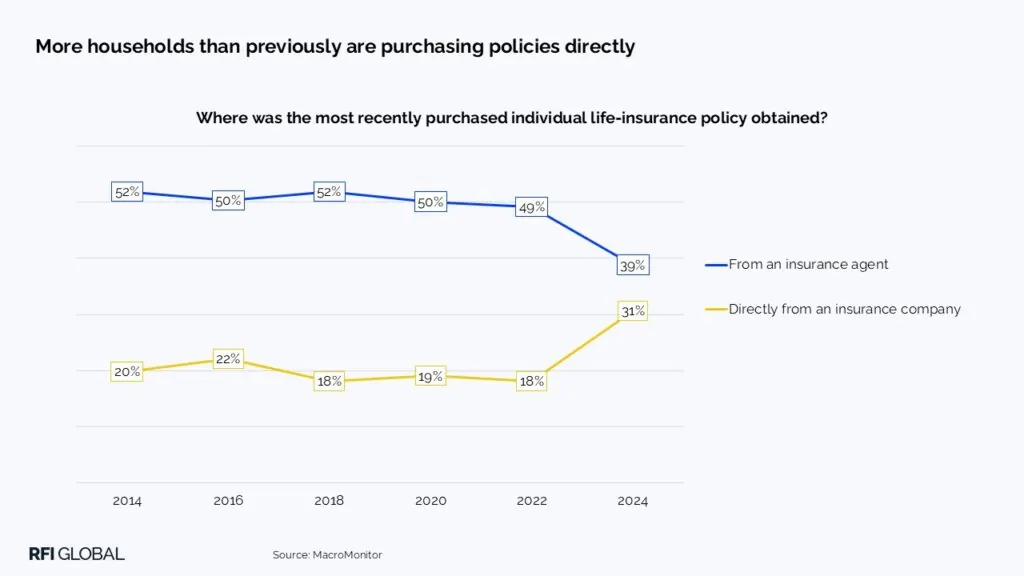

Just as digital banking transformed the financial services sector, insurance is undergoing a similar shift. MacroMonitor shows that 58% of households have now used a digital channel to engage with insurance providers, up from 38% in 2022.

At the same time, direct-to-consumer purchasing is on the rise. More consumers are buying insurance directly from insurance providers rather than through intermediaries, reinforcing the importance of a robust and user-friendly digital presence.

Insurance providers that invest in mobile and intuitive digital platforms stand to gain the most. Not only can these platforms help address one of the biggest barriers to insurance adoption, the perceived complexity of purchasing a policy, but they can also offer easy access to useful information and guidance to help households better assess their insurance needs.

How should insurers respond?

To succeed in the current economic environment, insurance providers must prioritize affordability, simplify offerings, enhance digital channels, offer guidance to those who need it, and leverage existing partnerships.

It is of growing importance that insurance providers remain competitive on price to meet the evolving needs of the lower- and middle-income households who continue to squeeze their budgets ever tighter. Providing resources and tools that help consumers make informed decisions would be well received by consumers, especially those most likely to switch their primary insurance provider who are often the least confident about what coverage they need.

Streamlining policy information, enrollment and claim processes is also crucial to reducing the perceived complexity often associated with purchasing policies and managing coverage. Enhancing digital journeys can support this while also ensuring providers are in a strong position as the insurance market becomes ever more digitalized.

And lastly, in response to shifting sentiments, providers must explore and leverage existing partnerships, expanding access through trusted channels such as employer benefits, payroll deductions, and financial institutions.

The challenges facing US households are influencing consumer behavior and how they make financial decisions. As such, insurers must respond appropriately or risk the insurance market shrinking in line with households’ budgets.

Get in touch to explore how shifting household finances are reshaping the insurance landscape—and what it means for your strategy.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.