Caitlin Hill, Insights Director, Australia

2025 was another year of rapid transformation for financial services in Australia. AI and digital technologies are transforming how consumers engage with their banks, while economic uncertainty and digital capabilities are altering expectations of value, loyalty and service. At the same time, Australian customer behaviour is evolving in ways that reflect both global pressures and local market dynamics.

Our Financial Services Trends and Predictions 2026 report identifies five key trends set to define the year ahead for financial services. Drawing on insights from over 110,000 Australian consumers and thousands of banking app interactions captured via our iSky platform, this article examines how these trends are unfolding locally, highlighting shifts in customer expectations, intensifying competitive pressure, and the opportunities for institutions that move early.

Trend #1: Building trust in AI-powered finance

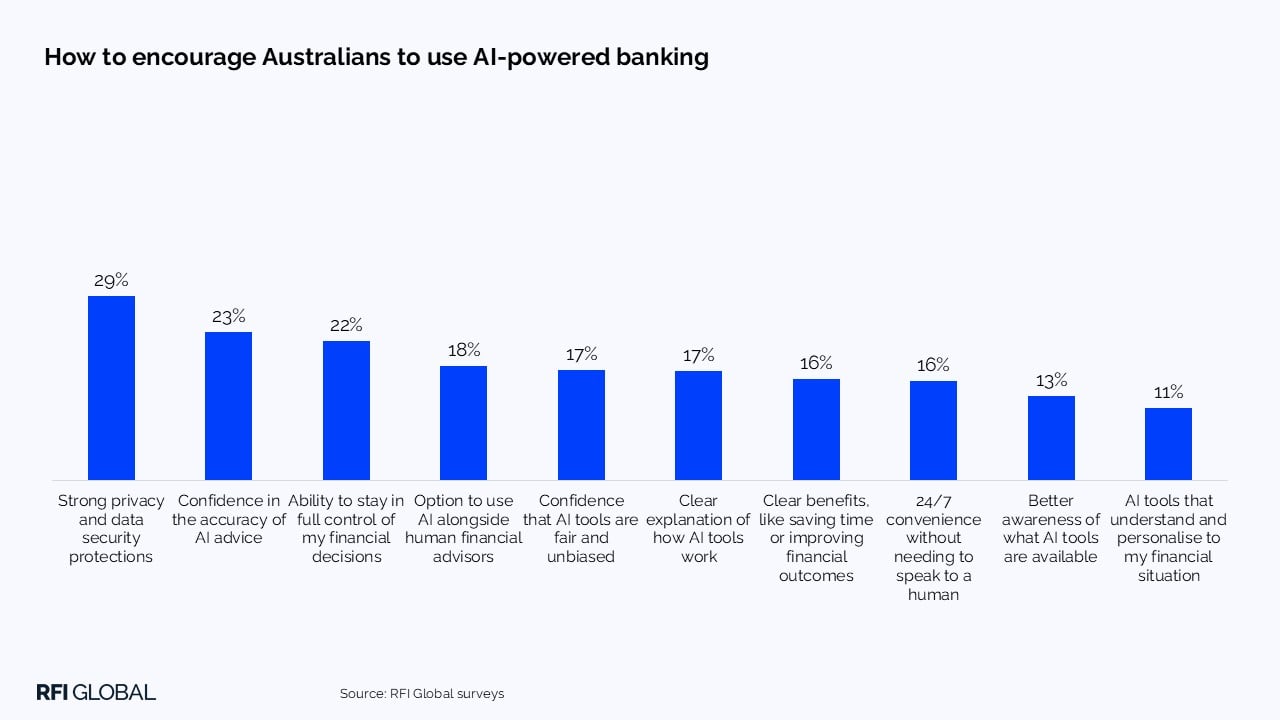

AI has become part of consumers’ everyday lives, shaping how people search, shop, work, and increasingly, how they manage their money. Banks are embedding AI into customer interactions, but adoption is constrained by trust. An overwhelming 94% of Australians have concerns about using AI with their bank, citing privacy and data security (37%), accuracy (30%) and the loss of human support (29%) as the key reasons.

While only one in ten Australians currently use AI to research financial products, more than half are open to using it for product comparison, signalling strong latent demand. To drive adoption, Australian banks must make AI governance visible. Customers want reassurance that recommendations are accurate, aligned to their personal circumstances and supported by robust safeguards around data use. Hybrid models also matter: one in five Australians says the option of human assistance alongside AI would increase their willingness to engage.

Digital behaviour suggests how quickly AI adoption could evolve. Weekly mobile banking usage in Australia has risen from 42% to 68% over the past six years. We expect AI to follow a similar path, moving from cautious experimentation to widespread use once confidence is established.

Banks that get governance, accuracy, and customer control right will lead in AI-enabled finance.

Trend #2: Digital user experience

Mobile is now the primary interface for managing money, and insights from our iSky platform show banks are rapidly expanding features that prioritise security, transparency and customer control.

In Australia, this evolution is particularly evident. Accessibility and customisation are growing priorities, with over 15% of institutions introducing enhanced features and information pages. Payment innovation and UX customisation remain central, with protections such as recipient verification and scam alerts increasingly embedded into everyday journeys. PayID, Osko and PayTo continue to gain traction, while product flexibility is improving. Westpac now enables customers to switch account types or fees without closing accounts, and more than 12% of institutions have introduced in-app card limit controls.

Performance data reinforces this focus, with Westpac, Revolut and CBA performing strongly in Australia, achieving high Voice of the Customer scores for both functionality and user experience.

As expectations continue to rise, Australian banks that excel in usability, security and service will define customer relationships, while those that lag risk competing largely on price.

Trend #3: The next chapter for neobanks

Globally, neobanks are entering a more mature phase. In markets such as the UK, US and Singapore, digital-only providers have moved beyond rapid customer acquisition towards deeper engagement, broader product sets and sustainable profitability, with around a quarter of consumers now holding accounts with a neobank.

Australia tells a different story. Just 6% of consumers hold a neobank account, and the first wave of challengers has largely receded. Of the digital banks granted licences in 2018 and 2019, several have exited or been absorbed by incumbents, including Volt Bank, Xinja and 86 400. Only a small number of players remain, such as Up, now owned by Bendigo and Adelaide Bank, and Judo, which is focused on business banking. Up illustrates the potential of challenger brands: it was named Most Recommended Consumer Bank (Non-Major Bank) in our Australian Banking and Finance 2025 Awards, based on 2024 data, achieving an NPS of +56.3.

In Australia, the legacy of neobanks is a heightened standard for digital engagement. For incumbents, competitive advantage now depends on delivering best-in-class digital experiences that meet rising expectations for simplicity, value and service.

Trend #4: Cybersecurity

Financial fraud is not new, but technology and AI have transformed scams into a global, real-time threat, defined by scale, speed and sophistication.

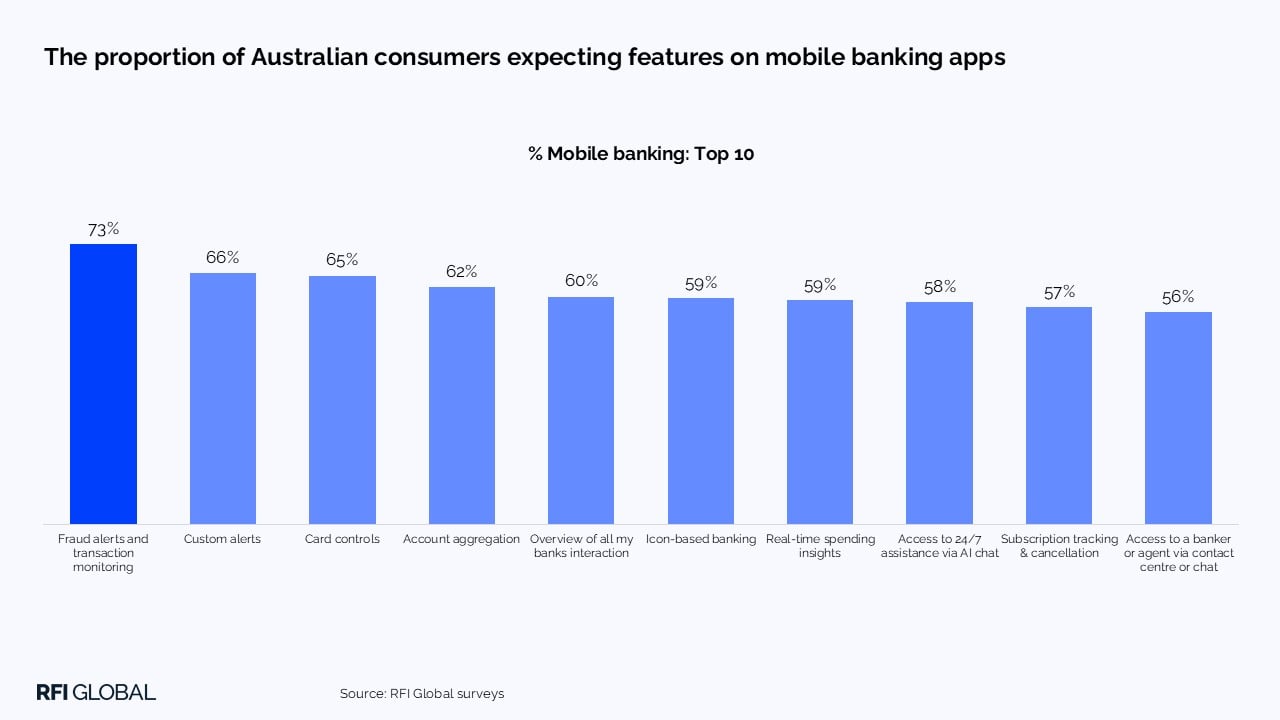

For Australian consumers, trust is now directly tied to how well banks respond when fraud occurs. Five percent of Australians say their bank’s response to fraud is a reason they are considering switching their primary provider. Expectations are also rising; 73% expect fraud alerts and transaction monitoring within their mobile banking app, ranking this ahead of custom alerts, card controls, and account aggregation.

Financial fraud is evolving rapidly. From crypto scams to AI-driven impersonation attacks, criminals exploit digital channels faster than traditional defences can adapt. Traditional authentication is increasingly vulnerable, while emerging threats such as synthetic identities require advanced detection combining transaction data, device intelligence, and behavioural signals – largely invisible to customers.

Cybersecurity is no longer just a risk function; it is integral to operational performance. Banks that strengthen protection without adding friction will be best placed to defend relationships, differentiate on security, and maintain confidence as threats continue to evolve.

Trend #5: Wealth in 2026

Affluent consumers are increasingly looking beyond savings and deposits in search of higher returns, creating a pivotal moment for wealth management. For banks, fee-based income from advice, portfolio management, and related services is increasingly important as net interest margins remain compressed.

Globally, our data shows a clear rise in investment intent among high-net-worth consumers as they seek to make their money work harder. In Australia, more than one in three high-net-worth individuals plan to deploy additional funds into new investments, with nearly a quarter of Australia’s high-net-worth consumers also planning to invest between $100,000 and $500,000 in new opportunities, signalling both confidence and a willingness to diversify.

However, translating intent into revenue remains a challenge due to behavioural inertia, risk sensitivity, and fragmented engagement across multiple providers.

Australian wealth providers that combine timely client engagement with targeted advice and personalised solutions will be best positioned to convert intent into fee-based growth.

What’s next for financial institutions in Australia?

2026 will be defined by the intersection of trust, technology and execution. Australian banks that act early to embed AI responsibly, strengthen cybersecurity and deliver seamless, mobile-first experiences will capture emerging opportunities. For wealth providers, converting investment intent into fee-based growth while managing fragmented relationships will be key.

Download the full Financial Services Trends and Predictions 2026 report to benchmark Australian consumer behaviour, see how local trends compare globally and access actionable insights to guide strategy and growth in the year ahead

Caitlin Hill

Insights Director, Australia

Caitlin Hill is an Insights Director at RFI Global, leading financial services research across Australia.

View full profileFrequently Asked Questions about Australian financial services in 2026

Q: What are the major financial services trends in Australia for 2026?

Five key trends are shaping Australian banking: adoption of AI in customer interactions, mobile-first digital experiences, evolving neobank dynamics, cybersecurity and fraud management, and changing investment activity among high-net-worth consumers.

Q: How are Australian consumers adopting AI in banking?

While only one in ten Australians currently use AI to research financial products, more than half are open to using it for product comparison, signalling strong latent demand.

Concerns remain around privacy, data security, accuracy, and human support, making transparent governance and optional human assistance critical for adoption.

Q: What opportunities exist for banks and wealth providers in Australia?

Institutions that act early to implement AI responsibly, enhance mobile experiences, strengthen cybersecurity, and provide targeted advice can convert customer intent into fee-based growth and gain a competitive advantage in the Australian market.

Q: How does Australia compare to global financial services trends?

While global markets show rapid neobank growth and AI adoption, Australia has lower neobank penetration, rising wealth investment intent, and strong mobile banking engagement, creating unique opportunities for local banks to lead on execution and customer experience.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.