Tiffany Ng, Client Executive, North America

Prediction markets are no longer an academic curiosity. Over the past couple of years, they’ve grown quickly in both scale and participation, and that growth points to something bigger than a passing trend. It reflects a shift in how younger adults deal with uncertainty, think about risk, and make financial decisions.

For financial institutions, the real question is not whether prediction markets matter. It is what their rise says about how Gen Z and Millennials are learning to think about money, risk, and opportunity.

What are prediction markets, and why do they matter?

Prediction markets are online platforms that let people trade contracts tied to real-world outcomes. The price of each contract reflects how likely the market thinks an event is to happen. As NPR puts it, these markets “price the probability of future events,” turning things like elections, economic data, or cultural moments into signals that update in real time as new information comes in.

What’s important is not just the mechanics. In practice, prediction markets turn belief into probability, price, and feedback. From a macro socio-economic perspective, that makes prediction markets interesting because they show how Gen Z and Millennials form confidence, change their minds, and respond to uncertainty when conditions are volatile. Instead of pretending the future is predictable, these online platforms treat uncertainty as something that can be adjusted for continuously.

A broader backdrop of financial uncertainty

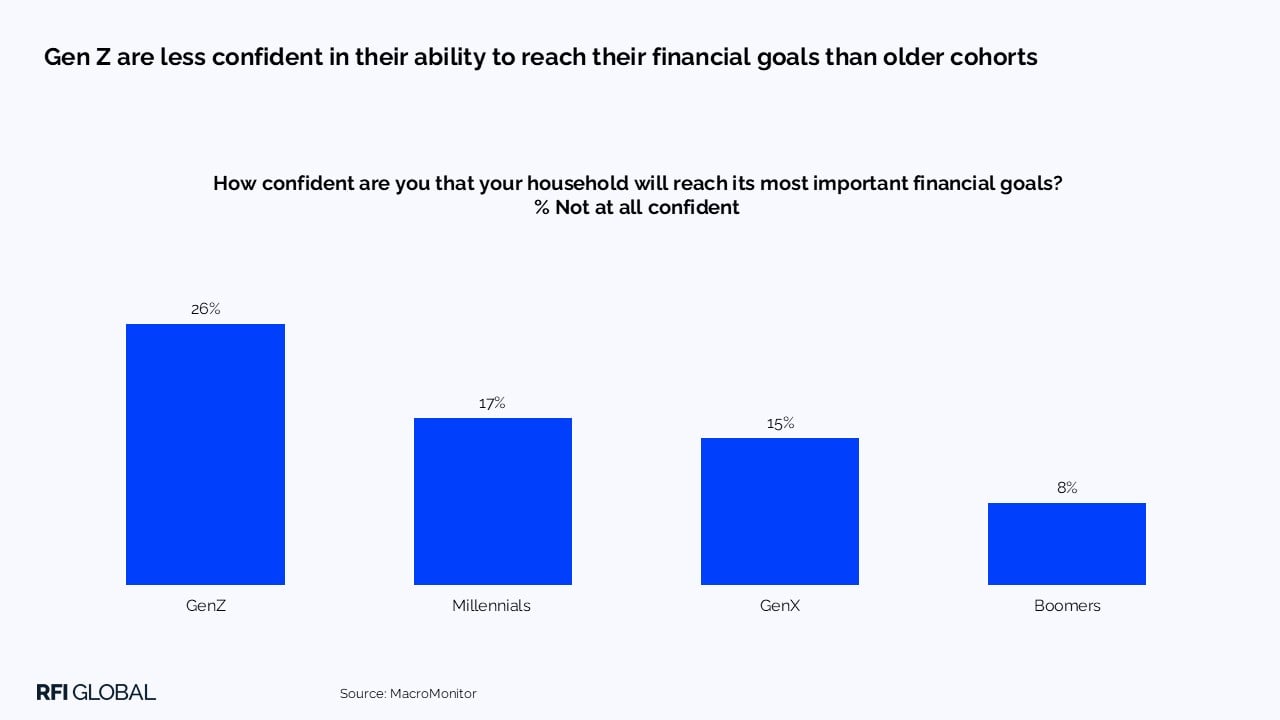

MacroMonitor data, the largest ongoing study of US household financial behavior, helps explain why this approach resonates now. More than a quarter (26%) of Gen Z (born after 1996) say they’re not confident at all about reaching their most important financial goals. That compares with 17% of Millennials (born between 1977 and 1996), 15% of Gen X (born between 1963 and 1976), and just 8% of Boomers (born between 1946 and 1962). Confidence drops sharply as you move younger, right where uncertainty is highest.

At the same time, prediction markets have scaled fast. According to Forbes, monthly trading volume jumped from under $100 million in early 2024 to more than $13 billion by late 2025, with annual volume reaching about $44 billion. Platforms like Kalshi and Polymarket account for a large share of that activity. This is not casual experimentation. It is sustained engagement.

How prediction markets fit into changing investment behavior

Prediction markets cover a range of binary outcome-based products such as contracts tied to real-world events ranging from politics (e.g. if President Trump will invade Greenland) to cultural moments (e.g. who will win the Oscars). Prediction markets transform any future scenario into a potentially profitable wager.

They work for many people because commitment is relatively low, feedback is quick, uncertainty is expressed clearly, and positions can be changed or exited easily. That does not mean younger investors are abandoning traditional assets. MacroMonitor data shows that 20% of Gen Z and 21% of Millennials own individual stocks, so traditional investing still matters.

What is changing is where experimentation happens. The fastest growth in participation among younger generations is in more speculative areas like crypto and prediction markets. These spaces offer immediacy, short feedback loops, and the chance of massive gains, which feels very different from slow, long-term equity accumulation. The shift isn’t about rejecting traditional markets. It’s about where people are learning and testing ideas.

Financial behavior adapts to reality

Financial behavior has always changed with economic conditions. For Millennials and Gen Z, the American Dream was taught as a clear sequence: get educated, find stable work, buy a home, and build long-term security. That belief shaped early choices, including taking on student debt and accepting delayed rewards.

But the conditions behind that model have weakened. Student loan debt reached $1.81 trillion in 2025, up from $1.16 trillion in 2014, according to the New York Federal Reserve. Only 30% of 2025 graduates landed entry-level jobs in their field, and unemployment among 16- to 24-year-olds rose to a post-pandemic high of 10.6%. MacroMonitor data shows that 26% of Gen Z and 31% of Millennials say work and job stability are major sources of stress.

As that pathway became less reliable, financial behavior adjusted. Long-term commitments started to feel riskier. Flexibility, liquidity, and the ability to change course became more valuable. Prediction markets reflect this shift by letting people test assumptions, hold convictions without locking in for years, and update their views as conditions change.

Homeownership and the limits of stability

Homeownership still matters culturally, but it is much harder to reach. MacroMonitor data shows that only 19% of households under 28 owned a home in 2024, compared with 31% of Boomers and Gen X at the same age. That delay weakens homeownership’s role as a stabilizing anchor.

Housing costs add to the pressure. Thirty-nine per cent of Gen Z and 38% of Millennial respondents say housing is a major source of financial stress, far higher than among older generations, according to MacroMonitor data. A tight job market, higher debt, and delayed access to housing all reinforce one another. When traditional routes to stability narrow, it’s not surprising that younger adults look elsewhere for upside, even if it comes with more risk.

Same constraints, different responses

Millennials came of age just as economic mobility became conditional. Our data shows that 45% say saving for rainy-day emergencies is a priority, yet 27% struggle to make ends meet. Almost half (46%) prefer to manage their finances independently rather than rely on advisors, and fewer than half (46%) feel on track to meet long-term goals. Prediction markets give them a way to test their macro socio-economic views and adjust positions as conditions evolve.

Gen Z entered adulthood without ever seeing broad-based stability. Our data shows that ten per cent say easy access to funds matters most when choosing investments. Nearly half (49%) prioritize rainy-day savings, yet more than a quarter (26%) still struggle financially. Financial tools that keep commitments light and allow quick adjustment fit naturally into this environment.

Crypto is another signal of experimentation

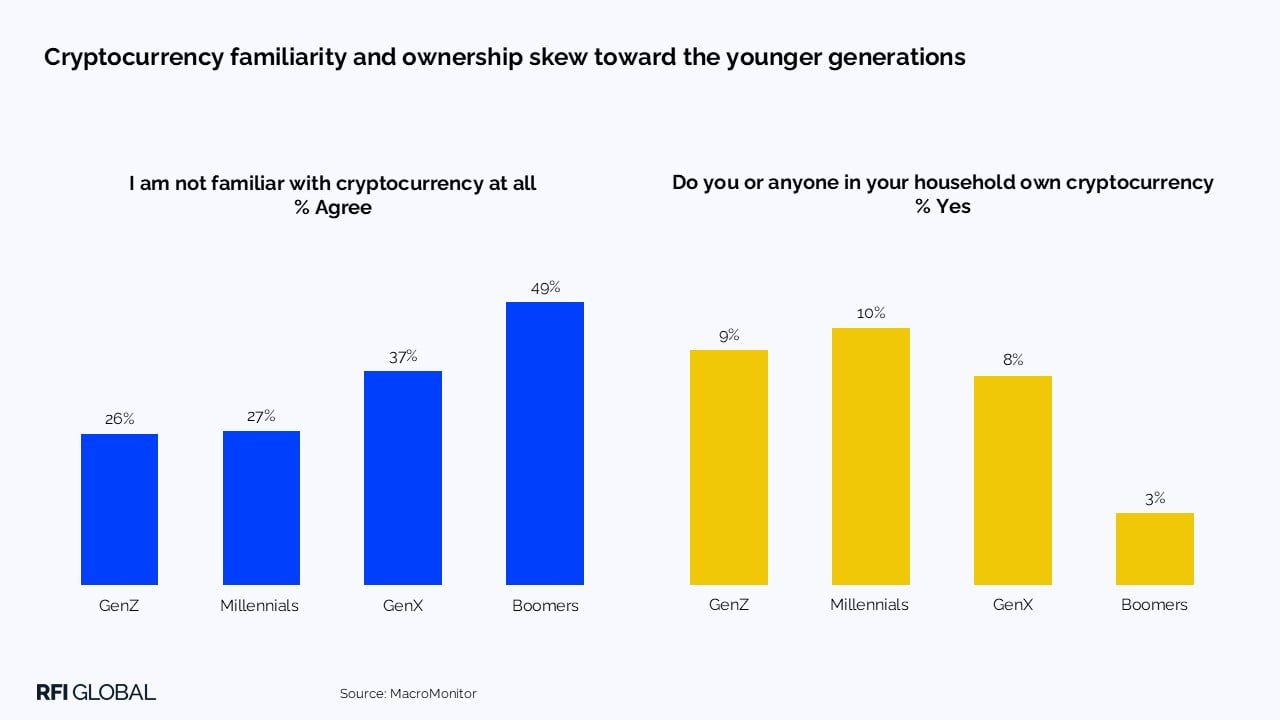

Crypto shows a similar pattern. Ownership is still limited overall, but it skews young. Our data shows that about one in ten (9%) Gen Z and (10%) Millennials own crypto, compared with 8% of Gen X and just 3% of Boomers. Unfamiliarity runs the other way, with nearly half (49%) of Boomers saying they don’t understand crypto, versus about a quarter (26%) of Gen Z and Millennials (27%). The takeaway isn’t mass adoption. It highlights where younger users feel comfortable experimenting with alternatives to traditional finance.

What does this mean for financial institutions?

The rise of prediction markets is a signal of how Gen Z and Millennials are starting to think about money and risk. For many in these generations, beliefs about what is likely to happen — economically, politically, or culturally — are being formed before they ever speak to a bank or advisor. Those beliefs are shaped in environments where probabilities update in real time and uncertainty is treated as normal, not something to be smoothed over.

That shift is becoming harder to ignore as major media outlets like CNN and CNBC partner with platforms such as Kalshi and integrate prediction odds into everyday coverage. For Gen Z and Millennials, this makes probabilistic thinking feel familiar and intuitive. For financial institutions, it means expectations around forecasting, confidence, and risk are being set earlier and outside traditional channels.

As prediction markets and investments increasingly sit side by side in the same apps and media feeds, the line between short-term speculation and long-term investing can blur. For Gen Z and Millennials who are still building their financial foundations, these early experiences shape how they understand risk, returns, and what progress looks like. The implication is not that institutions need to compete with prediction markets, but that financial understanding among younger generations is evolving upstream, with real implications for engagement, advice relevance, and credit behavior over time.

How institutions can respond

The opportunity is not to copy prediction markets, but to learn from what they reveal. Institutions should pay attention to these behaviors as early signals, strengthen education that clearly explains the difference between speculation and investing, and do a better job showing risk in practical terms — what could happen, how likely it is, and what the trade-offs look like.

These shifts also open the door to more behavior-based segmentation. Instead of grouping customers by age or assets, institutions can look at how people deal with uncertainty, how much flexibility they want, and how they learn best. By being open about uncertainty rather than pretending it does not exist, banks and wealth managers can build trust and stay relevant as financial decision-making continues to change.

These insights come from MacroMonitor, the largest ongoing survey of U.S. households. To explore how households are navigating housing, investing, and financial stress in more depth, get in touch to access the full dataset and subscribe to our US newsletter for regular, evidence-based insights.

Tiffany Ng

Client Executive, North America

Tiffany Ng is a Client Executive at RFI Global, supporting financial institutions across North America.

View full profileFrequently Asked Questions about prediction markets

Q: What are prediction markets and how do they work?

Prediction markets are online platforms where people trade contracts tied to real-world outcomes, such as elections, economic data releases, or cultural events. Contract prices reflect the market’s collective view of how likely an event is to occur and update in real time as new information becomes available.

Q: Why are prediction markets becoming popular with Gen Z and Millennials?

Prediction markets appeal to Gen Z and Millennials because they offer flexibility, quick feedback, and a way to engage with uncertainty without long-term commitment. In an environment of job insecurity, high debt, and housing stress, these markets allow younger adults to test ideas, adjust positions easily, and respond to changing conditions.

Q: What do prediction markets reveal about younger generations’ financial behaviour?

They highlight a shift toward probabilistic thinking and shorter decision horizons. Rather than relying on fixed forecasts or long-term assumptions, Gen Z and Millennials are increasingly comfortable updating beliefs as conditions change, reflecting lower confidence in traditional pathways to financial stability.

Q: What do prediction markets mean for banks and financial institutions?

Prediction markets signal that financial beliefs are forming earlier and outside traditional advisory channels. For institutions, this means adapting education, advice, and risk communication to meet customers who are already accustomed to real-time probabilities, visible uncertainty, and flexible decision-making.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.