Scott Muirhead, Client Director, Australia

Australian households are under increased financial pressure and are grappling with insurance affordability as premiums continue to rise. With high inflation and increased cost of living causing ever more pressure, budgets are under strain to afford everyday goods and services without considering the rising cost of maintaining adequate insurance coverage.

For insurance providers, supply chain costs associated with materials and repairs, a hardening global reinsurance market and exposure to increased natural perils over recent years have contributed to the rising costs.

The challenge for providers lies in maintaining successful and sustainable operations while ensuring the impacts to consumers are managed in a way that safeguards the accessibility and affordability of adequate cover for most Australians.

The rising cost of premiums

How big a problem is insurance affordability?

The most recent Australian Bureau of Statistics household inflation results reported a Consumer Price Index (CPI) increase of 3.8% over the 12 months to June 2024. One of the main financial services contributors to that rise was a 14% increase in the price of insurance.

RFI Council data shows that in this environment, over 80% of Australian Home and Motor insurance policyholders experienced a premium increase on their recent renewal. While the vast majority of customers feel their current policies offer adequate cover, 3 in 10 policyholders now say insurance is ‘a lot harder’ to afford than 12 months ago, with 1 in 10 reporting feeling ‘very stressed’ about their ability to afford adequate coverage.

The impact on customers

These rising costs have a direct and significant impact on customers’ ability to manage their insurance policies. The most immediate impact lies in their ability to pay their premiums. Across the industry, 15% reported having some sort of payment difficulty over the past year, with the majority having to make late payments and a lesser proportion missing payments altogether due to lack of funds.

The longer and potentially more detrimental impact on insurance providers lies in the actions customers might take to manage their circumstances. According to RFI Global Atlas consumer insurance study results, there has been a marked decline in Home and Motor policy auto-renewals over the 18 months to June 2024, with less than half of policies being rolled over automatically.

An increasing proportion of policies are now undergoing review prior to renewal, with more customers opting to check comparison sites as well as obtaining quotes from other insurers. While most policies are ultimately renewed with the same provider, our data indicates increased levels of policy-switching over the same 18-month period, with the rate of Home and Motor insurance policy-switching rising by up to 40%.

Not surprisingly, the size of the premium increase will guide switching behaviour. RFI Council results indicate that price increases of 10% or above have the greatest negative impact on customer retention.

So, what can insurance providers do?

In our Banking Uncovered podcast Tara Page, Chief Executive at RAA Insurance, winner of three awards in RFI Global’s Australian Banking & Finance Awards 2024, discusses the key to their customer-centric approach. She covers how they achieved customer excellence by working with and for members, including those who find themselves with affordability concerns in these tough economic times.

To address these challenges, insurance providers should focus on:

Flexibility in payment plans

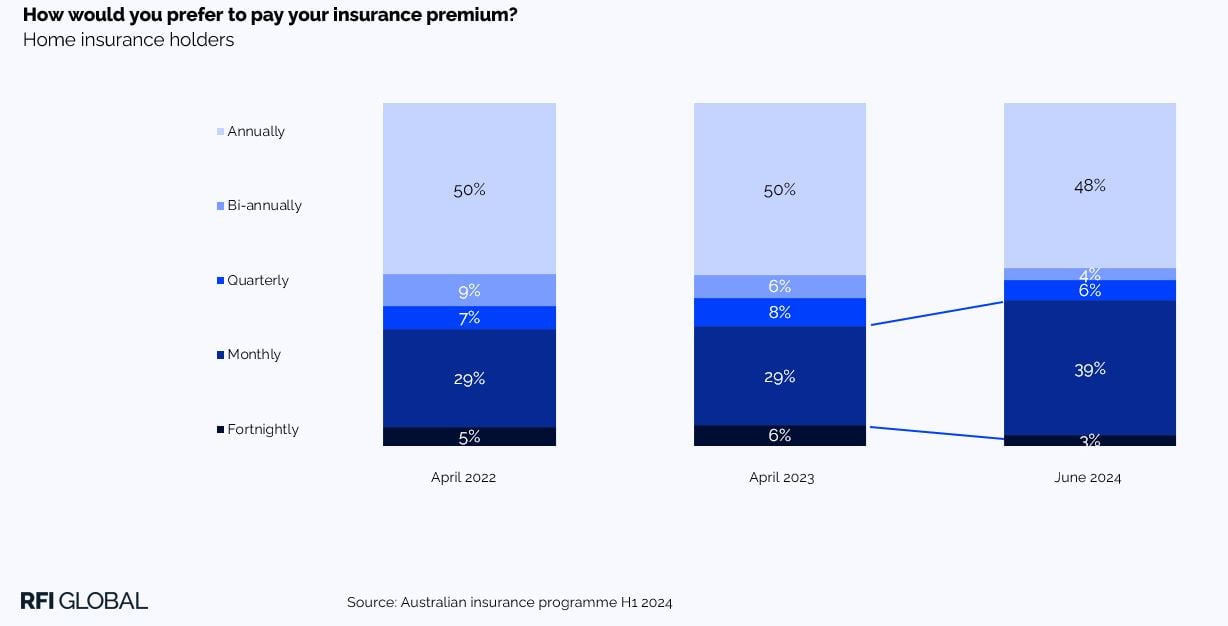

Flexibility is key, particularly when it comes to payments where customers may find smaller more frequent premium payments manageable, ideally without them having to pay more for the privilege. RFI Council data shows a considerable upswing in customer preference for monthly home insurance payments as the sweet spot for managing premiums within a budget full of competing bills.

Flexible product options

Designing products with flexible options to ease the burden of premiums is another area of focus for RAA, with Tara highlighting the importance of helping members make financial decisions that work for them.

Customer Education

Educating customers on their options for reducing premiums – whether eliminating unneeded benefits or tailoring components such as accepting higher excess – becomes the critical area of focus for providers wanting to intervene to assist and retain customers experiencing affordability issues.

Value for money

While price and financial concerns remain the primary drivers for insurance policy shopping around and switching, RFI Council results show the perception of value for money is a growing consideration.

Though important, the balance between cover, benefits and cost is only one component of the value equation. Tara underlines the need to find other avenues to assist members with their cost of living, via loyalty and discount programmes with affiliated partners. This results in a healthier customer base, and a more sustainable organisation able to provide protection and support for its customers into the future.

If you want to learn more about addressing these challenges get in touch for more insights from the studies.

Subscribe to get the latest RFI data and insights.

Scott Muirhead

Client Director, Australia

Scott Muirhead is a Client Director at RFI Global, partnering with financial institutions across Australia.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.