There are many life stage moments where financial institutions have an opportunity to acquire consumers and businesses and build profitable relationships with cross-border payments. Three of these moments share a number of similarities; 17 to 18-year-olds, new immigrants and start-ups. All three of these groups are in differing ways new- to-banking with unique needs.

Teenagers venturing abroad for the first time without parents want to buy money in foreign currencies to use for shopping and paying bills while abroad. New immigrants want to set up bank accounts, but more importantly want to be able to remit monies almost immediately to their home country. New businesses need to make and receive payments. Thanks to globalisation and digitalisation more and more businesses are now set up with international or even global ambitions from day one.

The importance of speed, ease and convenience

RFI Global data shows that all three of these cohorts are focused on speed, ease and convenience when remitting money, making payments in or buying foreign currency. Historically, as Surendra Chaplot, Global Head of Product at Wise, says in our Banking Uncovered podcast, banks have been at best opaque about these processes. There has been a lack of transparency around fees and costs and also it has historically been neither easy or convenient.

While financial institutions and regulators grapple with the complexity of this, as Rupert Lee-Browne, Chairman and Founder of Caxton, states, as far as a customer is concerned it is just a payment. Why should it be any different or more difficult than a simple domestic payment?

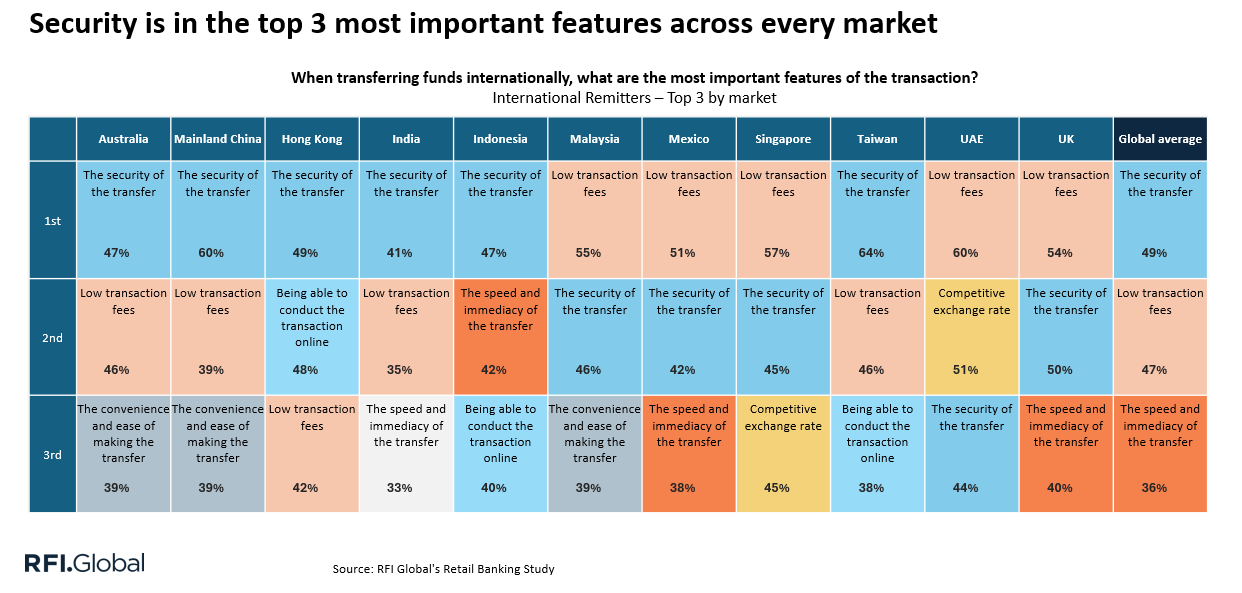

One of the key issues is security

Digital fraud and cyber-crime are now increasing exponentially in all markets. Payments are a weak point. As Jane Prokop, Executive Vice President and Global Head of Small and Medium-Sized Enterprises at Mastercard, states, as those payments move across border, the inherent risk increases significantly. The issue of payments and security is not new. As we emerged from the financial crisis, PayPal started to make significant inroads on the schemes’ share of payments. According to RFI data, at the time about 50% used schemes and 50% used PayPal. When consumers were asked the reason behind their choice, both cohorts cited the same driver – security. This shows its importance and also highlights the fact that it is the perception of security and the reputation for security that is important.

The importance of transparency

The historical lack of transparency, ease and convenience has opened the door for a number of fintechs and challengers to move into this space successfully. Wise and Caxtons are good examples of this.

RFI data shows that in Asia, 55% of remittance transactions are carried out by digital-only providers. However, it has also opened the door for fraudsters. As Jane Prokop says, 43% of cyber-crime is targeted at SMEs while RFI data shows that 90% of SMEs don’t worry about cyber-crime until it’s too late. When we look at RFI’s remittance data we see that security again is the major concern.

Overcoming security concerns for new technology

RFI’s youth and travel data shows that security is a top factor across every payment method. We have seen this happen previously with new payment methods. When contactless first appeared in 2007 in Australia, the appetite for the speed, ease and convenience were inhibited by the concerns around security. Only when the two major retailers accepted them and the limit was raised by gas/ petrol providers to over $30 (the average petrol spend was $38) did the use case become so powerful that the security concerns dissipated.

In 2012, Transport for London offered a free ticket if you used contactless to pay for your travel to help overcome this initial reluctance.

This imbalance or reluctance occurred again with mobile banking in 2012 and with digital wallets in 2017/18. While contactless, mobile banking and digital wallets all grew rapidly once they overcame this reluctance, it was mainly with cohorts that were already banked.

New opportunities for financial service providers

The key difference between previous changes and the opportunity with these cohorts is that the three cohorts all represent new-to-bank opportunities. All three are acquiring a first bank product. All three of these cohorts are also more likely than the average to be open to a digital provider. Providing secure cross-border payments therefore represents a gateway to significant acquisition opportunities and further cross-sell and main bank acquisition.

However, again they share a key similarity. They are all less likely than the average to understand the fraudulent risks inherent in their desired transaction. The fintech, bank or partnership can:

- Educate them about the fraud potential

- Provide a fast easy and convenient service

- Provide a secure service without unnecessary friction

While there has been a lot of focus on providing some combinations of the above there has yet to emerge in most markets or globally a brand or partnership of brands that is genuinely perceived as providing all three.

Whether it is new SMEs transacting cross-border, new immigrants sending money home, or young people having their first genuine independent financial experiences through travel, the size of the pie of each cohort is significant. It represents not just an acquisition boost, but a market-changing dynamic for whichever financial institution or partnership gets it right.

I have written in previous blogs about the need for banks to provide a good cross-border payment value proposition as a defensive measure. RFI data shows that 75% of customers who use a fintech for this are looking to switch their main bank. However, as the data shows, it is the new customer acquisition that cross-border payments represent that provides an even greater opportunity.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.