Jackie Greig, VP Marketing, Global

Consumers increasingly expect their financial institutions to understand their needs and deliver experiences that feel relevant to them. They manage relationships across multiple providers and are more willing to shop around for products and services that offer a better experience. These expectations are no longer set by banking alone. Customers now compare their experiences with the best digital interaction they have elsewhere, from shopping online to streaming entertainment. They expect financial institutions to understand their circumstances, anticipate their needs and make managing money easier.

Technology and AI have made it easier for banks to tailor products, services and communications. Yet many still struggle to deliver experiences that feel genuinely relevant. RFI Global research shows that in the US, only 16% of customers strongly agree that their bank tailors its solutions and communications to meet their needs. Satisfaction is even lower among Gen Z and Millennials. Across all generations, almost two-thirds (65%) want more personalised experiences.

Customers are also looking for greater support, not more communications. In the UK, only 53% believe their bank is proactive in anticipating their needs, falling to just 43% in Canada.

Creating relevant customer experiences

Personalisation is often used as a catch-all term, but in practice, there are two ways to tailor solutions for customers: customisation and personalisation.

Customisation is customer-led. It gives people control over how they interact with their bank, allowing them to tailor interfaces, features, security settings and communications according to their preferences.

Personalisation is bank-led. It uses customer data, behavioural insights and context to anticipate customer needs, delivering relevant recommendations, communications and support at the right moment.

The strongest digital experiences increasingly combine both aspects. Customers want control over the experience they create, while also expecting their bank to use their data intelligently to provide timely and relevant guidance.

Customisation: Giving customers control

Customisation has become increasingly common across digital banking, particularly within mobile apps. Many providers now allow customers to customise themes, dashboards, widgets, notification settings and accessibility features. However, more advanced customisation, particularly across web channels and product experiences, remains limited and inconsistent.

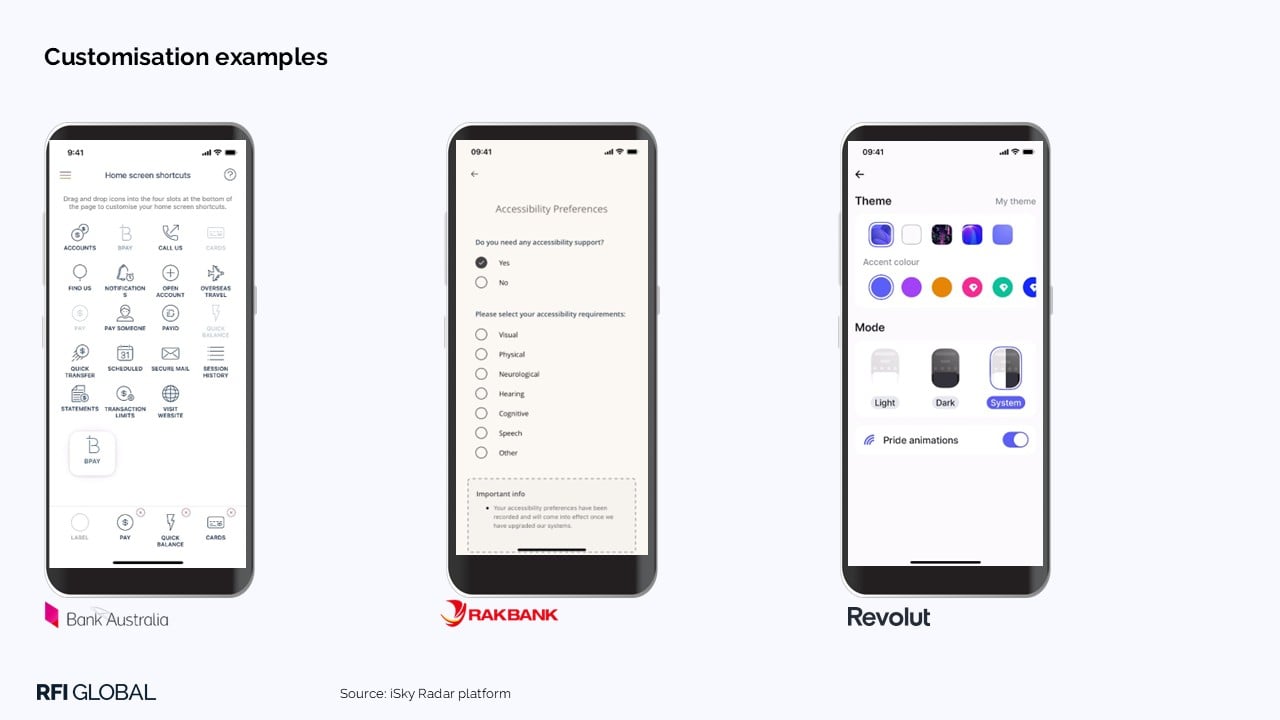

Our iSky Radar platform shows how banks are giving customers greater control over how they interact with digital banking experiences.

Bank Australia gives customers greater control over navigation, allowing them to drag and drop from 20 navigation options to tailor the app around the features they use most.

In the UAE, RAKBANK has introduced accessibility preferences within customer profiles, creating the foundations for more relevant experiences as these capabilities continue to evolve.

Revolut allows customers to customise themes, display modes, background images and animations. Customers can even choose whether to participate in seasonal or cultural animations, giving them greater ownership over the look and feel of the app.

Consumers clearly value customisation. In Australia, 75% want to set their own security preferences when opening a new account. More than half (54%) say being able to customise their dashboard is important, while communication preferences matter even more: 81% want the ability to choose which notifications they receive.

These capabilities may seem simple, but they help create banking experiences that feel more intuitive, accessible and relevant because customers decide how they want to engage.

Personalisation: Making banking more relevant

While customisation puts customers in control, personalisation focuses on making banking more relevant to them. By combining customer data with behavioural insights, financial institutions can anticipate needs, identify potential issues and recommend actions before customers encounter problems. Rather than simply presenting information, personalisation provides meaningful guidance at the moments when customers are most likely to benefit from it.

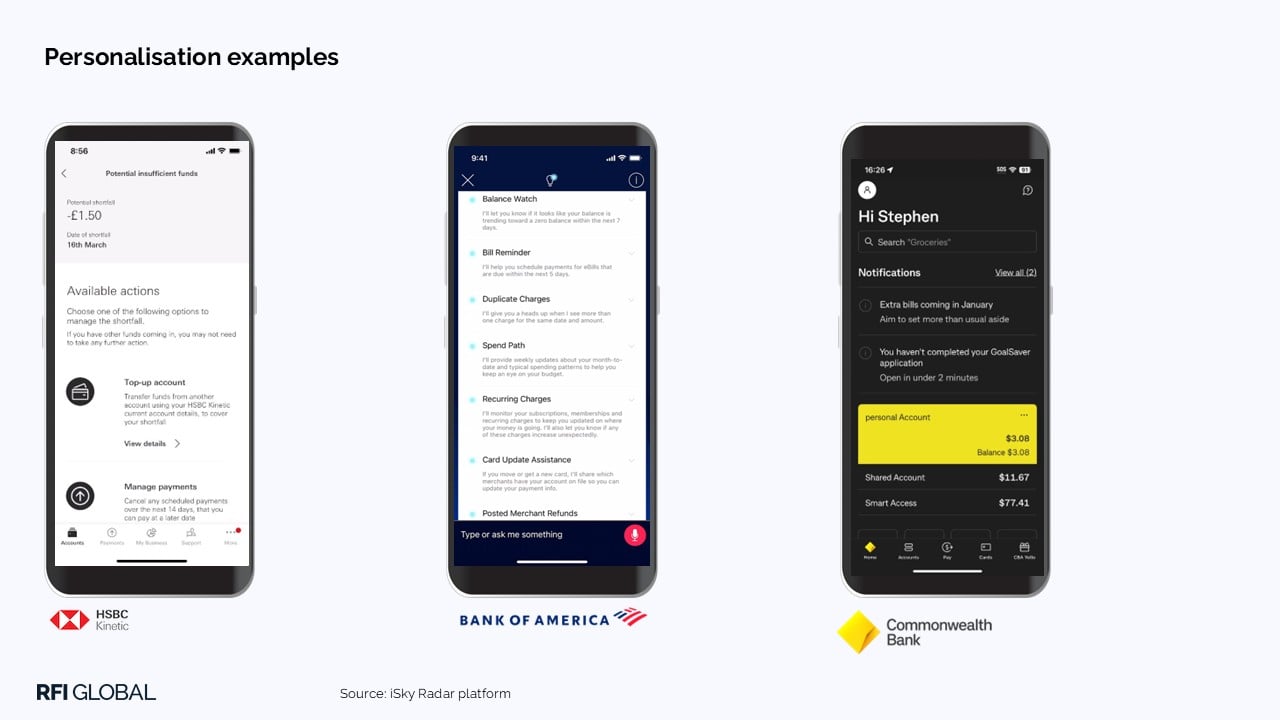

HSBC Kinetic provides a strong example. The app proactively identifies potential cash flow shortfalls, highlighting key information such as balances, upcoming transactions and projected shortfall dates, while offering practical next steps through an ‘Available Actions’ feature.

Bank of America’s Erica, recognised as one of the leading virtual assistants in banking, delivers personalised alerts on duplicate charges, bill reminders, refunds and unusual spending patterns, helping customers stay informed and on track.

Commonwealth Bank’s mobile app takes a similarly proactive approach, identifying upcoming bill increases and encouraging customers to set aside additional funds before those higher payments are due.

While the applications differ, the objective is the same: to deliver the right information to the right customer, at the right time. The most effective personalisation doesn’t just provide more information; it helps customers take action and make better financial decisions.

Beyond personalisation: delivering support that matters

RFI Global’s Financial Services Trends & Predictions 2026 report identified a growing focus on customer-controlled in-app features that improve confidence, transparency and relevance. According to iSky Radar data, over the past two years, 16% of banks globally have introduced profile management or account closing capabilities within their mobile apps. These developments reflect growing recognition that customers want greater control over both their digital identity and their banking experience.

Customisation and personalisation are both valuable, but they deliver impact in different ways. Customisation empowers customers to define how they engage, while personalisation helps make banking simpler, more proactive and more relevant. The most effective experiences balance customer control with intelligent, well-timed intervention.

Financial institutions must decide where that balance sits. Should experiences automatically adapt to customer behaviour and preferences, or should customers actively define how they want to engage? The answer will vary by customer segment, market and use case, but the strongest strategies are likely to combine both approaches.

The biggest challenge is that expectations are no longer confined to financial services experiences. Companies like Amazon, Netflix, YouTube and Spotify have set a new standard for convenience, relevance and anticipation of customer needs.

Financial institutions already have access to vast amounts of customer data. The competitive advantage will come from how effectively they collect and connect customer insight, activate it intelligently and deliver support at the moments that matter most.

Customers are not looking for more features. They are looking for banking that understands their needs, adapts to their circumstances and helps them make better financial decisions. As expectations continue to rise, success will depend on how effectively financial institutions turn relevant customer insight into experiences that genuinely improve the customer journey.

Get in touch to find out what customers in your market expect from tailored experiences, communications and support.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileFrequently Asked Questions

Q: Why does personalisation matter in banking?

Personalisation matters because customers increasingly expect their financial institution to understand their needs and deliver relevant experiences. They are also more willing to switch providers and compare their banking experience with the best digital interactions they have elsewhere. Banks that deliver relevant, timely support are better positioned to strengthen engagement and deepen customer relationships.

Q: What is the difference between personalisation and customisation in banking?

Customisation is customer-led and allows people to tailor how they interact with their bank, including dashboards, notifications, security settings and accessibility preferences. Personalisation is bank-led and uses customer data and behavioural insights to anticipate needs and deliver relevant recommendations, communications and support. The strongest banking experiences combine both approaches.

Q: How can banks deliver more relevant customer experiences?

The most effective banks balance customer control with intelligent, well-timed intervention. They use customer insight to tailor experiences around behaviours, preferences and financial circumstances, helping customers make better decisions and making banking feel more intuitive and relevant.

Q: How can banks use customer data to improve customer experience?

The competitive advantage does not come from collecting more data. It comes from connecting customer insight, activating it intelligently and delivering support at the moments that matter most. Leading banks use customer data to proactively identify potential issues, provide timely recommendations and make banking more useful and relevant to individual customers.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.